Download

1 / 15

150 likes | 304 Views

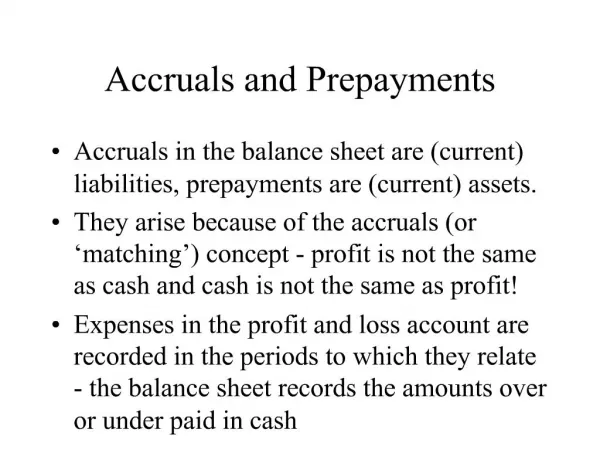

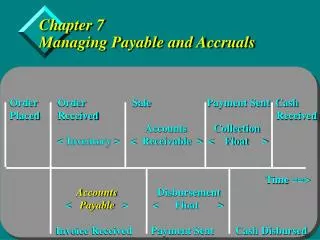

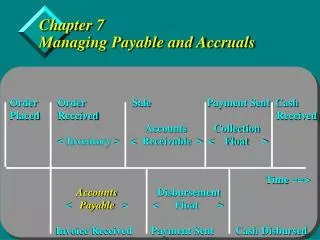

Chapter 7 Managing Payable and Accruals. Order Order Sale Payment Sent Cash Placed Received Received Accounts Collection

E N D

Chapter 7Managing Payable and Accruals • Order Order Sale Payment Sent Cash • Placed Received Received • Accounts Collection • < Inventory > < Receivable > < Float > • Time ==> • Accounts Disbursement • < Payable > < Float > • Invoice Received Payment Sent Cash Disbursed

Learning Objectives • Apply time value of money principles to the payment of accounts payable. • Decide when to take a cash discount for early payment and when to pay at the end of the credit period. • Better understand the ethical issues involved in payables behavior. • Develop appreciation for role information systems play in managing payables. • To develop effective monitoring tools.

Spontaneous Sources of Financing • Definition • a financing source occurring spontaneously from operations • Examples • payables • accruals

Accounts Payable • Open account – No need to apply for credit every time • Cash discount – Terms relative to delivery date • Prox – Terms refer to days of the following month after delivery. 2/10, prox net 30 • Seasonal dating – Used if customers have seasonal demand. 2/10, net 30, dating 90 is the same as 2/100, net 120 • Consignment – No payment required unless merchandise is sold

Payables Decisions and the Cash Flow Timeline Time ==> Purchase Cash Credit Date Discount Date Period

Basic Principles • Never pay early, pay on the last day of: • the discount period, or • the credit period • Take a cash discount when: • implied interest rate > opportunity rate • Stretch only as a last resort, not as a policy

Payment Decision Model • Three Possible Valuations • When days delayed < discount period • When days delayed > discount period • When days delayed > credit period

When Days Delayed < Discount Period • NPV = IP x (1-d) / (1 + (DD(k/365))) • IP = Invoice Price • d = Discount rate • DD = Days Delayed (days after invoice date) • k = Annual cost of capital • Note that PV would be a more appropriate designation

When Days Delayed > Discount Period • NPV = IP / (1 + (DD(k/365)))

When Days Delayed > Credit Period • IP x (1 + (DD-CP)x(fee/365))NPV = ---------------------------------- (1 + (DD(k/365))) • CP = Credit Period (days) • fee = Annual fee and intangible cost of late payment

Take or Leave a Discount • Take the cash discount if: • IP x (1-d) < IP / (1 + (CP-DP)x(k/365)) Or if • k < (d/(1-d)) x (365/(CP-DP))

Ethics and the Payment Decision Top Tier: Make a commitment of the will to enhance the well-being of our neighbors Middle Tier: The “Sun Light” test: Would both interested & impartial observers find my decision to be prudent & sound. • Lower Tier: Does the decision obey the intent and letter • of the law?

Monitoring the Payables Balance • Payables turnover approach • Period purchases / Accounts payable • Days purchases outstanding • Accounts payable / Average daily purchases • Balance fraction approach* *Gives the best picture of payables over time

Accruals • Definition • an expense that has been incurred but has not yet been paid • Two basic types • accrued wages and salaries • accrued interest and taxes

Summary • A cash discount should be taken when the investment/borrowing rate is less than the annualized discount rate. • Otherwise, pay at the end of the credit period. • Payment should not be stretched past the credit period. • The balance fraction monitoring method is preferred over the payables turnover method since turnover is influenced by purchasing trends.