Download

1 / 28

300 likes | 683 Views

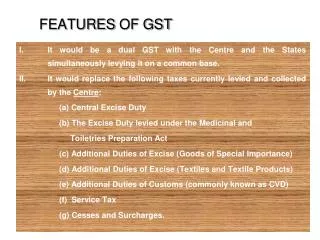

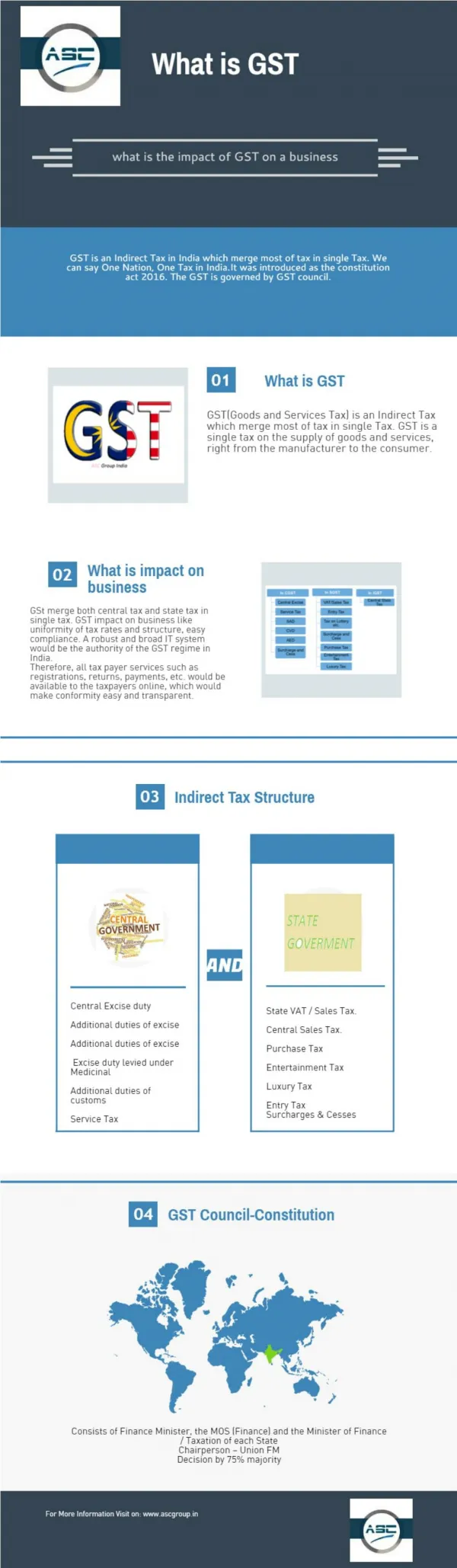

FEATURES OF GST. It would be a dual GST with the Centre and the States simultaneously levying it on a common base. It would replace the following taxes currently levied and collected by the Centre : (a) Central Excise Duty

E N D

FEATURES OF GST It would be a dual GST with the Centre and the States simultaneously levying it on a common base. It would replace the following taxes currently levied and collected by the Centre: (a) Central Excise Duty (b) The Excise Duty levied under the Medicinal and Toiletries Preparation Act (c) Additional Duties of Excise (Goods of Special Importance) (d) Additional Duties of Excise (Textiles and Textile Products) (e) Additional Duties of Customs (commonly known as CVD) (f) Service Tax (g) Cesses and Surcharges.

FEATURES OF GST – contd. • State taxes that would be subsumed under GST are: (a) State VAT (b) Central Sales tax (c) Luxury Tax (d) Entry tax ( other than those in lieu of Octroi) (e) Entertainment tax (f) Taxes on lottery, betting and gambling.

FEATURES OF GST - contd. • Credit of Central GST paid on inputs may be used only for paying CGST on the output and the credit of State GST on inputs only for paying State GST. In other words, the two streams of input tax credit cannot be mixed except in specified circumstances of inter-State sales. • GST would apply to all goods other than crude petroleum, motor spirit, diesel, aviation turbine fuel and natural gas. It would apply to all services barring a few to be specified.

FEATURES OF GST - contd. • Tobacco and tobacco products would be subject to GST. In addition, the Centre could continue to levy Central Excise duty and the State to sales tax. • A common threshold exemption would apply to both CGST and SGST and dealers with a turnover below it would be exempt from tax. A compounding option (i.e. to pay tax at a flat rate without credits) would be available to small dealers above this threshold.

FEATURES OF GST - contd. • The list of exempted goods and services would be kept to a minimum and it would be harmonised for the Centre and the States. • Exports would be zero-rated. • An integrated GST(IGST) would be levied on inter-State supply of goods and services. This would be collected by the Centre so that the credit chain is not disrupted. Accounts would be settled periodically between the Centre and the State to ensure that the State GST components is transferred to the destination State where the goods and services are eventually consumed.

FEATURES OF GST - contd. • The administrative mechanism for CGST and SGST would be harmonized to the extent possible. • CGST and SGST would be levied at rates to be mutually agreed upon by the Centre and the States based on the revenue-neutral rates.

TREATMENT OF INTER-STATE SALES IN GST • Levy of IGST (CGST rate + SGST rate) on inter-state movement of goods and services. • IGST to be collected by Centre. • Dealers/manufacturers making inter-state clearance to submit simple returns to CBEC giving details of quantum of SGST credits used for paying IGST duty and quantum of IGST credits used for paying SGST duty. • NSDL and SBI will act as clearing corporation and clearing bank respectively.

TREATMENT OF INTER-STATE SALES IN GST –contd. • SGST credits and for paying IGST duty to be transferred to the Centre and IGST credit used for paying SGST duty to be transferred to the States. • Adjustments to be made between Centre and the State through the clearing house mechanism. • Manufacturers/ dealers can take credit seamlessly. • It is essential to have Constitutional Amendments for empowering the States for levy of service tax, GST on imports and consequential issues as well as corresponding Central and State legislations with associated rules and procedures

VALUATION PROVISIONS AND GST • Taxable event: Supply of goods and services for a “consideration’. • Consideration ( definition): • Monetary consideration includes currency, cheque, promissory note, letter of credit, draft, pay order, traveler's cheque, money order, postal remittances and other similar instruments but does not include currency that is held for its numismatic value. • Non-monetary consideration includes goods or services supplied as payment for example in a barter ( including part exchange) in the case of services this includes giving up a right, refraining from doing something or agreeing to suffer a loss.

DIFFERENT ASPECTS OF CONSIDERATION -contd. SPECIFIC EXAMPLES OF CONSIDERATION: • Amounts received in furtherance of settlement of disputes Any payment for settlement of issue is generally not a consideration for supply by the aggrieved party. However settlement which grants the aggrieved party a right may be consideration for supply in GST. For example permission for future use of a trading title in lieu of a payment. • Defects: Returnable defects not part of consideration. • Subsidies:

DIFFERENT ASPECTS OF CONSIDERATION -contd. SPECIFIC EXAMPLES OF CONSIDERATION- contd. • Fine and penalties: • Project funding: To be included in supply of rights if there is a legal right. • Deposits: Returnable deposit not includible. • Free samples: Treated as deemed supplies for a consideration. • Compensation for damaged goods: • Repairs under warranties: Not includable.

DEFINITION OF VALUE • Value of a supply is defined to be an amount which with the addition of the GST paid or payable is equal to the consideration when the supplier and the buyer are not related or there is no other consideration flowing from the buyer to the supplier. • Value includes • Taxes , duties, levies, charges including GST on the supplies; and incidental expenses such as commission, packing, transport, insurance cost charged to the supplier.

DEFINITION OF VALUE • value excludes • Price deduction by way of discount for prompt payment • Price discounts and rebates granted to the customer and obtained by him at the time of supply. • Reimbursement of actual expenses incurred as payment of expenditure on behalf of the customer (agency function)

VALUATIONS AND RELATED PERSONS Following treated as related persons :- Inter connected undertakings (defined under section 2 of MRTP Act) Relatives (Section 2 of the Companies Act) Associated persons ( defined under the Income Tax Act) • In the case of supply to related persons the value shall be the open market value. Open market value refers to the full value which a buyer at the same marketing stage is required to pay in order to obtain the goods or services in question at that time and when the buyer and supplier are not related. • When no comparable supply of goods or service can be ascertained ; open market value includes – in respect of goods an amount that is equal to 105% of the purchase price of identical goods failing which is of similar goods or in the absence of a purchase price, 105% of the cost price determined at the time of supply.

VALUATION • Valuation and consideration partly or wholly received in kind: - part kind part cash: • the principle here is what would the provider of part exchange would have had to pay if the payment had been wholly in monetary terms. - completely barter • This would have to be done on the basis of the open market value.

VALUATION - contd. • Valuation in the case of issuance credit and debit notes. • A supplier issuing a credit or debit note is required to make an adjustment to the output tax. • A supplier receiving a credit note or debit note needs to make an adjustment in input tax. For this principle to operate, it is necessary that debit and credit note is issued for a single supply and not by issue of another tax invoice.

VALUATION – contd. • VALUATION IN RESPECT OF MARGIN SCHEMES. • The margin scheme is an optional method of accounting which allows for calculation of GST on the value added rather than on the full selling price. This scheme is allowed in a few situations when there is a problem in taking input tax credit. • Types of margin scheme: • Tour operator margin scheme • Second hand goods ( procured or cleared) • Paintings • Antique deals. • Grant or sale of long term lease. • Auctioneers scheme. • Ineligible item:- - precious metals, - precious stones and ornaments in gold.

VALUATION – contd. • Traders dealing in the sale of eligible goods can use the schemes provided they meet the following conditions: • The trader is registered for GST • The purchase invoices for the goods does not show GST separately. • The trader does not issue a GST invoice or other invoice which shows GST separately for the sale of the goods ( in other words, the buyer cannot take the credit) • All the record-keeping, accounting and invoice requirementsare met. .

VALUATION – contd. Input credit distributor: • In the case of an ‘input credit distributor’ the present scheme under service tax allows for transfer of credit from Head office to other offices when credit relates to supply of services and the supply is received by one of the offices of the registered person. This scheme is likely to continue. • Distribution of such credit will be deemed to be a supply of credit and the value of such credit transfer will be equal to the consideration to which such credit relates

VALUATION – contd. • VALUATION OF IMPORT OF GOODS: In case of imports, the value for GST is proposed to be the value adopted for the purpose of levying additional duty of Customs under Section 3 of the Customs Tariff Act, 1985. when goods exported from India are re-imported after having undergone certain processes like repair/ reworking then the value would be the cost of the value addition abroad, the insurance along with freight both ways plus the customs duty (excluding import GST leviable)

VALUATION – contd. TAX VALUE IN CASE OF IMPORT OF SERVICES: When service is received and duty liability under GST is to be discharged on reverse charge basis , then the importer has two identities – both a customer and a supplier. In such cases the importer discharges the duty liability. The value in such cases will be the total amount paid or payable including any tax levied abroad and converted into rupees.

VALUATION – contd. • VALUATION IN RESPECT OF COMPOSITE SUPPLIES: - Indicators of single supply: • different elements are integrated to the main supply – removal of one supply would affect the nature of supply. • Same amount is charged whether or not the customer buys all elements. ( in-flight meals) • The elements are advertised as a package. • The customer perceives what is supplied as a single supply not as independent elements ( for example, supply of ready-made suit, not separate supply of cloth, buttons, thread or stitching) • Ancillary supplies treated as single supply.

VALUATION – contd. • VALUATION IN RESPECT OF COMPOSITE SUPPLIES: • Indicators of multiple supply: • Separate pricing or invoicing • Elements are available separately. • There is a time differential between parts of the supply. • Elements are not inter-dependent/ connected.

VALUATION – contd. VALUATION IN THE CASE OF TRANSACTION BETWEEN PRINCIPAL AND AGENT: • An agent will be usually involved in at least two separate supplies at any one time – the supplies made between principal and third parties and the supply of agent’s own services to the principal for which the agent may charge a fee or commission. An agent may be a ‘buying agent’ acting on behalf of the buyer or a selling agent acting on behalf of the seller. A pure agent means a person who enters in to a contractual agreement with the client ( recipient of a service) to act on his behalf- such an agent does not use goods or services but only receives the actual amount incurred to procure such goods or services. • Normally when an agent incurs expenditure or costs in the course of providing taxable supply , all such expenditure or costs would be includible in the value for charging GST. However disbursements on account of pure agency functions will not be includible.

EXAMPLES OF TRANSACTIONS • 1 • 2. • 3.

JOB WORK TRANSACTIONS Broad principles: • Job work transactions will not be allowed without payment of GST – they would no more represent an unique transaction. • Job work transactions conform to the definition of taxable event as they represent supply of goods and services for a consideration. • GST is distinguishable on the value addition reflected in the job work charges received. • With the constitutional amendment dutiability will no more be related to the activity of manufacture but to supply of goods and services for a consideration. • Perhaps job work transaction could be brought under the margin scheme.

-- THANK YOU