Download

1 / 12

120 likes | 203 Views

Oye – III -. Money and finance in the 1930s and 1980s. P fc = $. S. D. Q. Flexible exchange rates. Exch. rate. Inflation. D fc. Imp . Curr Acct balance. Curr Acct Def. Devaluation. Exp . P fc = $. (fixed). D. Q. Fixed exchange rates. Exch. rate. Decline in reserves.

E N D

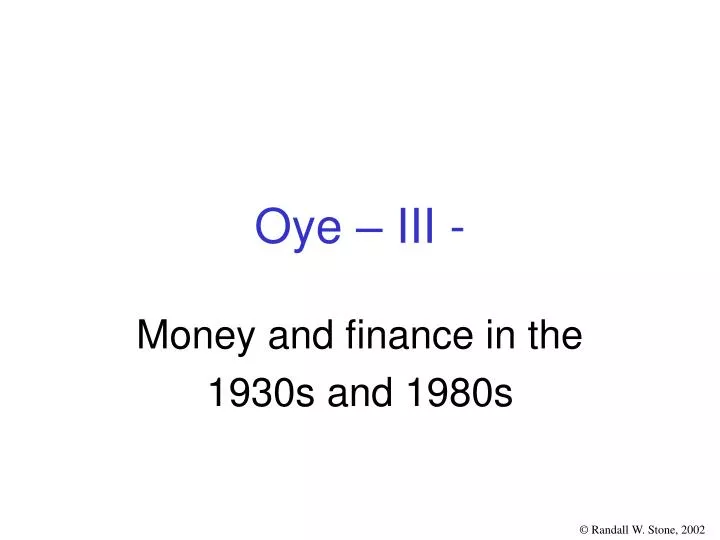

Oye – III - Money and finance in the 1930s and 1980s

Pfc=$ S D Q Flexible exchange rates Exch. rate Inflation Dfc Imp Curr Acct balance Curr Acct Def Devaluation Exp

Pfc=$ (fixed) D Q Fixed exchange rates Exch. rate Decline in reserves Dfc Inflation Imp Curr Acct deficit Real appreciation Reserves Decline Exp

Norms of the gold standard Primary Norms: Secondary Norms: Do not privatize: - Exchange controls - Loans - Sliding tariffs Simmons 1994

International lending in the 1930’s loans US surplus German WWI reparations Collapse: • Run on the Austrian Schilling, 1931 • Run on the German RM 1931 > default, cancellation of reparations Discrimination: • UK - Sterling bloc: loans, markets, debts • Germany - service British banks - not US banks, bonds UK, France WWI debts

Breakdown and reestablishment Breakdown • UK 1931 • US 1933 • France 1936

Breakdown and reestablishment Reestablishment • Tripartite Agreement 1936, further French devaluation • Explanation: interests changed • costs of unilateral cooperation declined • US, UK preferred France’s devaluation to commercial discrimination • reserve holdings liquidated

Objections • Circular • Infer interests from behavior • Explain behavior in terms of interests • Was there cooperation, harmony or mutual defection after 1936?

1982 Debt Crisis--Origins • Rapid expansion of sovereign lending in the 1970s • Reaganomics • U.S. budget deficit → inflation, strong $ • High U.S. interest rates → strong $ → high ratio of debt service/net exports • 1979 oil price shock • Overcommited capital in money-center banks; no incentives for regional banks to lend • Expectations shift → credit dries up → default Contagion effect

Managing the 1982 Debt Crisis IMF, IBRD, FED • 1985 Baker plan (private, IBRD, IMF); little private lending forthcoming • 1989 Brady plan • Conclusion: privatization is necessary Borrowers Banks

Objections • Subsequent evidence: Resumption of portfolio investment in 1990s after successful domestic adjustment • Theoretical: the debt issue area is fundamentally different from trade • There is a basic commitment problem • Lending will dry up unless the commitment problem is resolved

Macroeconomic coordination • Spillovers are public • 1978 Bonn Summit: any effects? • FRG delays a fiscal expansion • 1981-1985 Reagan’s non-contingent strategy • Contraction 1981-1982 • Expansion after 1982 • 1985 Plaza Accord to weaken the dollar • Japan refuses expansionary fiscal policy • Dollar declines because Fed lowers interest rates