Download

1 / 63

630 likes | 645 Views

Learn about banking assets, their classification, and practical application in banking operations. Explore how banks manage fund-based and non-fund-based assets to maximize returns and mitigate risks effectively.

E N D

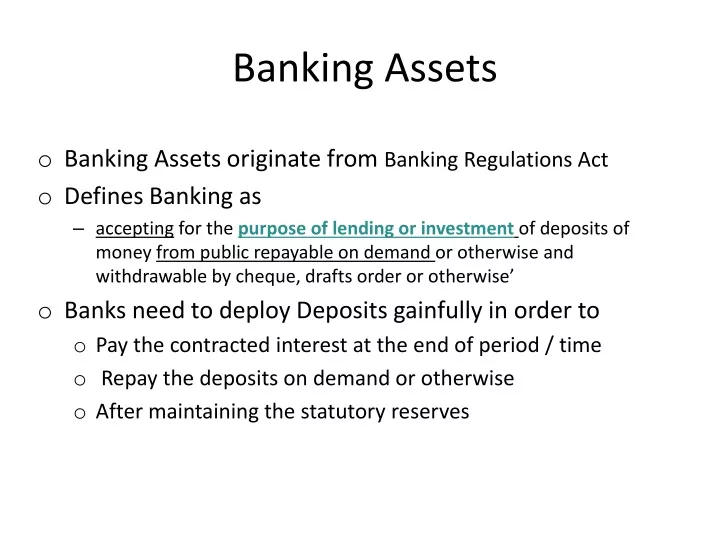

Banking Assets • Banking Assets originate from Banking Regulations Act • Defines Banking as • accepting for the purpose of lending or investmentof deposits of money from public repayable on demand or otherwise and withdrawable by cheque, drafts order or otherwise’ • Banks need to deploy Deposits gainfully in order to • Pay the contracted interest at the end of period / time • Repay the deposits on demand or otherwise • After maintaining the statutory reserves

Banking Assets – Classification • In a Bank’s Balance Sheet Assets are shown as : • Bills Purchased & Discounted • Cash Credits, Overdrafts & Loans payable on Demand • Term Loans • These are re-stated as • Secured by Tangible Assets ( incl Book debts ) • Secured by Bank/ Govt Guarantees • Unsecured • Re-stated again as • Priority Sector & Public Sector • Banks • Others

Banking Assets – In practice • Classified as : • Fund Based Facilities / Products • Non Fund Based Facilities / Products • Above may be either : • Secured by Tangible securities • Unsecured • By Segment • Corporate Banking Products • Large & Mid Corporates • MSME • Retail Banking Products

Fund Based Assets / Products • By Tenor • Bills • Purchased • Discounted • Cash Credit / Overdrafts • Demand Loans - < One year • Term Loans - > One year • Above may be Secured or Unsecured

Non Fund Based Products • Letters of Credit ( LCs ) • Sight LCs • Usance LCs • Guarantees • Financial Guarantees • Performance Guarantees • Deferred Payment Guarantees • Above may be Secured or Unsecured

- FUND BASED Corporate Banking Assets

Fund Based -Traditional Products • Working Capital : • Cash Credit against Stocks / Book debts • Demand Loans • Lock and Key Loans • Bills Purchased & Discounted • Regular • Under L/C • Term Loans :

Fund Based – Contemporary Products • Channel Financing • Factoring • Future Receivables Discounting • Credit card Receivables Securitisation • Lease Rental Securitisation • Loans Against Property ( LAP )

Cash Credit / Overdrafts • Suits most businesses & segments –Universal acceptance • Easy assessment, control and monitoring. • Easy to operate. • Running Account ( with a Debit Balance ) • By Cheques as a running account with governing Limits & Operating Drawing Power • Facility can be run on a in-and-out basis – Regular Deposit & Withdrawals

Cash Credit / Overdrafts • Funding is done from cash-to-cash stage. i.e RM purchase to sales realization • Granted against security of • Stocks ( all stages & kinds ) • Book Debts • In India constitutes the prime source of funding for Corporates • Because of its flexibility and ease of operation • Treated as short term & renewed every year • Technically payable on Demand • Can be a Hypothecation or Pledge

Demand Loans • Payable on Demand after a fixed Term • Usually less than & up to a Year • Can be given for purposes similar to CC • At times built out of Total Fund Based limits • Is also given against other securities • Like FDs, Securities etc • Can be Clean & Unsecured at times • Convenient for short term specified uses • Normally repayment : Bullet payment • Security charge can be a Hypothecation or Lien

Bills Finance • Bills Finance given to Finance Sales & Debtors : • Bills Purchased or • Bills Discounted • Normally given against ‘Sales’ Bills of Exchange • Drawn against Sales in course of business • On acceptable and known parties by the Bak • For period of Usance ( Credit ) upto 3-6 months • Facility gets rolled over on payment of Bills • When Given against ‘Sight Bills’ is called Bills Purchased • Preferred source of lending by Banks when parties are known & acceptable

Bills Finance • Is given as regular fund based limit • Is a preferred source of financing in International Trade • When nomenclatured in FC are called Foreign Bills • Can also be given under LCs of reputed Banks • Big source of Export Finance in Banks • Banks have a Hypothecation charge over the underlying Debts/ dues

Term Loans • Also called as Project Loans • Are given for Asset creation • As name suggests its give for a Term/ period • Usually given for periods longer than 3 years • Up to 10 years and longer • These loans finance small & Large projects • Considered ‘Tricky ‘ loans as taking a credit view over long periods is difficult and changes in business environment rapid

Term Loans • Normally payable in fixed instalments as per repayment schedule agreed upfront • Fixed Term, Fixed amount, Fixed Price • Secured by the assets created by the loan. • Charge on immovable financed is ‘Mortgage’ • Charge on Movable assets is Hypothecation • In term loans usually charge is on a ‘ Pari passu’ basis because there are more than one lenders

Channel Financing • Enables financing the whole supply chain of the anchor customers • dealers and • vendors. • Normally granted to associates of AAA / AA rated borrowers • With excellent payment record • e.g HLL, Maruti, ITC , Nokia, Hero Honda and more….. • Anchor co may/ may not give some comfort to the lender. • Has become a useful tool • to acquire better quality & large volume Assets for Banks/NBFCs • Supplies to dealers are discounted • Take out from the dealers’ cash flow. • Vendors are paid by discounting their sales bills • Repayment are from anchor customers who will pay on due date • Leverages the credit quality of a better rated customer & lowers risk

Factoring • Factoring is financing of the ‘Sales Ledger’ • A ‘Factor’ gets into the shoes of the seller • Manages collections, recovery, sales ledger keeping etc for the seller. • Different from sales bills discounting. • It’s a Buy out • Saves the hassle of hundis, due dates etc • Can be with/ without recourse now • In India usually with recourse to seller • Export factoring is called Forfaiting

Future Receivables Discounting • A very innovative product • to finance Infrastructure projects • Future cash flows discounted • for certain fixed period • Captured through an escrow account and • discounted upfront. • Repayment (Take-out ) is from the future cash flows. • Needs strict monitoring & control • on the future cash flows. • Suits projects like Toll roads, Bridges, Ports,

Rental Securitisation • Future rentals from better rated borrowers are securitised. • Captures the booming business of BPOs and real estate development • Against a fixed term covering loan amount • Premature exits not favored • Classic case of Credit enhancement through Product structuring • Leverages the rating of the Tenant and his Cash flows • Supported by mortgage as security

NON FUND BASED Corporate Banking Assets

Letters of Credit • Letter of Credit • Is a document issued by a Bank to a Seller • Guaranteeing the payment to Seller for goods supplied to a designated buyer • On presentation of the specified documents • LCs are issued as per provisions of UCPDC • Document serves as a guarantee to the seller • that it will be paid by the Bank regardless of • whether the buyer ultimately fails to pay. • Thus, the risk that the buyer will fail to pay is transferred from the seller to the Bank.

Letters of Credit • Letters of credit are used primarily • in international trade for large transactions • There are 4 parties to a Letter of Credit • Issuing Bank • Applicant also ‘The Buyer’ • Beneficiary also ‘The Seller’ • Advising Bank • All LCs issued are ‘Irrevocable’ • Can be amended only at the request or consent of beneficiary • Letters of Credit may be • For imports/domestic purchases and are • Sight • Usance

Bank Guarantees • Another Non Fund Product Line in Banks • Banks leverage their credibility and acceptability to issue Guarantees to Third parties • Guarantees are issued on behalf of their Clients • Bank Guarantees are a good source of fee income & deposits for Banks • Huge demand by Infrastructure , Construction & Project Companies for their business • Enables clients to reduce funds outlay and save costs

Bank Guarantees • Issued for variety of purposes for such clients • Bid Bonds • Earnest money • Advance for projects • Release of retention money • Performance Guarantee • At times for Customs in lieu of customs duty • General & Miscellaneous

Bank Guarantees • There are 3 parties to a Bank Guarantee, viz • Applicant or the Bank’s Client • Beneficiary • Issuing Bank • Bank Guarantees have a validity period and can’t be open n continuing • Unlike LCs they are issued in a free format acceptable to the Beneficiary and Bank

Buyers & Supplier Credit Buyer's credit • Enables local importers ( Buyers ) gain access to cheaper foreign funds close to LIBOR rates • Saves costs and gives longer tenors for payment • Tenor ( Duration ) of buyer's credit varies from country to country, as per the local regulations. • Buyer's credit can be availed for one year in case the import is for trade-able goods • Three years if the import is for capital goods • Interest on buyer's credit may get reset, every six months.

Buyers & Supplier Credit • Exporter or Supplier gets paid on due date; • whereas importer gets extended date for making an import payment as per his cash flows • Buyer can deal with exporter(seller) on sight basis • negotiate a better discount and • use the buyers credit route to avail financing. • The funding can be in any Foreign currency • (USD, GBP, EURO, JPY etc.) as per choice of Buyer • Buyer can use this financing for any form of trade viz. open account, collections,or LCs • Currency of imports can be different from the funding currency, which enables importers to take a favourable view of a particular currency

NATURE OF SECURITIES Nature & Kind of Bank’s charge

Securities • Banks mostly lend against Securities • Unsecured loans are often backed by Personal Guarantees • Borrower must have clear title to securities and capable of charging them to the Bank • Securities can be • Movable • Immovable • Tangible • Intangible • Must be marketable

Kinds of Securities • Securities for Bank Loans • Fixed Deposits • Debt instruments of rated Companies • LIC Policies • Shares of listed Companies • Gold • Corporate Loans • Stocks & Book Debts • Plant & Machinery • Land & Building

Charges & Modes of Creation • Charge on security • Means making a security legally available to the lending banker • Creditor ( Bank ) gets definite & defined rights on assets till loan is repaid / liquidated • Absolute ownership remains with the borrower in most cases

Types of Charges • Lien • Negative Lien • Assignment • Pledge • Hypothecation • Mortgage • Right of Set Off

LIEN : Modes of Creation • Right to retain the goods/securities until debt due is paid • Banker’s lien is more than possessary and is implied pledge • Banker has a general lien • Does not require a separate agreement • Applicable to goods & securities and not to Monies deposited with bank • Possession of goods/securities must be obtained in usual course of business • Right of General lien not affected by Limitation for amounts covered by security value

LIEN… • Negative lien : • Securities do not lie in bank’s possession • Debtor undertakes not to create a charge on unencumbered security • Does not require registration in case of Companies

Assignment • Transfer of Debt, Right / property in favour of the Bank • LIC policies, book Debts, Supply bills • Assignee gets absolute right over security assigned • Other creditors do not get priority over Assignee • Assignee does not get a better title than the assignor

Pledge • Pledge is a bailment or legal delivery of goods by a debtor with an intent to create a charge as security for Loans • Legal ownership remain with pledgor • Possession, actual or constructive with pledgee • Fixed charge in favor of the Bank • Does not require registration with ROC • Not subject to priority claims of other creditors • Pledgee not bound to sell goods by Public auction in case of default at his absolute discretion • After giving reasonable notice to borrower • Sale of pledged goods does not extend Limitation • Bank can sell & recover his dues even after Limitation

Hypothecation • Not clearly defined under law • It is considered an equitable pledge governed by the terms of hypothecation deed • Applicable on moveable goods • Neither transfers ownership or possession to lender • Borrower holds possession as agent of the Bank with constructive possession with Bank. • Needs registration with ROC in case of companies • Most used method to lend by Banks, despite weakness in security and its enforcement

Mortgages • Transfers interest in specific immoveable property in favor of bank • Forms of mortgages used by banks • Mortgage by deposit of title deeds • Simple or Registered Mortgage • Charges registered with ROC in case of companies • Registered mortgage needs to be registered with Sub registrar of assurance within 120 days of creation. • Equitable mortgage can be done at only notified centres • Registered can be done at any centre

Retail Loans • Retail Loans have seen a recent focus by Banks • Was restricted to loans against FDs & Gold and few others on ‘Customer need’ basis • Initially started with • Housing or Mortgage loans as a Priority Sector • Broad based to other assets to meet Retail customer aspiration • Align with Global Banks • Steady rise in portfolios of Retail loans in Banks YOY • Additional avenue has enabled spreading of risk • Better pricing and higher NIMs to boost profitability

Retail Loans- Kinds • Loans against FDs & Securities • Loans against shares • Gold Loans • Car & Two wheeler loans • Mortgage Loans & Loans against Property • Education Loans • Personal Loans • Credit Cards

Loans against FDs & Securities • Basic & simplest Retail Loan Product • Depositor can ,on request, get ‘x’% of the value of FD as loan from the Bank. • Instant & automatic at times • Certain Banks allow drawals on ‘as & when basis’ • Bank note a Lien on the FD to the extent of the loan • Zero risk product with Bank’s Right to set off. • Borrower has the option of adjusting it on due date or repaying the loan as per his convenience • Interest rate charged is normally 2 % higher than contracted rate of FD. • No loans are granted against Other Bank FDs

Loans against FDs & Securities • Loans against Securities • Specified securities as per Bank’s Credit policy • These could be Kisan Vikas Patra, Mutual fund units, LIC policy ( surrender Value ), • Loan is for an ‘x’% of Face value/ market value/ maturity value / surrender value • Borrower needs to service interest on the loan. • Repayment can be fixed as per mutually agreed terms for 6-36 months • Can be given as Demand Loan or Overdraft • Interest charged is as per Bank’s interest rate policy • Bank notes its lien / assignment / charge on security

Loans against Shares • Given against pre approved list of Listed companies shares, as per Bank’s Policy • Given normally as an overdraft for approved uses • Bank holds a Pledge on shares • Loan Limit & DP is calculated as per market value of shares on date of sanction • Value of security is normally checked at weekly intervals • In case of fall in value , Borrower must pay the difference • Margin Call • Margin money for limit calculation is 50 % on MV . • ROI is as per Bank’s extant policy • Bank’s overall exposure under this product falls under ‘ Capital Market’ exposure limit set by RBI

Gold Loans • One of the most traditional Loan products • Because of ease of availability of security • Security is easily marketable and has stable value • Quality & Quantity can be easily checked • Valuation/ Price is available in public domain • Bank holds a Pledge on the Gold • Loans are given for short period • Given as a Demand Loan with regular or bullet repayment • Quite popular in South Indian branches of Banks • Assignment

Auto Loans • Car & Two wheeler loans • Big push in the past 10 years • Erstwhile dominated by Foreign Banks & NBFCs • Thrust has led to the growth of the auto industry • Prior to 2000, only 10 -15 % vehicles were financed • Currently 90% vehicles are financed • Huge impact on Bank’s Balance Sheet • Add-on avenue to deploy funds and improve NIIs • Risk mitigated as large number of clients

Auto Loans • Special structured loans to meet customer needs • Products may differ Client wise- model wise • Products for salaried may be of long tenor • SEP + SENP may have differently designed products • Credit view is taken on asset as well as Client profile • Market Value curve is also a determining factor • Loans vary from 70-90 % of Asset value ( LTV ) • Varies with Brand & Models • Seek to capture existing Free Cash Flows • Credit Decision is a mix of Credit view + Asset view

Auto Loans • Could be EMI oriented • Tenors vary from 3-7 years • Short end typically for 2 wheelers • Banks have a hypothecation charge over asset • Auto loans adopt novel channel for sales • Banks tie up with Auto companies to bring new structured products for their models • To increase sales of vehicles +loans • Also tie up with Auto dealers to improve penetration • Assignments