Download

1 / 15

150 likes | 326 Views

Long-Term Care Financing Reform: A Federal and Private Insurance Partnership Model. Dan Mendelson January 15, 2008. American Consumers are Largely Unprotected Against the Costs of Long Term Care. Few people are insured against the risk of long-term care costs

E N D

Long-Term Care Financing Reform: A Federal and Private Insurance Partnership Model Dan Mendelson January 15, 2008

American Consumers are Largely Unprotected Against the Costs of Long Term Care • Few people are insured against the risk of long-term care costs • 90% of people over age 55 have no long-term care insurance coverage despite the risk of annual costs exceeding $70,000 • Few Have Adequate Assets • Two-thirds of elderly couldn’t cover more than one year of nursing home care • Medicare doesn’t cover long-term care • Medicaid requires impoverishment for coverage • Coverage only after the exhaustion of personal resources, limited home care coverage for the elderly and no coverage for assisted living services • Family caregivers fill in the gap at high cost to their own well-being • There are 50 million family caregivers in the U.S. • Caregivers are 2 to 6 times as likely to develop depression / anxiety Sources:, AHIP Center for Policy and Research, “Long-Term Care Insurance Partnerships: New Choices for Consumers – Potential Savings for Federal and State Governments,” January 2007. National Family Caregivers Association and Caregiving in the U.S., National Alliance for Caregiving and AARP, 2004 Long-Term Services and Supports: The Future Role and Challenges for Medicaid, Judith Kasper for the Kaiser Commission on Medicaid and the Uninsured, September 2007

Few people are insured against the risk of long-term care costs Population Over Age 55 Source: AHIP Center for Policy and Research, “Long-Term Care Insurance Partnerships: New Choices for Consumers – Potential Savings for Federal and State Governments,” January 2007.

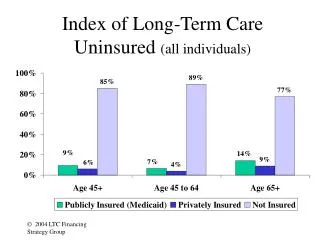

Few Have Adequate Assets Distribution of Elderly Living in the Community by Level of Assets, 2005 Source: Long-Term Services and Supports: The Future Role and Challenges for Medicaid, Judith Kasper for the Kaiser Commission on Medicaid and the Uninsured, September 2007. Uses $70,000 as the nursing home annual cost.

Family caregivers fill in the gap at high cost to their own well-being Hours of Care Per Week Provided by Caregiver Survey Respondents Source: Caregiving in the U.S., National Alliance for Caregiving and AARP, 2004

Government agencies are under budget pressure as the primary payers of long-term care • Medicaid and Medicare together pay nearly 70% of post-acute and long-term care costs • Medicare Hospital Insurance Trust Fund will be exhausted in 2019 • Long-term care accounts for more than 35% of state Medicaid budgets • Individuals using both Medicare and Medicaid are especially a challenge Sources: Avalere Health Analysis of CMS National Health Expenditure Data, Medicare Trustees Report; Medicaid Expenditures for Long-Term Care Services: 1992-3004 by Brian Burwell, Kate Sredl and Steve Eiken

Medicaid and Medicare together pay nearly 70% of the nation’s post-acute and long-term care costs 2004 Nursing Home and Home Care Spending: $185.3 billion Source: Avalere Health analysis based on: Medicare, private and non-CMS public expenditures for free-standing nursing home and home health care reported by Centers for Medicare and Medicaid Services (CMS), National Health Expenditures by Type of Service and Source of Funds for 2004, and Medicaid Expenditures for Long-Term Care Services: 1992-3004 by Brian Burwell, Kate Sredl and Steve Eiken, www.hcbs.org. Figure includes Medicaid spending on ICF/MR.

Individuals using both Medicare and Medicaid are among the costliest to these programs 14% of the population 16% of the population Sources: MedPAC Data Book 2006: Section 3, Dual Eligible Beneficiaries, June 2006; John Holahan and Arunabh Ghosh, “Dual Eligibles: Medicaid Enrollment and Spending for Medicare Beneficiaries in 2003, for the Kaiser Commission on Medicaid and the Uninsured, July 2005.

Goal: Provide incentives and opportunities for individuals to protect themselves against the financial risk of LTC • Provide federal catastrophic long-term care coverage for individuals who contribute –according to their ability— toward the costs of long-term care • Reward individuals who save or insure for future LTC costs by age 55 or earlier • Reshape private financing options and improve affordability through creation of federally-approved private financing options, including LTC insurance • Establish strong public outreach campaign to educate the public about the availability of the new options

Goal: Preserve and improve the safety net through modernization of government benefits and choice of care options • Replace Medicaid coverage of long-term care services for low-income elderly with federal uniform eligibility rules and benefits • Exempt low-income elderly from the private contribution requirement • Improve benefit options by adding the choice of: • cash certificates for home and community-based services, including family caregivers, and • assisted living facility services

Goal: Ensure that beneficiaries are cared for in the most appropriate setting and align care delivery with a single financing entity • Create comprehensive, nationwide post-acute and long-term care assessment system for determining need and benefits • Implement a new Medicare post-acute care payment system based on characteristics of the patient regardless of the post-acute care setting in which the patient receives care • Federalize existing Medicaid LTC benefits to ensure that post-acute and LTC services are appropriately aligned

New System Medicare Low-income Receive Federal Benefit Post-Acute Care Personal LTC Contribution Federal Catastrophic Home Health Adult Day Care Care Coordinators Determine Placement In-Home/Other Residential Care and Services Skilled Nursing Facility Assisted Living Facility Services Rehab Hospital Nursing Facility Services Long-Term Care Hospital Community/No prior PAC Use FFS unified payment system or managed care Private insurance, LTC savings accounts, reverse mortgage Federal FFS rates, managed care, cash certificates

Sources of Federal Funds Medicare Part A Post-Acute Care Reform State LTC Maintenance of Effort Replacement of Medicaid with Private Coverage Better Management and Targeting of Public LTC Benefits Uses of Federal Funds Catastrophic Coverage Federal Low-Income Benefit Sources and Uses of Federal Funds

Gradual Implementation Needed Package Breadth Requires Multi-Stage Implementation 2007-2012 2012-2017 Federal LTC Benefit Create LTC Payment System and Rules Administer Personal Accounts Transition Duals Post-Acute Reforms Patient Assessment Tool Payment System Reforms Preparatory LTC Reforms Reform LTC Insurance Market Create LTC Financing Tools

Model Summary • Reforms current system to address lack of coverage • Grants incentives for individuals to maintain coverage • Modernizes government benefit structure • Creates consistency across care settings • Creates partnership between federal government and private financing • Fosters improved, affordable private LTC financing and insurance options • Provides public catastrophic benefits to people who plan for their own care • Creates national low-income benefit • Includes cash certificates, managed care, and fee-for-service • Shifts financing and administration from states to feds