Download

1 / 27

270 likes | 389 Views

Innovation Napa Valley: Economic Outlook toward Innovation Napa , CA October 17, 2012. Robert Eyler, Ph.D. Professor, Economics Department Frank Howard Allen Research Scholar Sonoma State University eyler@sonoma.edu. Time to wake up.

E N D

Innovation Napa Valley:Economic Outlook toward InnovationNapa, CA October 17, 2012 Robert Eyler, Ph.D. Professor, Economics Department Frank Howard Allen Research Scholar Sonoma State University eyler@sonoma.edu

Time to wake up • Commercialized science from incentives solves problems • Competitive advantages for CA can be lost • Housing’s role in the economy is follower not leader • Markets are global, speedy and moving west

Domestic National Economy • International concerns • European debt issues and solutions: looking better, but remain • What about US debt issues? • Chinese and East Asian growth beginning to slow: why? • Labor Markets • Unemploymentcontinues to fall nationally and in CA: can we live with 7%? • Structural issues versus cyclical: housing markets changed returns to trades • Election year makes hiring and investment difficult to predict • Monetary Policy: Lending markets • Recovery slowbut steady: US more vulnerable to global market changes • Deposits still rising, rates are still low: Federal Reserve now 2013-14 for next rate hike, maybe (why?)

Lending markets: some considerations • Operation Twist (QE 2.5) + QE3 • Lower medium- and long-term rates meant to provide incentives to borrow: why not to lend? • Margin squeeze at banks continues: why is lending not happening? • European debt situation + China connections • If austerity works, European recession coming • May need to sell bonds en masse to pay refinance debts: want to attract China on demand side • American rates may rise slowly also: more cost for lending 7

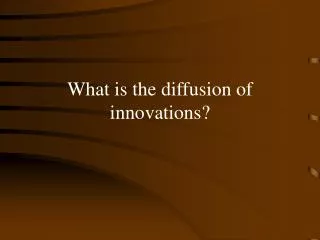

8 Source: Federal Reserve Board

California • Labor Markets • California continues to lag national employment • Continued slow income growth leads to demand uncertainty • Adaptation and Adjustment • Equity markets have softened pension debate: structural problems remain • Labor market bifurcation parallel to housing: (I-5 versus 101) • Public labor market issues may affect private markets • CA needs to be a place where businesses can grow and survive for labor markets to follow • Competition is global 11

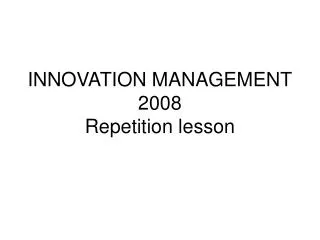

Payroll Employment, Seasonally Adjusted, US and CA, Jan 2000 = 100 Source: EDD

Employment, Seasonally Adjusted, 2000 – June 2012, Index Jan 2007 = 100 Source: EDD

Housing • 2013 continues momentum from 2012 • Distressed inventory still there, but falling quickly • Napa and Marin better than Sonoma for now: why? • Interest rates to be more a problem than help • Will remain low but likely to be volatile • Lending markets squeezed on both sides • Need job growth and stability for true recovery • Housing needs to be seen as a portfolio asset • Shift in demand due to land use, market forces

Distressed Sales, California(Percent of Total Sales) SOURCE: California Association of REALTORS®

Distressed Sales by County(Percent of Total Sales) SOURCE: California Association of REALTORS®

Regional Economy: Part 1 • Business growth has been in small business and self-employed/1099 businesses • True across state, especially North Bay • NB job recovery faster than CA in general • Chicken-egg issue: job creation vs. business creation • Napa is moving toward a more complete export economy • Global marketplace, exposed to global market forces • Differentiated from other, regional competition

Change in Self-Employed Businesses and Payroll Businesses, 2002-10, Napa County

Asset Building as Economic Development: Regional Economy Part II • What “leakages” does Napa have with respect to • Supporting the wine/hospitality/tourism industries? • Utilization of vacant commercial space that can house diverse industries? • Can industrial diversity take place toward innovation? • Do entrepreneurs live in Napa and want to scale/finance businesses? • Are there VC/Angel/Seed financing in Napa that already invest in scalable tech businesses?

Where are we headed? • Recovery into 2013: continued, slow recovery • Investment needs to recover, labor markets to follow • Financial market uncertainty remains • Public labor markets likely to change in 2013 • Election results will help clarify issues • Will a shift of public workers stall progress? • Regional connections, competition to rise globally • Housing market continues to recover • All three macro markets beginning to move as one, just slower than in recent (but not all historic) cycles