Download

1 / 11

110 likes | 254 Views

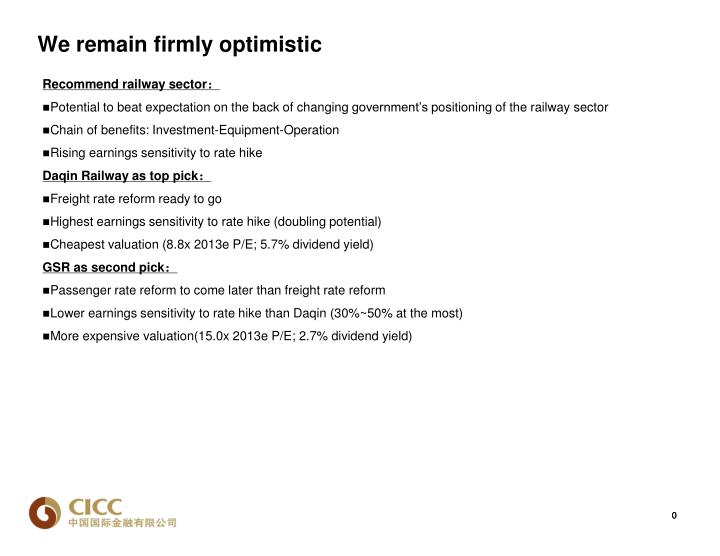

We remain firmly optimistic. Recommend railway sector : Potential to beat expectation on the back of changing government’s positioning of the railway sector Chain of benefits: Investment-Equipment-Operation Rising earnings sensitivity to rate hike Daqin Railway as top pick :

E N D

We remain firmly optimistic • Recommend railway sector: • Potential to beat expectation on the back of changing government’s positioning of the railway sector • Chain of benefits: Investment-Equipment-Operation • Rising earnings sensitivity to rate hike • Daqin Railway as top pick: • Freight rate reform ready to go • Highest earnings sensitivity to rate hike (doubling potential) • Cheapest valuation (8.8x 2013e P/E; 5.7% dividend yield) • GSR as second pick: • Passenger rate reform to come later than freight rate reform • Lower earnings sensitivity to rate hike than Daqin (30%~50% at the most) • More expensive valuation(15.0x 2013e P/E; 2.7%dividend yield) 0 0

Reform of freight rate formation mechanism:rate hike, market orientation, flexibility New mechanism:Market mechanism, upper limit based on price relations, downward adjustment allowed Old mechanism:Government control, cost plus pricing, dual-pricing Upper limit according to market-based calculation Absolute rate decided by administrative guidance Freight rate= base 1+ base 2*distance+railway construction fund + electrification surcharge Railway construction fund=rate(Rmb 0.033/FTK)*weight*distance Electrification surcharge=rate (Rmb 0.012 /FTK)*WT.*electrified distance Some joint-stock transport companies and JV railways could implement special freight rate (such as GSR and Daqin) Railway operators could make downward revision to freight rate Railway construction funds to be merged into and adjusted together with freight rate and all lines adopting universal rates would collect funds Converging special rate and general rate for lines whose special rate is simliar to the general rate(for example: Daqin line, Guangping section of Beijing-Guangzhou Line). Source :China Railway Corporation,CICC Research Source:China Railway Corporation,CICC Research

Passenger rate:later than freight rate reform,adjustment for fastest and slowest train unlikely, and 10%~20% change likely Price relation would also be adopted; adjustment for fastest and slowest train restricted due to railway’s public function and price hearings; price for other classes might rise more significantly. Passenger rate is positively related to train conditions and distance; base rate has not been changed for years Passenger rate=base rate*distance*price relation between carriage class + insurance (now abolished) + air-conditioning Price relation between carriage class:hard/ softseat: hard/softbedat 1.0: 2.0: 2.2: 3.85 Quality passenger train:new air-conditioned train could revise up rate by 50% at most • Passenger base rate has not been changed since 1995 • Structural rise for passenger rate (due to opening of HSRs, etc. Source:CICC Research Source:China Railway Corporation,CICC Research

Potential rate hike scale and earnings sensitivity Calculation of Daqin’s sensitivity to rate hike Calculation of GSR’s sensitivity to rate hike Optimal Scenario: Ordinary freight rate +Rmb0.025; Special freight rate +Rmb0.035 (converging with ordinary rate); Rmb0.033 railway construction fund returned; Long haul passenger rate +15%. Base Scenario: In 2014, ordinary freight rate +Rmb0.02, special freight rate +Rmb0.015 and no change to railway construction fund and long haul passenger rate. Conservative Scenario: In 2014, ordinary freight rate +Rmb0.015, special freight rate +Rmb0.01 and no change to railway construction fund and long haul passenger rate. Source:Company Data,CICC Research Source:Company Data,CICC Research

Catalysts:1)1Q13 results;2)3rd Plenary Session in Nov.;3)Rate hike likely to materialize in early 2014 Daqin’s 3Q13 results likely to rise >15% on low base and rate hike in this Feb. Railway and rate reform likely to get more attention during the 3rd Plenary Session in Nov. Source:Wind,CICC Research Source:CICC Research Rate hike likely to materialize after the Spring Festival (1ST Feb.). More likely to occur in April than in Feb. Source:CICC Research

Risk Analysis:1)small downside risk to traffic volume Thermal power generation accelerated and a 8%-10% growth likely in 2H13 Narrowing price spread for domestic and imported coals; thermal coal imports stay flat YoY Source:Wind,sxcoal.com,CICC Research Source:CICC Research Falling inventory in ports and power plants Source:Wind,sxcoal.com,CICC Research

Risk Analysis:2)Sound results from Shuohuang line traffic diversion pressure test;medium risk still mild Zhunchi line to start operation in 2013 Shenhua has low exposure to third-party railways and ports; Decent pressure test results from Daqin • Capacity expected to reach 30mn-50mn ton at early operation • Shenhua reduced delivery through third-party railways and ports in 1H13, but Daqin recorded stable traffic volume • The 70mn tons coal transported by Daqin unlikely to be affected much Source:Company Data,CICC Research Insufficient port capacity to check traffic diversion from Shenhua Source:Company Data,CICC Research Source:Company Data,CICC Research

Risk Analysis:3)Controllable diversion from other lines Source:Company Data,CICC Research

Risk Analysis:4)Traffic diversion pressure ahead in 2H14 • GSR expects Futian Station of Guangzhou-Shenzhen High-speed Railway to start operation in 2H14. • We do not expect much traffic diversion before the opening of Futian Station, but a 5% decline in traffic volume in 2H14 would negatively affect GSR’s earnings by ~8%. To be open in 2H14 Estimated traffic diversion from GSHR Source: Company data, CICC research

Historical PE/PB Band Daqin Railway GSR Tielong Container Logistics