Download

1 / 7

110 likes | 870 Views

Capital Asset Pricing Model (CAPM). A Case from China’s Stock Market. CAPM: A great innovation in the field of finance invented by William Sharpe (1963 1964) and John Lintner (1965 1969). Objectives: 1.The expression and meaning of the CAPM

E N D

Capital Asset Pricing Model (CAPM) A Case from China’s Stock Market

CAPM: A great innovation in the field of financeinvented by William Sharpe (1963 1964) and John Lintner (1965 1969) Objectives: 1.The expression and meaning of the CAPM 2.The methodology used to test the CAPM

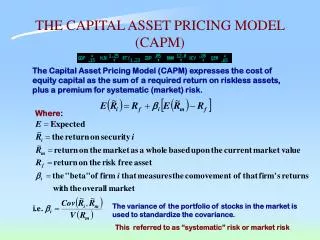

1. The Expression and Implication of the CAPM The CAPM quantifies tradeoff between risk and expected return and yields the following expression: E(Ri) = Rf + [E(Rm) – Rf]I

1.The Expression and Implication of CAPM • The essence of CAPM is that the expected return on any asset is a positive linear function of its beta and that beta is the only measure of risk needed to explain the cross-section of expected returns. • The spirit of CAPM is . No , no CAPM.

2. Methodology: Fama-MacBeth Approach The basic idea of the approach is the use of a time series (first pass) regression to estimate betas and the use of a cross–sectional (second pass) regression to test the hypothesis derived from the CAPM.

2. Methodology: Fama-MacBeth Approach • Step 1 (First-Pass Regression): For each of the N securities included in the sample, we first run the following regression over time to estimate beta: • Step 2 (Second-Pass Regression) We run the following cross-section regression over the sample period over the N securities:

2. Methodology: Fama-MacBeth Approach • 1). should not be significantly different from zero, or residual risk does not affect return. • 2). should not be significantly different from zero, or the expected return on any asset is a positive linear function of its beta. • 3). must be more than zero: there is a positive price of risk in the capital markets, namely, a positive relationship exists between systematic risk and expected return.