Download

1 / 20

290 likes | 866 Views

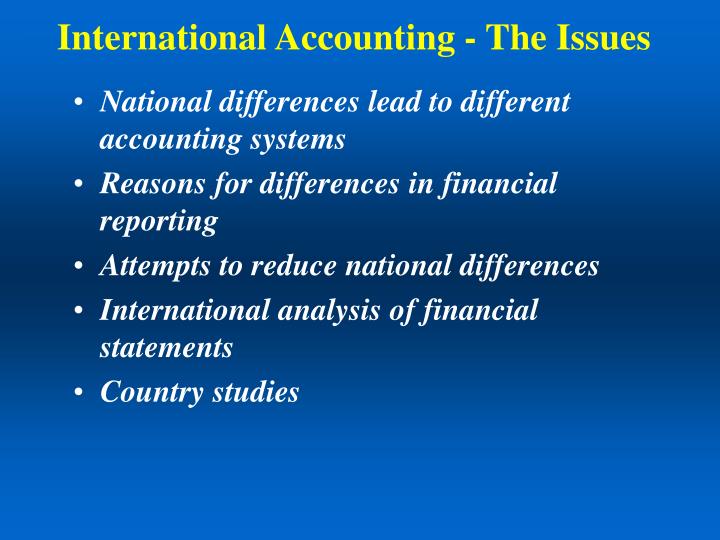

International Accounting - The Issues. National differences lead to different accounting systems Reasons for differences in financial reporting Attempts to reduce national differences International analysis of financial statements Country studies.

E N D

International Accounting - The Issues • National differences lead to different accounting systems • Reasons for differences in financial reporting • Attempts to reduce national differences • International analysis of financial statements • Country studies

National differences lead to different accounting systems • Importance of family • Family run businesses(e.g. France) • Maximisation of profit not necessarily the main priority • The firm has a responsibility to society (e.g. Germany) • Separation of ownership and control • Need for a “true and fair view” (e.g. UK)

Why do Accounting Systems Vary from Country to Country? • The national legal system • The way in which industry is financed • The relationship between the tax and the reporting systems • The influence and status of the accounting profession • The extent to which accounting theory is developed • Accidents of history • Language

The national legal system • Roman law system • set of defined rules • code of accounts • little flexibility • Common law system • encourages flexibility • case law • companies acts - true and fair view • in 1981 the European Fourth Directive was incorporated into UK companies legislation • a specified format of accounts for the first time

The way in which industry is financed • USA, UK, and Sweden • heavy reliance on individual investors (equity) • registered shareholders • active stock markets developed • need for stewardship accounting • France and Germany • much less equity investment • more loan capital • heavy bank involvement • bearer shares

The relationship between the tax and the reporting systems • USA and UK • separate rules for computing taxable profit and profit for financial reporting purposes • tax rules more prescriptive • financial reporting rules require more disclosure • France and Germany • tax rules effectively become the financial reporting rules

The influence and status of the accounting profession • Development of capital markets leads to the development of the accountancy profession • The need for audit in an advanced capital market environment • accountants held in high esteem • In countries where capital markets have not developed (Eastern Europe) accountants seen as book-keepers • Accountancy profession develops accounting standards

The extent to which accounting theory is developed • Accounting theory can influence accounting practice • Theory may be developed at an academic or practice level • Netherlands - accountants receive both academic and professional training • UK - too many practising accountants see academic development as irrelevant to practice

Accidents of history • Occupation during war • Membership of the EU • Effects of scandals associated with company failures

Language • Difficulty in translating concepts from one language to another

Australia Canada France Germany Ireland Japan Mexico Netherlands UK USA IASC established in 1973 by the accounting professions in:( now the IASB )

International Accounting StandardsInternational Financial Reporting Standards Support around the world

Some countries that have adopted IASs / IFRSs • Kenya • Kuwait • Malta

Austria Belgium Germany France Finland Italy Luxembourg Russia Switzerland Some countries that have permitted listed companies to prepare their consolidated accounts in accordance with IASs / IFRSs

Some countries that have permitted foreign listed companies to apply IASs / IFRSs without reconciliation to national GAAP • Netherlands • New Zealand • Norway • South Africa • Sweden

Some countries that have permitted companies to apply IASs / IFRSs provided there is a reconciliation to national GAAP • Denmark • Hong Kong • Poland • Spain • USA

Some countries that have taken IASs / IFRSs into account when formulating their own financial reporting standards • Australia • Malaysia • Singapore • Sri Lanka • UK

A strong desire for international harmonisation • Reduce costs for the preparation of accounts • Reduce pressure on auditors • Reduce criticisms of financial regulators • Improve decision usefulness for investors

International Analysis of Financial Statements • Language • Format and extent of disclosure • Currency • Valuation and profit measurement • Taxation

Major financial reporting issues • Accounting for groups of companies • Accounting for assets • Accounting for inventories • Substance over form • Capital instruments • Accounting for employee costs