Download

1 / 30

310 likes | 343 Views

Explore how manufacturing companies determine inventory costs, allocate overhead, and use job order and process costing systems. Learn about perpetual inventory and cost flow in production. Examine the allocation of factory overhead in manufacturing.

E N D

CHAPTER 16 PRODUCT COSTING SYSTEMS IN MANUFACTURING OPERATIONS

Chapter Overview • How does the way a manufacturing company determine the cost of its inventory and cost of goods sold differ from the way a merchandising company determines them? • How does a cost accounting system help a manufacturing company assign costs to its products? • Since factory overhead is not a physical part of the product, how does a company include the cost of overhead in the cost of its products?

Chapter Overview • Why is there more than one type of cost accounting system? • What is a job order cost accounting system, and how does a company use this system? • What is a process cost accounting system, and how does a company use this system?

Cost Accounting Systems • Cost accounting systems track the flow of manufacturing inputs through the manufacturing process. • As raw materials, direct labor, and factory overhead inputs move through the manufacturing process, the costs of manufacturing the products are accumulated. • Cost accounting systems accumulate and track this activity.

Direct materials are the raw materials that physically become part of a manufactured product Direct labor is the labor of the employees who work with the direct materials to convert or assemble them into finished products. Factory overhead includes all items, other than direct materials and direct labor, that are necessary to manufacture products. They usually cannot be traced to individual products. Relationship of Manufacturing Cost Elements of Unlimited DecadenceExhibit 16-1

Perpetual Inventory Systems • Most cost accounting system use a perpetual inventory system, maintaining a continuous record of the balance in the inventory accounts. • For a merchandiser, this simply involve increasing the inventory account for merchandiser purchases and decreasing it for merchandise sold. • In a manufacturing company, this involves all three inventory accounts: raw materials, goods-in-process, and finished goods.

Manufacturing Cost Flow • In a perpetual inventory system, the manufacturing cost flow mirrors the physical flow of goods. • For example, when direct raw materials are requisitioned to production, the raw materials account decreases for the cost of the direct raw materials and the goods-in-process account increases by a like amount. • For example, when goods are completed, goods-in-process inventory decreases for the cost of the goods manufactured and finished goods inventory increases by a like amount.

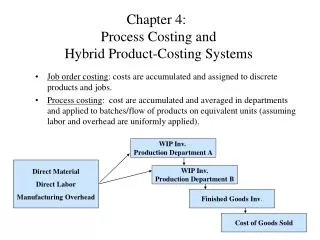

Cost Accounting Systems • Two different types of cost accounting systems are used, depending on the nature of the manufacturing process. • Job-order cost systems accumulate and track the cost of products by job. Each job is unique and easily identifiable. • Process costing systems accumulate and track the cost of products by process. Products are homogeneous and may go through one or several different processes until a finished product is obtained.

Job Order Cost Systems • When a company manufactures one unit of a unique product or manufactures a unique group of products, it treats that unit or group as a job order. • Examples of different “jobs” include a construction project, a custom set of kitchen cabinets, an audit by a public accounting firm, or the first printing of a textbook in a publishing company. • It is easy to determine when a job starts and when it ends because each job is unique.

Factory Overhead Allocation • While direct materials and direct labor are easy to track and can be assigned to jobs through the raw materials requisition and labor ticket forms, factory overhead is more difficult. • Factory overhead includes all of the indirect cost of manufacturing all jobs, such as indirect materials and labor, factory rent, depreciation, insurance and other factory operating costs. • These cost can’t be allocate on a job specific basis, but are instead allocated based on a predetermined overhead rate.

Period of time that production is in process and jobs are being finished and delivered January 1, 2004 December 31, 2004 When all overhead costs are estimated or budgeted Estimated cost have to be assigned before total costs are known Period of time that production is in process and jobs are being finished and delivered January 1, 2004 December 31, 2004 When all overhead costs are known When all overhead costs need to be assigned to jobs Timing Issues of Assigning Manufacturing Overhead

Expected factory overhead costs for the year Expected direct labor hours for the year = Predetermined overhead rate The predetermined overhead rate can be based on any activity driver, depending on the circumstances. In the case of Unlimited Decadence, the driver is direct labor hours so this what is used. Predetermined Overhead Rates • A predetermined overhead rate provides the solution to allocate overhead costs before all of the costs are finally known. • This rate is then used to assign factory overhead to jobs during the year.

Expected factory overhead costs for the year Expected direct labor hours for the year $7,584,000 2,400,000 DLH The predetermined overhead rate of $3.16 is then applied to jobs at Unlimited Decadence, based on the number of direct labor hours used in the job. Predetermined Overhead Rates = $3.16 per direct labor hour used

Assets = Liabilities + Stockholders’ Equity +$395 (Goods-in-Process inventory) The $395 is recorded in the Goods-in-Process account as well as on the supporting job cost sheet for the job (Exhibit 16-3) Recording Factory Overhead Assigned to Jobs • Using the predetermined rate of $3.16 per DLH, how would Unlimited Decadence record factory overhead for a job requiring 125 direct labor hours? • 125 hours X 3.16 = $395 – factory overhead assigned. The Factory Overhead account decreases and the Goods-in-Process account increases. -$395 (Factory overhead)

Assets = Liabilities + Stockholders’ Equity +$4,000 (Factory overhead) Recording Actual Factory Overhead Costs • As Unlimited Decadence actually incurs factory overhead costs, the factory overhead account is increased. • If $4,000 in factory utilities are incurred and paid, the Factory Overhead account increases and the Cash account decreases. -$4,000 (Cash)

Assets = Liabilities + Stockholders’ Equity +$2,980 (Finished goods inventory) The job cost sheet for Job #101 is marked finished and removed from the goods-in process supporting job records to the finished goods supporting records Recording Cost of Finished Jobs • As Unlimited Decadence completes a job, the cost must be transferred from the Goods-in-Process account to Finished Goods account. • If Job #101 is finished during the year for $2,980, how is the cost transferred? -$2,980 (Goods-in-Process inventory)

Assets = Liabilities + Stockholders’ Equity Record sale +$4,000 (Accounts receivable) -$2,980 (Finished Goods Inventory) +$4,000 (Sales Revenue) -$2,980 (+Cost of goods sold) Adjust inventory Recording Sale of Finished Goods • When Unlimited Decadence sells job #101 to the customer, two entries will be prepared under the perpetual inventory system. • If Job #101 is sold for $4,000 on account, how is this recorded?

A negative balance in the account means applied overhead was more than actual, so overhead is overapplied* Factory Overhead Account +$7,640,000 -$7,900,000 Unlimited Decadence decreased the account for costs applied based on the predetermined rate Unlimited Decadence added actual costs to the account as incurred Bal, 12/31 - $260,000 *a positive balance would mean overhead is underapplied Over (Under) Applied Factory Overhead • When a predetermined rate is used, it is based on estimates. It inevitably applies more or less than the actual factory overhead costs incurred during the year.

Assets = Liabilities + Stockholders’ Equity +$260,000 (Factory Overhead) Eliminating the Over (Under) Applied Overhead • Over (under) applied factory overhead is transferred to the cost of goods sold during the year, since its ultimate impact is on the cost of goods produced and sold. • The $260,000 of overapplied factory overhead means that job costs were overstated, so cost of goods sold is reduced for $260,000 and the negative balance in Factory Overhead is eliminated. +$260,000 (-Cost of goods sold)

Process Cost Systems • When a company manufactures large volumes of identical units of products, a process cost accounting system is used. • A process cost accounting system keeps track of the costs applied through one or more manufacturing processes until the finished product is made. Costs are accumulated by process, not by job. • In a process cost system, direct labor and factory overhead are grouped together as “conversion costs.” This becomes important when there are unfinished units in the inventory.

Process Cost Sheet for One Process (No Beginning or Ending Inventories)Exhibit 16-7

Assets = Liabilities + Stockholders’ Equity Raw Materials Inventory Goods-in-Process Inventory Factory Overhead Wages Payable (a) -$3,000 (a) +$3,000 (a) Transfer of raw materials to production (b) +$2,000 (b) +$2,000 (b) Direct labor incurred for production (c) +$2,500 (c ) -$2,500 (b) Factory overhead applied to production Conversion costs Accumulating the Cost of a Single process • How would the $7,500 in costs accumulated on the process cost sheet (Exhibit 16-7) for April be recorded?

From this, the cost assigned to each finished unit is $5.00 per unit ($2.00/gallon of average direct materials costs and $3.00/gallon average conversion costs. Assets = Liabilities + Stockholders’ Equity +$7,500 (Finished goods inventory) Transfer of Finished Process Products • One the cleaning solvent has been through the single process, it can be transferred to finished goods much the way it is done in a job cost system. -$7,500 (Goods-in-Process inventory)

Equivalent Units • Because manufacturing a product takes time and because production is continuous, often there are unfinished units in the ending Goods-in-Process Inventory account. • When this occurs, a company must modify the cost-assignment procedure to be sure that costs are assigned to both finished products and those that remain in the ending inventory. • Unfinished units do not have the same amount of cost inputs as finished units and so one method of assigning the costs does not work.

Equivalent Units • To handle this problem, a company that uses a process cost system counts each finished unit as a whole unit. • Unfinished units are counted as a part of a whole unit, that part being the estimated percent that the product is complete. • For example, if Lady Macbeth had a bottle of solvent that was 80% complete in the ending Goods-in-Process Inventory, it would be counted as 80% of a whole bottle of solvent. • When physical products in a process are counted this way, they are called equivalent units.

Costs are then assigned to 800 equivalent units, which permits per-unit costs to be assigned to completed and unfinished products in direct proportion to the amount of resources each group used. Equivalent Units • The number of equivalent units in a group of unfinished physical products is the total number of physical products times their average percentage of completion:

Lady MacBeth Process Cost Sheet(Ending Inventory)Exhibit 16-8

Lady MacBeth Process Cost Sheet(Beginning and Ending Inventory)Exhibit 16-9