Download

1 / 14

170 likes | 273 Views

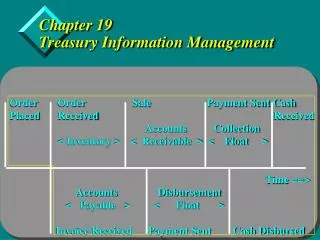

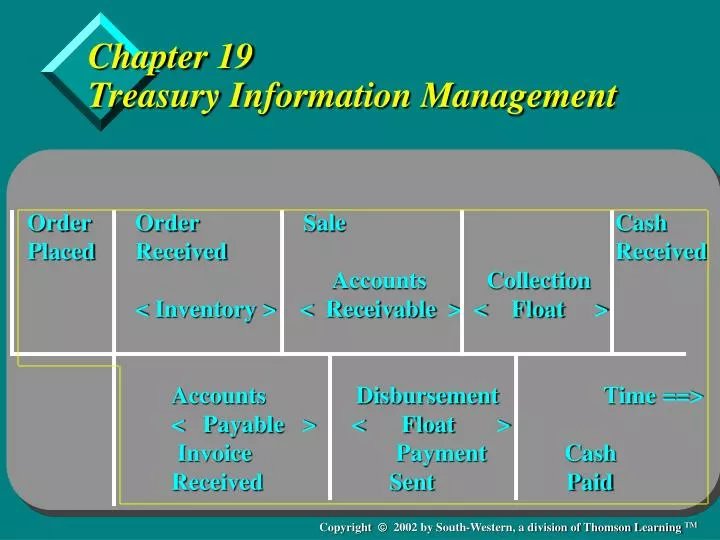

Chapter 19 Treasury Information Management. Order Order Sale Cash Placed Received Received Accounts Collection

E N D

Chapter 19Treasury Information Management • Order Order Sale Cash • Placed Received Received • Accounts Collection • < Inventory > < Receivable > < Float > • Accounts Disbursement Time ==> • < Payable > < Float > • Invoice Payment Cash • Received Sent Paid

Learning Objectives • Appreciate the benefits of e-commerce • Understand what EDI is and the issues involved in its implementation • Differentiate between the component parts of EDI • Understand the benefits of applying the Internet to e-commerce • Understand how treasury managers use information technology to make better financial decisions

Key Information Flows Strategic Level Management Level (analysis and decision support) Operations Level (data and value flows)

Electronic Data Interchange (EDI) • Electronic business data interchange, EBDI • Financial EDI, FEDI • Electronic funds transfer, EFT

EDI Communications Formats, ASC X12 Standards • 810 Invoice • 820 Payment order/remittance advice • 821 Financial information reporting • 822 Customer account analysis • 823 Lockbox information • etc.

Format Options for Funds Movement, NACHA • PPD: Direct deposit • CCD: Cash concentration and disbursement • CCD+: Same as CCD with addendum space • TXP: For express purpose of electronic tax payments • CTX: Corporate trade X12 format with variable data fields • RCK: Re-presented check entries format

How Transaction Sets and Payment Formats Are Used FOCUS ON PRACTICE General Motors’ divisions transmit remittance instructions using the ASC X12 820 format to their banks. The banks convert the 820 transmission into the CTX format, which includes both payment instructions, dollars, and invoice remittance data. At this time, not all banks can handle a CTX format. If the supplier’s bank cannot handle such a format, GM’s bank will send the payment instructions in a CCD format and will then route a printed report of the remittance data to the supplier.

Benefits and Problems with EDI • Benefits • improves quality of services to customers • employee productivity is enhanced • operations are streamlined • EDI provides for more effective asset management • EDI can improve payables area • cash management costs are reduced • banks often allow for larger credit lines • Problems • development and acceptance of standards • data communication security • legal issues

E-Commerce and the Internet • Information reporting • Transaction initiation • Image access • E-Procurement • Internet invoicing and payment • Digital marketplaces • Future role of the Internet

Auditing the Information System • Survey results • Cash flow timeline events • Assessment of a firm’s cash management practice • Assessing the treasury management workstation

Cash Flow Timeline Events • Purchasing • Accounts payable • Inventory • Sales • Receivables • Treasury • Financial administration

Assessment of Cash Management Practices • Four basic areas to assess • cash positioning/mobilization • bank relationship management • short-term investment/borrowing • treasury systems management • Each assessed on 6 key elements • level of productivity • use of advanced strategies/automation • effective internal controls • performance measurement standards • involvement in cash-related decisions company-wide • industry reputation

Assessment of Treasury Workstations • Balance reporting module • Bank information • Cash mobilization • Consolidation of information • General investment module • General debt module • Communications and system features • Vendor services and support

Summary • The chapter discussed EDI and its component parts of EBDI, FEDI, and EFT • The chapter provided a variety of check lists for auditing the short-term financial management systems