Download

1 / 65

980 likes | 1.51k Views

Analyzing and Recording Transactions. Chapter. 2. Learning objectives. Analyzing and Recording Process Source document, Accounts & Ledger T-account vs. Debit & Credit Double-Entry Accounting Journalizing and Posting transactions Transaction analysis for FastForward Trial Balance

E N D

Analyzing and Recording Transactions Chapter 2

Learning objectives • Analyzing and Recording Process • Source document, Accounts & Ledger • T-account vs. Debit & Credit • Double-Entry Accounting • Journalizing and Posting transactions • Transaction analysis for FastForward • Trial Balance • Decision analysis: Debt ratio • Wells Fargo, Hangseng Bank, CCB

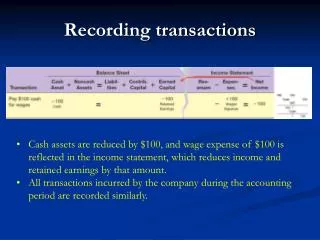

Analyzing and Recording Process- Transactions Exchanges of economic consideration between two parties. External Transactions occur between the organization and an outside party. Internal Transactions occur within the organization.

Record relevant transactions and events in a journal Analyze each transaction and event form source documents Post journal information to ledger accounts Prepare and analyze the trial balance 1.Analyzing and Recording Process- Transaction recording process

2.Source Documents, Accounts & Ledger- Source documents Bills from Suppliers Checks Purchase Orders Employee EarningsRecord Bank Statement Sales Tickets

2.Source Documents, Accounts & Ledger - The Account and its Analysis An account is a record of increases and decreases in a specific asset, liability, equity, revenue, or expense item. The general ledger is a record containing all accounts used by the company.

2.Source Documents, Accounts & Ledger - The Account and its Analysis AssetsAccounts LiabilitiesAccounts EquityAccounts = +

2.Source Documents, Accounts & Ledger - Asset Accounts Cash Accounts Receivable Land AssetAccounts Notes Receivable Buildings Prepaid Accounts Equipment Supplies

2.Source Documents, Accounts & Ledger - Liability Accounts Accounts Payable Notes Payable LiabilityAccounts Unearned Revenues Accrued Liabilities

2.Source Documents, Accounts & Ledger - Equity Accounts Owner’s Capital Owner’s Withdrawals EquityAccounts Revenues Expenses

– – + + Owner’s Capital Owner’s Withdrawals Revenues Expenses 2.Source Documents, Accounts & Ledger - The Account and its Analysis = + Assets Liabilities Equity

A T-account represents a ledger account and is a tool used to understand the effects of one or more transactions. 3. T-Account VS. Debits & Credits

= + Assets Liabilities Equity EQUITIES ASSETS LIABILITIES Debit Credit Debit Credit Debit Credit +- - + - + 3. T-Account VS. Debits & Credits - Rules for debit & credit accounts

_ _ Owner’s Capital Owner’s Withdrawals + Revenues Expenses Capital Withdrawals Revenues Expenses Debit Credit Debit Credit Debit Credit Debit Credit - + +- - + +- Exh. 3.8 3. T-Account VS. Debits & Credits - Rules for debit & credit accounts(cont.) Equity

3. T-Account VS. Debits & Credits- account balance An account balance is the difference between the increases and decreases in an account.

= + Assets Liabilities Equity EQUITIES ASSETS LIABILITIES Debit Credit Debit Credit Debit Credit +- - + - + 4. Double-Entry Accounting • Each transaction affect al least 2 accounts • In each transactions, amount debited = amount credited • For all transactions, sum of debits = sum of credits • Sum of debit account balance = sum of credit account balance

= + Assets Liabilities Equity Step 1: Analyze transactions and source documents. Step 2: Apply double-entry accounting Step 4: Post entry to ledger Step 3: Record journal entry 5. Journalizing and Posting Transactions- Process

Titles of Affected Accounts • Transaction Date • Transaction explanation • Dollar amount of debits and credits 5. Journalizing and Posting Transactions - Journalizing Transactions

T-accounts are useful illustrations, but balance column ledger accounts are used in practice. Three more columns Post reference column Description column Balance column 5. Journalizing and Posting Transactions - Balance Column Account

5. Journalizing and Posting Transactions - Posting Journal Entries 1 Identify the account.

5. Journalizing and Posting Transactions - Posting Journal Entries (cont.) Enter the date. 2

5. Journalizing and Posting Transactions - Posting Journal Entries (cont.) Enter the amount and description. 3

5. Journalizing and Posting Transactions - Posting Journal Entries (cont.) 4 Enter the journal reference.

5. Journalizing and Posting Transactions - Posting Journal Entries (cont.) Compute the balance. 5

5. Journalizing and Posting Transactions - Posting Journal Entries (cont.) 6 Enter the ledger reference.

6. Transactions Analysis for FastForward- 16 Transactions • Chuke Taylor invests $30,000 cash in Fastward • FastForward pay $2,500 cash for supplies • FastForward pay $26,000 cash for equipment • FastForward purchase $7,100 supplies on credit • FastForward collect $4,200 cash for consulting service • FastForward pay $1,000 cash for December rent • FastForward pay $700 cash for employee salary • FastForward provide consulting service of $1,600 and rent its facility for $300. the customer is billed $1,900 for these services.

6. Transactions Analysis for FastForward- 16 Transactions (cont.) • FastForward receive $1,900 cash from client of transaction 8 • FastForward pay $900 cash to supplier of transaction 4 • Chuke Taylor withdraw $600 cash from Fastward • FastForward receive $3,000 cash in advance from customer for consulting service • FastForward pay $2,400 cash insurance premium for a 24-month coverage beginning from December 1. • FastForward pay $120 fro supplies • FastForward pay $230 cash for December utilities • FastForward pay $700 cash in employee salary for work performed in the latter part of December.

Analysis: Double entry: 101 301 Posting: 6. Transactions Analysis for FastForward- Transaction 1

Analysis: Double entry: Posting: 101 126 6. Transactions Analysis for FastForward- Transaction 2

Analysis: Double entry: Posting: 101 167 6. Transactions Analysis for FastForward- Transaction 3

Analysis: Double entry: Posting: 201 126 6. Transactions Analysis for FastForward- Transaction 4

Analysis: Double entry: Posting: 101 403 6. Transactions Analysis for FastForward- Transaction 5

Analysis: Double entry: Posting: 101 640 6. Transactions Analysis for FastForward- Transaction 6

Analysis: Double entry: Posting: 101 6. Transactions Analysis for FastForward- Transaction 7

6. Transactions Analysis for FastForward- Transaction 8 Provided services of $1600 and rent its test facilities for $300. the customer is billed $1,900 for these services. The accounts involved are: (1) Accounts Receivable (asset) (2) Consulting Revenue (equity) (3) Rental Revenue (equity)

Double entry: Posting: 406 403 6. Transactions Analysis for FastForward- Transaction 8 Provided services of $1600 and rent its test facilities for $300.

6. Transactions Analysis for FastForward- Transaction 9 The client in transaction 8 paid $1900 to FastForward. The accounts involved are: (1) Cash (asset) (2) Accounts Receivable (asset)

Double entry: Posting: 101 106 6. Transactions Analysis for FastForward- Transaction 9 The client in transaction 8 paid $1900 to FastForward.

6. Transactions Analysis for FastForward- Transaction 10 Paid $900 cash as partial payment for its earlier $7100 purchase of supplies, leaving $6200 unpaid. The accounts involved are: (1) Cash (asset) (2) Accounts Payable (liability)

Double entry: Posting: 101 201 6. Transactions Analysis for FastForward- Transaction 10 Paid $900 cash as partial payment for its earlier $7100 purchase of supplies, leaving $6200 unpaid.

6. Transactions Analysis for FastForward- Transaction 11 Taylor withdrew $600 from the business for personal use. The accounts involved are: (1) Cash (asset) (2) Taylor, Withdrawals (equity) Remember that the balance in the Taylor, Withdraws account actually increases. But, equity actually decreases because withdraws reduce equity.

Double entry: Posting: 101 6. Transactions Analysis for FastForward- Transaction 11 Taylor withdrew $600 from the business for personal use.

6. Transactions Analysis for FastForward- Transaction 12 FastForward receive $3,000 cash in advance from customer for consulting service The accounts involved are: (1) Cash (asset) (2) Unearned Consulting Revenue(liability)

Double entry: Posting: 101 6. Transactions Analysis for FastForward- Transaction 12 FastForward receive $3,000 cash in advance from customer for consulting service

6. Transactions Analysis for FastForward- Transaction 13 The accounts involved are: (1) Prepaid Insurance (asset) (2) Cash (asset) FastForward pay $2,400 cash insurance premium for a 24-month coverage beginning from Dec. 1.

Double entry: Posting: 101 6. Transactions Analysis for FastForward- Transaction 13 FastForward pay $2,400 cash insurance premium for a 24-month coverage beginning from Dec. 1.

6. Transactions Analysis for FastForward- Transaction 14 FastForward pay $120 cash for supplies The accounts involved are: (1) Supplies (asset) (2) Cash (asset)

Double entry: Posting: 101 6. Transactions Analysis for FastForward- Transaction 14 FastForward pay $120 cash for supplies

6. Transactions Analysis for FastForward- Transaction 15 FastForward pay $230 cash for Dec. utilities The accounts involved are: (1) Utility Expense (equity) (2) Cash (asset) Remember that the balance in the utility expense account actually increases. But, equity actually decreases because expenses reduce equity.

Double entry: Posting: 101 6. Transactions Analysis for FastForward- Transaction 15 FastForward pay $230 cash for Dec. utilities