Download

1 / 2

20 likes | 34 Views

<br>Is debt becoming a burden? Consider consolidating it with a personal loan. Tap on the link to check the PDF.<br><br>https://blog.moneyinminutes.in/debt-consolidation-with-a-personal-loan/<br>

E N D

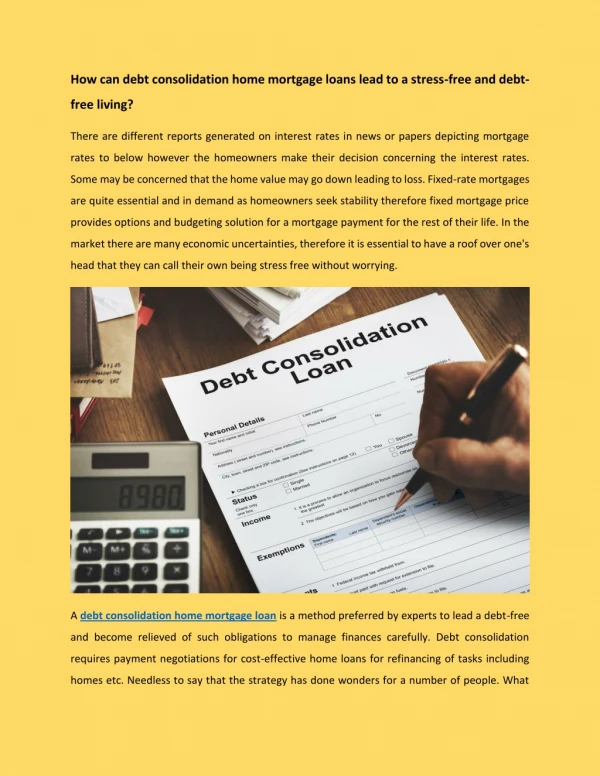

DEBT CONSOLIDATION WITH A PERSONAL LOAN Debts are always seen in the bad light but if we change our perspective a little bit, we can precisely conclude that they play a huge part in fulfilling our goals or dreams. It also helps us to meet different kinds of financial shortcomings that come our way. Everyone at some point in their life must have taken some form of debt or a credit instrument. However, you also must pay due attention to managing the debt. It is as important as getting financial support when you need it. Poorly managed debts can often lead to diminishing credit score and impact your credit history which certainly tampers with your chances of future borrowings. To tackle this situation and have a financially stable life, you must ensure that you do not have multiple debts at one time. Every loan has its own terms of service, EMI dates, and many other things. Having several loans at one time can create a hassle like situation as it is difficult to deal with multiple lenders and their terms and conditions. Here, debt consolidation can prove to be a saviour for you and resolve the blunder of unwise financial planning. To make it more clear, let us tell you about debt consolidation and situations that highlight the need for the same. What is Debt Consolidation? Debt consolidation is a financial tactic used to ease the repayments arising out of multiple existing debt instruments. In simple terms, here, 'debt' means loan and 'consolidation' means to add, which means a loan that adds all kinds of debts in one place and makes it a single loan. It will free you from different short term loans or personal loansthat you have taken in the past, and now you just need to pay for one loan. The debts which are included in this are all kinds of personal loans, vehicle loans, and credit card outstanding bills arising out of multiple credit cards. Consolidating all loans into a single personal loannot only helps ease servicing the debts but also helps you to save some money as now you don't need to pay several interests demanded by different loans and lenders. When should I opt for Debt consolidation? Everyone always tries their best to not fall into the debt trap and maintain a financially stable life. While you may be a master at dealing with debts, there could be a few habits that may be gradually leading you to a debt trap like situation. Here we have listed a few habits/situations that can hamper your financial future and where opting for debt consolidation is the best idea. ● Uncontrolled Spending Habits

If you always have a temptation to buy different things, then you also must be ready to manage your spending. If you are not able to manage your spending, then you have to take a short term loan to meet your end month shortcomings. If you take several short term loans then it is recommended that you first make arrangements to pay your debts on time. If you get trapped between all the due dates and interest rates, go for debt consolidation with a personal loan, which will help you clear off all your existing debts at once and leaves you with liquidity to fuel your spending while also leaving room for monthly savings. High Dependency On Credit Cards Credit cards have become the most convenient way for payment in today's times. The facility of swipe now and pay later have attracted all of us. But if you are unable to repay the amount within the time limit then you have to pay a huge interest rate for that. The interest rate of credit cards is certainly high when compared to a personal loan.Often, we surpass the credit limit in the desire for convenience. To avoid paying high-interest rates on credit cards, you should consolidate the bills with the help of a personal loan. There are options for customised loans, specially designed to consolidate credit card bills arising from multiple credit cards that you own. High Debt To Income Ratio The Debt to Income Ratio (DTI) is the indicator of debts borrowed against the income earned by an individual. It is crucial to balance it for a good financial health and debt portfolio. A DTI of 30-50% is considered to be a healthy DTI ratio. If your debts are more than 50% of your total income earned, then it is a thing to worry and you need to consider debt consolidation. Debt consolidation will help reduce the EMI and will help you manage your repayments. Unable to contribute to monthly Savings If you are busy repaying the principal amount and the interests of your loans and don't have much money left to save for the future, then debt consolidation is a great idea. Savings are very much necessary as they are the primary source that comes in handy during the onset of unforeseen circumstances or any sudden emergencies. You must save at least 20% of your income and if you are unable to save this amount due to other debt repayments and monthly expenses, then you must consider a personal loanthat will certainly help increase liquidity and make more space for monthly savings. ● ● ● A personal loanthat consolidates all your debts into one single loan is the best thing you can do if you are facing the aforementioned situations in your life. It will help you to maintain a good credit score and lead you to a financially stable life. It will also protect you from all the hassles of dealing with multiple lenders and memorizing multiple due dates arising out of multiple loan repayment schedules. Original Source: https://blog.moneyinminutes.in/debt-consolidation-with-a-personal-loan/