Download

1 / 19

190 likes | 372 Views

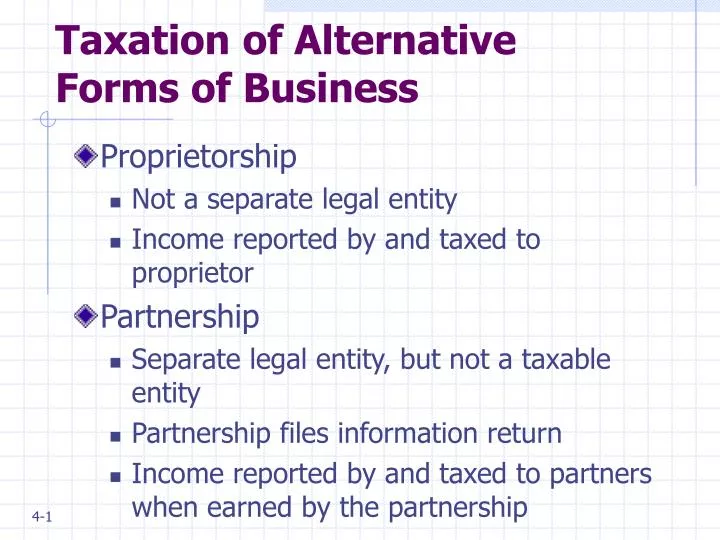

Taxation of Alternative Forms of Business. Proprietorship Not a separate legal entity Income reported by and taxed to proprietor Partnership Separate legal entity, but not a taxable entity Partnership files information return

E N D

Taxation of Alternative Forms of Business • Proprietorship • Not a separate legal entity • Income reported by and taxed to proprietor • Partnership • Separate legal entity, but not a taxable entity • Partnership files information return • Income reported by and taxed to partners when earned by the partnership

Taxation of Alternative Forms of Business continued • Corporation • Separate legal entity • C corporation • Taxable entity – income reported by and taxed to the corporation • Dividend distributions are not deductible by the corporation, and are taxable income to the recipient shareholders • Increases in value of shares taxed as capital gains when stock is sold

Taxation of Alternative Forms of Business continued • S corporation • Not a taxable entity – files an information return • Income reported by and taxed to shareholders when earned by the corporation • Limited to 75 non-corporate shareholders • Limited Liability Company (LLC) • Generally elect to be taxed as partnerships

Calculating After-Tax Business Accumulations • Some more notation • tp = partner-level tax rate on ordinary income • tc = corporate income tax rate • Rp = before-tax return on partnership investment • rp = after-tax rate of return on partnership earnings = Rp(1 – tp) • Rc = before-tax return on corporate investment • rc = after-corporate-level-tax (but before shareholder-level tax) rate of return on corporate earnings = Rc(1 – tc) • ts = effective annualized tax rate on shares

After-Tax Partnership Accumulation • Assume that partnership distributes cash each year to the partners sufficient to pay tax, then reinvests remaining after-tax earnings for n periods, then liquidates • After-tax accumulation = $I[1 + Rp(1-tp)]n(same as IV1 from Chapter 3)

After-Tax Corporate Accumulation • Assume that corporation makes no dividend distributions; it reinvests all after-corporate-tax earnings for n periods, then liquidates • After-tax accumulation = $I[1 + Rc(1 – tc)]n (1-tcg) + tcg$I(similar to IV2 from Chapter 3)

Choice of Partnership or Corporate Form • Assuming Rp = Rc, difference in after-tax accumulations depends on tp, tc, tcg, and n • If tp = tc and tcg = 0, after-tax accumulations are identical • If tp = tc and tcg > 0, the partnership form dominates the corporate form for all n • If tp > tc and tcg = 0, the corporate form dominates the partnership form for all n • If tp > tc and tcg > 0, either form may be preferred

Choice of Form continued • Why might Rp Rc? • Liability issues • Administrative and reporting cost differences • Access to capital • Owner control over management

Comparing Partnership and Corporate Forms when Rp Rc • One approach: find a rate of return to corporate form at which investor is indifferent • rc* = {[(1+rp)n – tcg]/(1 – tcg)}1/n – 1 • For any given set of tax rate variables and time horizon, can solve for rc* using the above formula. Then solve for the required before-tax rate of return, Rc*, using: Rc* (1 – tc) = rc* • For any Rc > Rc*, corporate form preferred; otherwise, partnership form preferred

Example • Let Rp = 10%, tp = 40%, tc = 35%, tcg = 20%, and n = 5. Then rp = 10%(1 - 40%) = 6% • rc* = {[1.065 - .20]/(1-.20)}1/5 –1 = 0.073 or 7.3% • Rc* = 7.3%/(1 - .35) yields Rc* = 11.2% • Interpretation: The corporation must produce a before-tax rate of return 1.2% higher than the partnership, to overcome its tax disadvantage

Example continued • Suppose n = 25. • rc* = {[1.0625 - .20]/(1-.20)}1/25 –1 = 0.067 or 6.7% • Rc* = 10.3% • Interpretation: Over a longer time horizon, the tax deferral of the lower capital gains tax on the corporate liquidation becomes more valuable, and the required corporate before-tax rate of return is only .3% higher than the partnership return

Example continued • Finally, suppose n = 50 • rc* = {[1.0650 - .20]/(1-.20)}1/50 –1 = 0.064 or 6.4% • Rc* = 9.8% • Interpretation: Over a very long time horizon, the corporation is preferred to the partnership even with a lower before-tax return. Why? The annual corporate tax rate is lower than the annual partnership tax rate, and the capital gains tax is deferred 50 years.

Effective Annualized Tax Rate on Shares • Example showed that increased deferral of capital gains taxation reduces the required corporate return • One way to calculate the impact of such deferral is the effective annual tax rate – the rate of annual taxation on increased corporate value at which the shareholder would end up with the same after-tax accumulation • ts = 1 – rp/rc*

Example continued • When n = 5, rc* = 7.3%, and ts = 1 - .06/.073 = 17.8% • When n = 25, rc* = 6.7%, and ts = 1 - .06/.067 = 10.4% • When n = 50, rc* = 6.4%, and ts = 1 - .06/.064 = 6.3% • Interpretation?

Comparisons of Corporate and Partnership Forms over Time • Review Table 4.4 in text • How were these numbers calculated? • I would use: • rc* = {[(1+rp)n – tcg]/(1 – tcg)}1/n – 1 • Rc* = rc*/ (1 – tc)

Required Corporate Return with Dividends • Recall our initial assumption that the corporation pays no dividends • Would we expect the payment of dividends to increase or decrease the required corporate rate of return, relative to the partnership? Why? • We can incorporate dividends into the equation for rc*, but we won’t do so

Other Complications • Corporate and individual tax rates are not constant • Vary across taxpayers, given progressive rate structures • Vary across time • Rates of return are not constant over time • Corporate net operating losses and carryback/carryover rules affect timing of taxation

Other Complications continued • Different types of investors have different tax characteristics and thus different rates • Fully taxable individual investors • Tax-exempt investors (pension funds, non-profit organizations) • Corporations • Foreign investors • Broker-dealers

Other Organizational Forms and Their Tax Characteristics • Foreign subsidiaries • Closely held corporations • Not-for-profit corporations • Tax-imputation corporations • REITs • REMICs