Download

1 / 42

420 likes | 610 Views

INDIRECT TAX COMPLIANCES. CA. Abhay Desai Managing Partner, M/s Yagnesh Desai & Co. TYPES OF INDIRECT TAXES . VAT/CST EXCISE SERVICE TAX. COMPLIANCES. PAYMENT OF TAX FILING OF RETURNS. VAT/CST. Interest/Penalties Returns Payment of tax. INTEREST - PENALTIES.

E N D

INDIRECT TAX COMPLIANCES CA. Abhay Desai Managing Partner, M/s Yagnesh Desai & Co.

TYPES OF INDIRECT TAXES VAT/CST EXCISE SERVICE TAX CA. Abhay Desai

COMPLIANCES PAYMENT OF TAX FILING OF RETURNS CA. Abhay Desai

VAT/CST Interest/Penalties Returns Payment of tax CA. Abhay Desai

INTEREST - PENALTIES Interest on delayed payment levied @ 18% p.a. (Sec. 30(5)) Penalty for non submission of return in time - Penalty can be levied Rs.100/- per day for first 7 days thereafter Rs. 100 + Rs. 100 per day up to 30 days. Thereafter Rs. 3,000 per month of part of month with a maximum limit of Rs.10,000/- (Sec. 29(5)). Lump sum Dealer : penalty can be levied up to ceiling of Rs.1000/- only. Dealer submitting quarterly return: upto Rs.2000/- only. CA. Abhay Desai

RETURNS Frequency of returns Forms of returns Type of returns Date for filing the returns CA. Abhay Desai

RETURNS (Rule 19) CA. Abhay Desai

RETURNS CA. Abhay Desai

RETURNS CA. Abhay Desai

DUE DATE OF FILING THE RETURNS For E –Return If Tax Payable for the Month is 5,000 or less than Rs.5,000 than within 60 days from the end of the respective Month. If Tax Payable for the Month is 5,000 or more than Rs.5,000 than within 70 days from the end of the respective Month. In case of Dealer who are liable for Quarterly E- Filing of Return than within 75 Days from the end of Quarter. CA. Abhay Desai

DUE DATE OF FILING THE RETURNS For Paper Return Within 30 Days from the end of the Month / Quarter Revised Return - If after furnishing a return if any dealer discovers any error, omission , or incorrect statement therein, he may furnish a revised return before the expiry of One Month from the last date prescribed for Original Return. CA. Abhay Desai

ANNUAL RETURN Every Registered dealer shall furnish Annual Return by way of Self Assessment to the Commercial Tax Officer within whose jurisdiction his chief place of business is situated. Registered dealer who is co operative society engaged in the manufacture of Sugar or Khandsari shall furnish annual return on or before 31st December after end of year to which return relates [ Form No. 205 & 205A ]. Dealer who are liable for VAT Audit shall furnish Annual return within 9 month from the end of the year to which annual Return relates.[ Form No. 205 & 205A]. Dealer to whom permission to pay Lump sum Tax has been granted U/s. 14, 14A ,14B, 14C and 14D within 3 Months [ Form No. 202 ]. Dealer who holds Incentive of Sales Tax Exemption in [ Form No.203 ] and Sales Tax deferment in [Form No. 204]. Any other dealer will have to file within 3 Month from the end of the Year to which return relates [ Form No. 205 & 205A.] In case Turnover Exceed Rs. 1 Crore than E- Filing is also mandatory. CA. Abhay Desai

PAYMENT OF TAX 22 days from end of the month/quarter CA. Abhay Desai

PROCESS CA. Abhay Desai

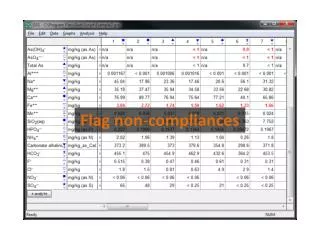

VERIFICATION OF ITC CA. Abhay Desai

EXCISE INTEREST/PENALTY RETURNS PAYMENT OF DUTY CA. Abhay Desai

INTEREST/PENALTIES Interest for delayed payment under section 11AA – 18% Tax default beyond 30 days – penalty under rule 8 – daily clearance on payment of duty in cash, plus prohibition of using cenvat credit, till dues are paid up. Penalty for non-filing of returns: Upto Rs. 10,000 (Rule 27) No revision possible CA. Abhay Desai

PAYMENT OF DUTY SSI Units: 5th of succeeding quarter/6th in case of e-payment Other: 5th of succeeding month/6th in case of e-payment For March: 31st March E-payment mandatory if duty liability exceed Rs. 1 lac in PY. CA. Abhay Desai

RETURNS CA. Abhay Desai

RETURNS CA. Abhay Desai

PROCESS CA. Abhay Desai

SERVICE TAX INTEREST/PENALTIES RETURNS/DUE DATE PAYMENT OF TAX CA. Abhay Desai

INTEREST/PENALTIES Interest: 18% p.a. (Reduced by 3% if value of taxable service less than Rs. 60 lakhs) Penalty for late payment of tax: Rs. 100/day or 1% per month, whichever is higher (Maximum: 50% of tax) Penalty can be waived u/s 80 Fees for late filing: First 15 days: Rs. 500; 16-30 days: Rs. 1000; 31 days or more: Rs. 1000 + 100/day (max. Rs. 20,000) CA. Abhay Desai

RETURNS Form ST-3 To be filed on half-yearly basis Due date: 25th of month following the half-year All assesses to mandatorily file e-returns Revised return: 90 days from original return CA. Abhay Desai

PAYMENT OF TAX Individuals/Partnership firms: 5th day of succeeding quarter/6th of paid electronically Others: 5th day of succeeding month/6th of paid electronically Due date for March: 31st March E-payment mandatory if total payment exceed Rs. 1,00,000 (including CENVAT) CA. Abhay Desai

BUDGET CHANGES W.e.f. 01.10.2014 every assessee has to make e-payment of excise duty. Assistant Commissioner / Deputy Commissioner of Central Excise shall have the power to allow the assessee to deposit tax by mode other than internet banking vide Notification No. 19/2014–Central Excise (N.T.) dt. July 11, 2014. Rule 8(3A) has been substituted to provide that in case of default in payment of Excise Duty, the assessee must suomotu pay a penalty of 1% per month on the amount of Excise Duty unpaid for each month or part thereof. This change will take effect from the date of publication of the amending Rules in the Official Gazette. CA. Abhay Desai

BUDGET CHANGES Slab rate system for interest is proposed w.e.f. 01.10.2014. CA. Abhay Desai

REVERSE CHANGE MECHANISM Currently under reverse charge mechanism, service tax has to be paid at the time of making the payment to service provider. It is proposed that w.e.f. 01.10.2014 service receiver will have to make payment either on the date of payment or the day after 3 months from the date of issue of invoice, whichever is earlier (First proviso to Rule 7 of Point of Taxation Rules). CA. Abhay Desai

M/s Yagnesh desai & Co.819, Siddharth complex,Beside express hotel, Alkapuri,Vadodara – 390007M) 7874668953L) 0265-2339039 OFFICES : Vadodara, Ahmedabad & New-Delhi CA. Abhay Desai