Download

1 / 26

360 likes | 1.08k Views

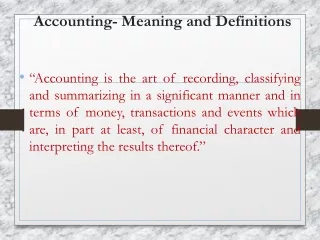

Definitions of Accounting. Make possible the periodic matching of cost (efforts) and revenue (Littleton, 1953).

E N D

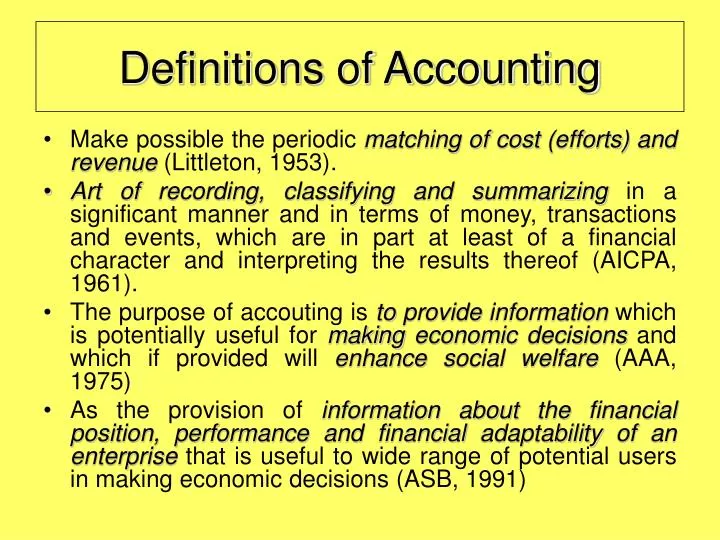

Definitions of Accounting • Make possible the periodic matching of cost (efforts) and revenue (Littleton, 1953). • Art of recording, classifying and summarizing in a significant manner and in terms of money, transactions and events, which are in part at least of a financial character and interpreting the results thereof (AICPA, 1961). • The purpose of accouting is to provide information which is potentially useful for making economic decisions and which if provided will enhance social welfare (AAA, 1975) • As the provision of information about the financial position, performance and financial adaptability of an enterprise that is useful to wide range of potential users in making economic decisions (ASB, 1991)

Definitions of Accounting-Cont’d • The process of identifying, measuring, recording and communicating the economic events of an enterprise to interested users of the information. • identifying? • measuring? • recording? • communicating?

The Roles of Accounting • As a business language - medium of business communication • Decision making tools • Accountability and control - accountability: accountable for action taken (stewardship function) - control: evaluation of performance • As an information system -subsystem to MIS, for decision making and strategy planning purpose.

Accounting Profession • Financial Accountant • Management Accountant • Finance • Auditing: Internal or External

Accounting Professional Bodies • MIA • MICPA • MASB • FRF Q: What are the functions and powers of the above bodies?

Accounting Principles • Going concern • Consistency • Accrual basis

Accounting Concepts and Assumptions Accounting Assumptions • Separate entity • Historical cost • Full disclosure • Prudence • Periodicity • Monetary • Materiality • Matching of cost and revenue • Double entry

Accounting standards • A guide, practice or rules to be followed by accountants when reporting financial information to the publics. • Aim as a guidelines for the accounting practitioner & to narrow down areas of differencs in accounting practices to allowcomparability.

MASB • IAS have been the major thrust in all MASB standards. • FRS ≈ IFRS • Where conditions warrant a separate standard to meet the needs of a particular industry or local regulatory and statutory requirements, MASB will issue a specific standard to fill the gap. Q: What are the procedures for developing a MASB standards? How many standards are currently finalised by MASB?

Accounting policies • Specific accounting principles,conventions and practice chosen by an enterprise in the preparation of financial statements. • eg depreciation methods: straight line, reducing balance, etc.

Qualitative Characteristics of accounting information • Relevant • Reliable • Comparability • Understandability • The accounting assumptions, principles and qualitative characteristics together with accounting standards are collectively referred to as GAAP

Preparation of financial statements • ‘True and fair view’ presentation: • info must be relevant, reliable, comparable and understandable. • Follow GAAP • State reasons if not comply with MASB standards • Choose and use accounting policies as required by para 20 of MASB 1.

Historical cost • Requires assets to be recorded at original costs • If a van is purchased at RM40,000, what will the price of the car recorded in the next 5 years time?

Full Disclosure • Requires all circumstances and events that would make a difference to financial statement users should be disclosed

Prudence • Also known as coservatism • Anticipate no profits and provide for all losses.

Consistency • Presentation and classification of accounting item(s) must be consistent from one accounting period to another.

Materiality • An item is material if the misreporting of that item effects the users’ decision making. • Materiality depends on: • the size or the value of the item • the nature of the item

Monetary • Report all business transactions or events in monetary units, i.e. in RM, USD, Rp, etc.

Matching of Cost and Revenue • Expenses are matched with revenues in the period in which efforts are expended to generate revenues.

Double Entry • Every transactions will be recorded in the journal into debit and credit.

Accrual Basis • Transactions are recorded in the periods in which the events occur, rather than in the periods in which the company receives or pays cash.

Separate entity • States that every entity can be separately identified and accounted for. • Requires accounting activities of an entity be kept separate from those of owner and separate from all other economic entities.

Going concern • The assumption that operation of a company shall continue in forseeable future without being closed or sold. • Allows the use of historical cost when recording assets.

Periodicity • Assumption of an economics life of a business can be divided into artifitial time periods

Users of Accounting Information • Internal users • management for planning and control of business, resource allocation decision making, etc. • External users • investors (existing and potential) • creditors • suppliers • customers • employees • governmnet (LHDN)