Download

1 / 7

70 likes | 179 Views

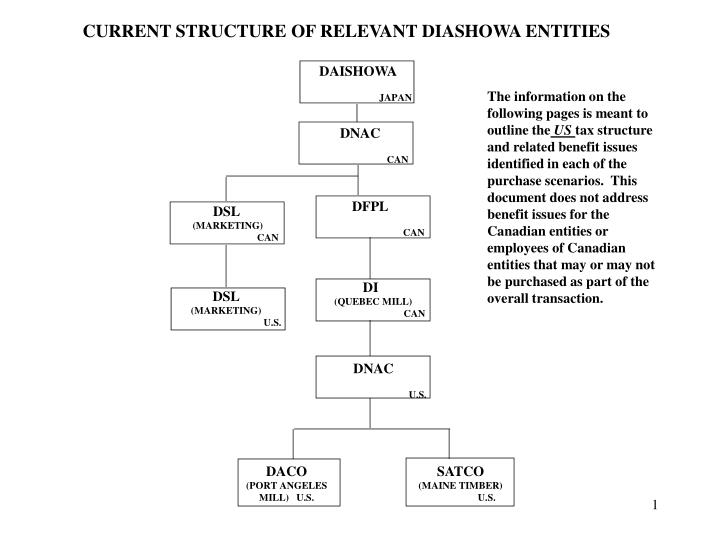

CURRENT STRUCTURE OF RELEVANT DIASHOWA ENTITIES. DAISHOWA JAPAN.

E N D

CURRENT STRUCTURE OF RELEVANT DIASHOWA ENTITIES DAISHOWA JAPAN The information on the following pages is meant to outline the US tax structure and related benefit issues identified in each of the purchase scenarios. This document does not address benefit issues for the Canadian entities or employees of Canadian entities that may or may not be purchased as part of the overall transaction. DNAC CAN DFPL CAN DSL (MARKETING) CAN DI (QUEBEC MILL) CAN DSL (MARKETING) U.S. DNAC U.S. DACO (PORT ANGELES MILL) U.S. SATCO (MAINE TIMBER) U.S.

SCENARIO I – ENRON PURCHASES DSL(CAN) AND DSL(US) AS PART OF ACQUISITION DAISHOWA JAPAN ALT. 1 DNAC CAN Step 1 Move DNAC(US) to DAISHOWA (Japan) or DNAC(CAN) by DI sale to either DAISHOWA (Japan) or DNAC(CA) of DNAC(US) shares. No movement of DNAC(US) or SATCO employees. ALT. 2 DFPL CAN DSL (MARKETING) CAN DI (QUEBEC MILL) CAN DSL (MARKETING) U.S. DNAC U.S. DACO (PORT ANGELES MILL) U.S. SATCO (MAINE TIMBER) U.S.

SCENARIO I – ENRON PURCHASES DSL(CAN) AND DSL(US) AS PART OF ACQUISITION Step 2 Create Enron Newco(US). Enron Newco(US) purchases shares of SATCO from DNAC(US). Movement of SATCO employees into Enron Newco (US). Benefit issues outlined below. DAISHOWA (JAPAN) OR DNAC (CAN) SATCO SHARES ENW NEWCO U.S. DNAC U.S. CASH Benefit Issues For SATCO: a. Extend DNAC(US) plans for 60 days while Enron Newco(US) plans are put in place. b. Put new plans into place for SATCO employees. c. Transfer assets from DNAC(US) plan into Enron Newco(US). DACO (PORT ANGELES MILL) U.S. SATCO (MAINE TIMBER) U.S.

STEP 3 DNAC (CAN) sells DFPL shares to Enron Newco(CAN) and DNAC(US) is not part of the purchase. Benefit issues for DSL(US) employees are outlined below. SCENARIO I – ENRON PURCHASES DSL(CAN) AND DSL(US) AS PART OF ACQUISITION ENA 3RD PARTY INVESTOR 50% 50% ENW L.P. DAISHOWA JAPAN BV-1 DUTCH ENW NEWCO U.S. DNAC CAN SATCO BV-2 DUTCH CASH Benefit Issues For DSL(US) Employees: 1. Transfer ownership of the DNAC(US) plan to DSL(US) or successor entity and fund plan; or 2. Move employees to the Enron Newco(US) entity where SATCO employees go and a repeat steps a. – c. on Page 3 for SATCO employees. DFPL SHARES DFPL CAN DSL(CAN) NEWCO CAN DI (QUEBEC MILL) CAN DSL(US)

SCENARIO II – ENRON DOES NOT PURCHASE DSL(CAN) AND DSL(US) AS PART OF ACQUISITION DAISHOWA JAPAN ALT. 1 DNAC CAN Step 1 Move DNAC(US) to DAISHOWA (Japan) or DNAC(CAN) by DI sale to either DAISHOWA (Japan) or DNAC(CA) of DNAC(US) shares. No movement of DNAC(US) or SATCO employees. ALT. 2 DFPL CAN DSL (MARKETING) CAN DI (QUEBEC MILL) CAN DSL (MARKETING) U.S. DNAC U.S. DACO (PORT ANGELES MILL) U.S. SATCO (MAINE TIMBER) U.S.

SCENARIO II – ENRON DOES NOT PURCHASE DSL(CAN) AND DSL(US) AS PART OF ACQUISITION Step 2 Create Enron Newco(US). Enron Newco(US) purchases shares of SATCO from DNAC(US). Movement of SATCO employees into Enron Newco (US). Benefit issues outlined below. DAISHOWA (JAPAN) OR DNAC (CAN) SATCO SHARES ENW NEWCO U.S. DNAC U.S. CASH Benefit Issues For SATCO: a. Extend DNAC(US) plans for 60 days while Enron Newco(US) plans are put in place. b. Put new plans into place for SATCO employees. c. Transfer assets from DNAC(US) plan into Enron Newco(US). DACO (PORT ANGELES MILL) U.S. SATCO (MAINE TIMBER) U.S.

SCENARIO II – ENRON DOES NOT PURCHASE DSL(CAN) AND DSL(US) AS PART OF ACQUISITION STEP 3 DNAC (CAN) sells DFPL shares to Enron Newco(CAN) and DNAC(US) is not part of the purchase. Benefit issues for DSL(US) employees are outlined below. ENA 3RD PARTY INVESTOR 50% 50% ENW L.P. DAISHOWA JAPAN BV-1 DUTCH ENW NEWCO U.S. DNAC CAN SATCO BV-2 DUTCH CASH DFPL SHARES Benefit Issues For DSL(US) Employees: Move chosen DSL(US) employees to the Enron Newco(US) entity where SATCO employees go and a repeat steps a. – c. on Page 6 for SATCO employees. DFPL CAN NEWCO CAN DI (QUEBEC MILL) CAN