Download

1 / 10

100 likes | 368 Views

RCP Advisors, LLC. Tom Danis, Managing Principal and Co-founder RCP Advisors: Private Equity Fund-of-Funds Manager. December 9, 2008. Introduction – Discussion on Current PE Market Conditions. “The Denominator Effect” Public Markets Down Private Equity Flat? Sovereign Wealth Funds

E N D

RCP Advisors, LLC Tom Danis, Managing Principal and Co-founderRCP Advisors: Private Equity Fund-of-Funds Manager December 9, 2008

Introduction – Discussion on Current PE Market Conditions • “The Denominator Effect” • Public Markets Down • Private Equity Flat? • Sovereign Wealth Funds • Large Pools of Capital • Smart Pools of Capital? • Private Equity Fundraising Landscape • Global PE Investing – Less Attractive • Niche PE Strategies – More Attractive • Extended Fundraising Periods Expected • Recession = Opportunity for Attractive PE Vintage Year Returns

“The Denominator Effect” • PE allocations increased in 2008 - 57% of LPs plan to increase PE allocations while only 2% plan to decrease PE allocations • However, LPs have now reached / exceeded PE targets due to significant declines in non-PE portfolios • LPs above desired allocation must decide to: • Increase target PE allocation • Reduce new PE investments, including both the number of new relationships and re-up investments • Actively manage existing portfolio through secondary sales Source – Private Equity Spotlight, October 2008; Private Equity Analyst, October 2008; Buyouts Magazine, October 2008

Cash Flows Back to Investors Have Slowed • Record fundraising and investment levels in 2005 – 2007 generated rising capital call volume until the recent slowdown in 2008 • The current difficult exit environment has led to many LPs facing negative cash flows • The lack of distributions further limits LPs’ ability to make new commitments • Certain LPs have sought liquidity by selling existing fund interests in the secondary market - Secondary volume increased from $11.2 billion in 2006 and $12.2 billion in 2007 to $20.7 billion estimated for 2008 Source – VentureXpert 2008; Credit Suisse Strategic Partners

Sovereign Wealth Funds – A Growing Source of Capital • Sovereign Wealth Funds (“SWFs”) have continued to expand in size and importance • ~30 SWFs globally that manage $3.2 trillion, and expected to grow 15-20% per year for the next 5 years • Merrill Lynch estimates SWFs will invest $3.1 - $6 trillion into world stock markets in the next 5 years • SWFs have invested ~7% of AUM in PE • SWFs have been more active in direct investments than in partnerships, especially in distressed financial services • Many SWF investments in private equity have included a GP-ownership stake Source – Grant Thornton – Top Trends in Middle Market Private Equity; International Financial Services London

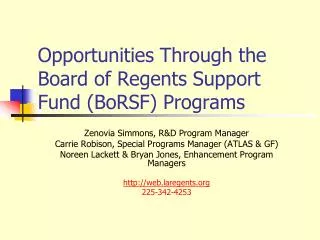

Private Equity Fundraising – LP Analysis • Global fundraising remains strong through Q3 ’08 • However, 2nd and 3rd quarters have slowed down • In addition, LPs have put decisions on hold suggesting a further slowdown in the 4th quarter • Historically, recession years have provided the attractive vintage year performance (see slide #8) • Overall fundraising is expected to fall less markedly • Demand for mega buyout / generalist funds is expected to slow down • Infrastructure, Distressed and Secondaries are experiencing strong LP demand Source – VentureXpert 2008

Private Equity Fundraising – GP Analysis • A record number of funds are seeking capital • >1,600 funds in the market seeking to raise $942 billion • $865 billion raised in 2006 & 2007 combined • Average number of months fundraising has increased: • 9.5 months in 2004 • 14.2 months in 2008 • In response to difficult marketing conditions, many GPs have lowered fund size targets or suspended fundraising efforts • Certain “First Time” funds are seeking alternative methods of raising capital Firms are “showing greater patience than they originally anticipated, settling for smaller fund sizes, finding a white knight to make early acquisitions possible and fundraising in intervals between dealmaking.” (1) Source – Private Equity Intelligence; S&P European PE Quarterly, October 2008; (1) Buyouts Magazine “Debut Fundraisers Try Range of Strategies.” September 8, 2008

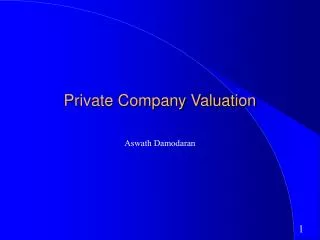

Private Equity Strategies and Investment Momentum Source – Private Equity Intelligence; (1) Private Equity Insider “New Landscape Creates Secondary Field Day” September 24, 2008

Recession Recession Buyout Fund Returns Across Economic Cycles Top Quartile Buyout Funds by Vintage Year Source – Cambridge Associates US PE Benchmarks, upper quartile net IRR calculated by vintage year as of June 30, 2008

Headquarters 100 N. Riverside PlazaSuite 2400Chicago, IL 60606T: 312.266.7300F: 312.266.7433 West Coast Office 949 South Coast DriveSuite 550 Costa Mesa, CA 92626T: 949.335.5000F: 949.335.5010 www.rcpadvisors.com