Download

1 / 70

720 likes | 1.02k Views

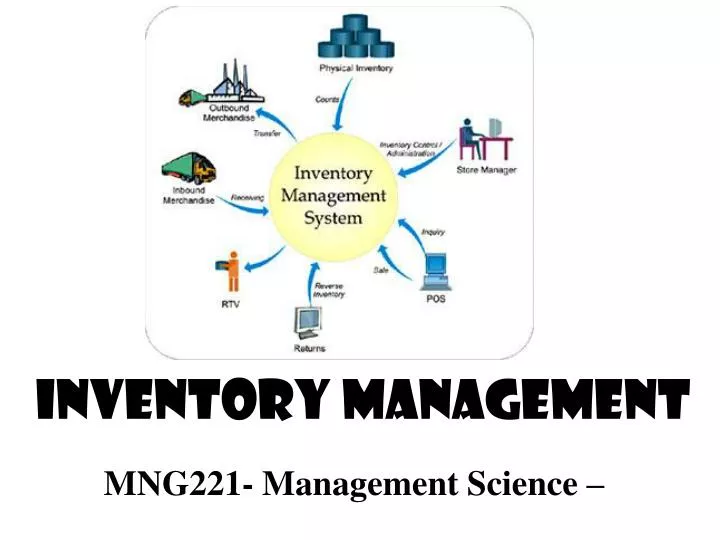

MNG221- Management Science – . Inventory Management. Lecture Outline. Types of inventory Reasons for holding inventory Stock costs Objective of inventory management Pareto analysis Deterministic and stochastic models. Inventory Management. Stock may be classified into: Raw materials

E N D

MNG221- Management Science – Inventory Management

Lecture Outline • Types of inventory • Reasons for holding inventory • Stock costs • Objective of inventory management • Pareto analysis • Deterministic and stochastic models

Inventory Management • Stock may be classified into: • Raw materials • Work-in-progress • Finished goods • Resources, Labor, Cash The classification depends on the nature of the firm.

Inventory Management • The main purpose of inventory is simply to meet customer demand. • It often represents a significant cost to a business firm, (including insurance, obsolescence, depreciation, interest, opportunity costs, storage costs, etc.) • Therefore inventory related costs can be controlled, through the management of inventory levels.

Inventory Management Elements of Inventory Management

Elements of Inventory Management • Inventoryis defined as a stock of items kept on hand by an organization to use to meet customer demand. The Role of Inventory The main reasons for holding inventory are: • To satisfy demand immediately • To meet seasonal or cyclical demand

Elements of Inventory Management The Role of Inventory • To allow for unimpeded production and provide independence between operations. • To take advantage of bulk purchasing price discounts. • To absorb seasonal fluctuations. • A necessary part of the production process.

Elements of Inventory Management The Role of Inventory (continued) • Inventory may also accumulate because of poor control methods, obsolesce and suboptimal decisions.

Elements of Inventory Management Demand • A crucial component and the basic starting point for the management of inventory is customer demand, because it exists for the purpose of meeting the demand of customers. • Customers can be Internal(machine operator) or External (Individual purchasing goods from stores)

Elements of Inventory Management Demand (Continued) • An essential determinant of effective inventory management is an accurate forecast of demand. • The demand for items in inventory is classified as dependent or independent • Dependent Demand items are used internally to produce a final product • Independent Demand items are final products demanded by an external customer.

Elements of Inventory Management Inventory Costs • There are three basic costs associated with inventory: • Carrying Costs - are the costs of holding items in storage. • Ordering Costs - are the costs associated with replenishing the stock of inventory being held.

Elements of Inventory Management Inventory Costs • Shortage costs- also referred to as stockout costs, occur when customer demand cannot be met because of insufficient inventory on hand.

Elements of Inventory Management Inventory Costs • The objective of inventory management is to employ an inventory control system that will indicate how much should be ordered and when orders should take place to minimize the sum of the above three inventory costs

Inventory Management Inventory Control Systems

Inventory Control Systems • An Inventory System is a structure for controlling the level of inventory by determining how much to order (the level of replenishment) and when to order. • There are two basic types of inventory systems: a continuous (or fixed order quantity) system and a periodic (or fixed time period) system.

Inventory Control Systems • The primary difference in the two systems is that in a: • Continuous system - an order for the same amount is placed whenever the inventory decreases to a certain level. • Periodic system - order is placed for a variable after an established passage of time.

Inventory Control Systems Continuous Inventory System • In a continuous inventory system, (alternatively referred to as a perpetual system or a fixed order quantity system) a constant amount is ordered when inventory declines to a predetermined level, referred to as the reorder point. • This fixed order quantity is called the economic order quantity

Inventory Control Systems Continuous Inventory System • The inventory level is closely and continuously monitored so that management always knows the inventory status. • However, the cost of maintaining a continual record of the amount of inventory on hand can also be a disadvantage of this type of system.

Inventory Control Systems Periodic Inventory System • In a periodic inventory system, (also referred to as a fixed time period system or periodic review system) an order is placed for a variable amount after a fixed passage of time.

Inventory Control Systems Periodic Inventory System • The inventory level is not monitored at all during the time interval between orders. • It has the advantage of requiring little or no record keeping • It has the disadvantage of less direct control

Inventory Management Economic Order Quantity ModelsBasic Model

Economic Order Quantity Models • The most widely used and traditional means for determining how much to order in a continuous system is the Economic Order Quantity (EOQ) model, also referred to as the Economic Lot Size Model. • The function of the EOQ model is to determine the optimal order size that minimizes total inventory costs.

Economic Order Quantity Models The Basic EOQ Model • It is essentially a single formula for determining the optimal order size that minimizes the sum of carrying costs and ordering costs.

Economic Order Quantity Models The Basic EOQ Model Assumptions • Demand is known with certainty and is relatively constant over time. • No shortages are allowed. • Lead time for the receipt of orders is constant. • The order quantity is received all at once.

Economic Order Quantity Models The Basic EOQ Model The Inventory Order Cycle

Economic Order Quantity Models The Basic EOQ Model • Q is the point at which ordering and carrying costs react inversely to each other in response to an increase in the order size. • R is the point at which a new order is placed with enough lead time for the reordering of stock.

Economic Order Quantity Models The Basic EOQ Model – Carrying Costs • Carrying cost is usually expressed on a per-unit basis for some period of time on an annual basis (i.e., per year), and sometimes as a percentage of average inventory. Average Inventory = Q or ∑Q points over period, t 2 number of points

Economic Order Quantity Models The Basic EOQ Model – Carrying Costs

Economic Order Quantity Models The Basic EOQ Model – Carrying Costs Thus, Carrying cost is Ordering Costs is Total Inventory Cost is The EOQ cost model

Economic Order Quantity Models The Basic EOQ Model • The Optimal Value Of Q corresponds to the lowest point on the total cost curve or the point where the ordering cost curve intersects with the carrying cost curve.

Economic Order Quantity Models The Basic EOQ Model • Thus The Optimal Value Of Q by equating the two cost functions and solving for Q, as follows:

Economic Order Quantity Models The Basic EOQ Model • Alternatively, the optimal value of Q can be determined by differentiating the total cost curve with respect to Q

Economic Order Quantity Models The Basic EOQ Model • The total minimum cost

Economic Order Quantity Models The Basic EOQ Model - Example • The I-75 Carpet Discount Store wants to determine the optimal order size and total inventory cost given an estimated annual demand of 10,000 yards of carpet, an annual carrying cost of $0.75 per yard, and an ordering cost of $150. • The store would also like to know the number of orders that will be made annually and the time between orders (i.e., the order cycle).

Economic Order Quantity Models The Basic EOQ Model – Example • The model parameters as follows:

Economic Order Quantity Models The Basic EOQ Model – Example • The optimal order size is computed as follows:

Economic Order Quantity Models The Basic EOQ Model – Example • The total annual inventory cost is determined by substituting Qopt into the total cost formula, as follows:

Economic Order Quantity Models The Basic EOQ Model – Example • The number of orders per year is computed as follows:

Economic Order Quantity Models The Basic EOQ Model – Example • Given that the store is open 311 days annually (365 days minus 52 Sundays, plus Thanksgiving and Christmas), the order cycle is determined as follows:

Economic Order Quantity Models The Basic EOQ Model • The optimal order quantity determined in general, is an approximate value, because it is based on estimates of carrying and ordering costs as well as uncertain demand. • This in practice it is acceptable to round off the Q values to the nearest whole number. • However, the EOQ model is robust; because Q is a square root, errors in the estimation of D, Cc, and Co are dampened.

Inventory Management Economic Order Quantity ModelsNon-instantaneous Model

Economic Order Quantity Models Non-instantaneous Receipt Model • A variation of the basic EOQ model is achieved when the assumption that orders are received all at once is relaxed. • It is also referred to as the Gradual Usage, or Production Lot Size, model. • In this EOQ variation, the order quantity is received gradually over time and the inventory level is depleted at the same time it is being replenished.

Economic Order Quantity Models Non-instantaneous Receipt Model • This is a situation most commonly found when the • Inventory user is also the producer • When orders are delivered gradually over time • When retailer and producer of a product are one and the same.

Economic Order Quantity Models Non-instantaneous Receipt Model The EOQ model with Non-instantaneous Order Receipt

Economic Order Quantity Models Non-instantaneous Receipt Model • The ordering cost component of the basic EOQ model does not change. • However, the carrying cost component is not the same for this model variation because average inventory is different. • The maximum inventory level is not simply Q; it is an amount somewhat lower than Q,

Economic Order Quantity Models Non-instantaneous Receipt Model • Unique parameters of this model: • p = daily rate at which the order is received over time, also known as the production rate • d = the daily rate at which inventory is demanded

Economic Order Quantity Models Non-instantaneous Receipt Model • As such, the maximum amount of inventory that is on hand is computed as follows:

Economic Order Quantity Models Non-instantaneous Receipt Model • Given the maximum inventory level, the average inventory level is determined by dividing this amount by 2, as follows:

Economic Order Quantity Models Non-instantaneous Receipt Model • The total carrying cost, using this function for average inventory, is:

Economic Order Quantity Models Non-instantaneous Receipt Model • Thus, the total annual inventory cost is determined according to the following formula: