Download

1 / 16

180 likes | 240 Views

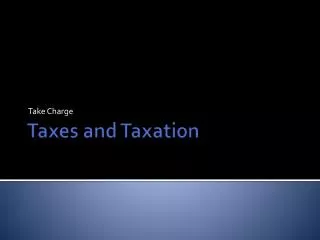

TAXATION AND EFFICIENCY. Chapter 15. Excess Burden Defined. Government levies tax on barley. A. Pounds of corn per year. C a. C b. E 1. C 1. i. F. D. B 0. B 1. Pounds of barley per year. Effect of Tax on Consumption Bundle. A. Pounds of corn per year. G. C a. E 2. C b. E 1.

E N D

TAXATION AND EFFICIENCY Chapter 15

Excess Burden Defined Government levies tax on barley A Pounds of corn per year Ca Cb E1 C1 i F D B0 B1 Pounds of barley per year

Effect of Tax on Consumption Bundle A Pounds of corn per year G Ca E2 Cb E1 C1 i ii F D B1 B0 Pounds of barley per year

Excess Burden of the Barley Tax A Pounds of corn per year G Tax Revenues Ca H M Equivalent variation E2 Cb E1 C1 i ii F D I B3 B1 B0 Pounds of barley per year

Questions and Answers • If lump sum taxes are so efficient, why aren’t they widely used? • Are there any results from welfare economics that would help us understand why excess burdens arise? 15-5

Questions and Answers • Does an income tax entail an excess burden? 15-6

Questions and Answers If the demand for a commodity does not change when it is taxed, does this mean that there is no excess burden? A • Uncompensated response • Income effect • Substitution effect-compensated effect • Compensated demand curve Pounds of corn per year E1 Ca i J R E2 Cb S C1 ii F D K B3 B1 = B2 Pounds of barley per year

Excess Burden Measurement with Demand Curves a Excess burden = ½ ηPbq1tb2 Price per pound of barley Tax revenues Excess burden of tax S’b (1 + tb)Pb g f d i h Pb Sb Db q2 q1 Pounds of barley per year

Preexisting Distortions Theory of the Second Best Double-dividend hypothesis

Excess Burden of a Subsidy m Price per unit of housing services Excess burden n o v Sh Ph u q r (1 – s)Ph Sh’ Dh h1 Housing services per year h2

Excess Burden of Income Taxation Excess burden = ½ εωL1t2 Excess burden SL Wage rate per hour f d i w (1 – t)w h g a L2 L1 Hours per year

The Allocation of Time Between Housework and Market Work Excess burden = ½ (ΔH)tw2 $ $ (1 – t)VMPmkt b w2 a w1 w1 (1 – t)w2 e VMPmkt VMPhome d c Hours worked inhome per year H1 Hours worked inmarket per year H* 0 0’

Does Efficient Taxation Matter? Why no excess burden budget? Is efficiency the primary objective of government policy? Does excess burden mean a tax is bad?

Chapter 15 Summary • Taxes and subsidies generally impose excess burdens, caused by tax- or subsidy-induced distortions in behavior • Differential taxation of inputs also create excess burdens • Lump sum taxes have no excess burden, although are unattractive for other reasons

Appendix A – Formula for Excess Burden A = ½ * base * height = ½ * (di) * (fd) fd = ∆Pb = (1 + tb) * Pb – Pb = tb * Pb di = ∆q η = (∆q/∆Pb)(Pb/q) ∆q = η(q/Pb)∆Pb since ∆Pb = tb * Pb ∆q = η(q/Pb)*(tbPb) = η * q * tb since di = ∆q A = ½(di)(fd) = ½(ηqtb)*(tbPb) = ½ * η * Pb * q * (tb)2

Appendix B – Multiple Taxes and the Theory of the Second Best Price per gallon of gin Price per gallon of rum f c (1 + tg)Pg (1 + tr)Pr g b h Pr a d Pg e Dr’ Dg Dr g2 g1 r1 r3 r2 Gallons of gin per year Gallons of rum per year