Download

1 / 113

1.36k likes | 2.24k Views

Engineering Economics. Prof.Dr. Cengiz Kahraman ITU Industrial Engineering Department. Engineering Economics. Interest Tables In order to simplify the routine engineering economy calculations involving the factors, tables of factor values are prepared for some certain interest rates:

E N D

Engineering Economics Prof.Dr. Cengiz Kahraman ITU Industrial Engineering Department

Engineering Economics • Interest Tables • In order to simplify the routine engineering economy calculations involving the factors, tables of factor values are prepared for some certain interest rates: • 1-Discrete Tables • 2-Continuous Tables

Engineering Economics • Compound Interest Rates 1- Nominal Interest Rate • Nominal interest is the annual interest rate without considering the effect of any compounding. where • interest rate / interest period • m = number of compoundings per year

Engineering Economics 2- Effective Interest Rate (EIR) • Effective interest is the annual interest rate , taking into account the effect of compounding during the year. where • im = interest rate / interest period • m = number of compoundings per year

Engineering Economics • Example: • Consider the situation if a person deposited $100 in a bank that pays 5% interest, compounded semi-annually. How much would be in the savings account at the end of one year? • Solution: • 5% interest, compounded semi-annually, means that the bank pays 2.5% every six months. • The total money at the end of one year is • What annual interest rate yields the same amount of money, $105.06?

Engineering Economics takes into account the effect of compounding during the year. So, it is EIR. 5% interest, compounded semi-annually does not take into account the effect of compounding during the year. So, it is NIR.

Engineering Economics • Using the formulas of EIR and NIR, • Example: • If a savings bank pays 1.5% interest every three months, what are the nominal and the effective interest rates? (NIR=6%, EIR=6.1%) • Example: • An engineer deposits $1,000 in a savings account at the end of each year. If the bank pays interest at the rate of 6% per year, compounded quarterly, how much money will have accumulated in the account after 5 years? ($5,652.40)

Engineering Economics • Interpolation • Sometimes it is necessary to locate a factor value for an interest rate i or number of periods n that is not in the interest tables. When this occurs, the desired factor value can be obtained in one of two ways: 1- by using the formulas, or 2- by interpolating between the tabulated values. • The value obtained through interpolation is not exactly the correct value, since we are linearly interpreting nonlinear equations. • Nevertheless, interpolation is acceptable and is considered sufficient in most cases as long as the values of i or n are not too distant from each other.

Engineering Economics • Example: • Determine the value of the A/P factor for an interest rate of 7.3% and n of 10 years, that is, . • Solution: • We have the following situation: • The correct factor value is 0.144358.

Engineering Economics • Example: • A university credit union advertises that its interest rate on loans is 1% per month. Calculate the effective annual interest rate and use the interest factor tables to find the corresponding P/F factor for n=8 years. • The interpolated value is 0.3858 while the correct factor value is 0.3848.

Engineering Economics • Periods • Adjusting Periods • To use interest tables, the payment and compounding periods must agree. • Single Payment Factor Requirements • i and n must be in agreement • If not, either ior n must be adjusted

Engineering Economics • Adjusting Uniform Series • If payment period (PP) and compounding period (CP) agree, solve as usual. • If CP is more frequent than PP • Find the effective i for the PP • Count the number of PP's and use as n • Use values in Standard Factor Notation • If PP's are more frequent than CP's, no interest is paid.

Engineering Economics • Continuous Compounding • Continuous compounding can be thought of as a limiting case of the multiple-compounding situation. If we define r as the nominal annual interest rate and m as the number of interest periods per year, then the interest rate per interest period and the number of interest periods in n years is mn. The single payment compound amount formula may be rewritten as

Engineering Economics:Continuous Compounding • If we increase m, the number of interest periods Per year, without limit, m becomes very large and approaches infinity and r/m becomes very small and approaches zero.This is the condition of continuous compounding, that is, where the duration of the interest period decreases from some finite duration to an infinitely small duration dt and the number of interest periods Per year becomes infinite. In this situation of continuous compounding: • and

Engineering Economics:Continuous Compounding • This is the continuous compounding single payment compound amount formula. The continuous compounding single payment present worth formula is . • Example: A bank offers to sell savings certificates that will pay the purchaser $5,000 at the end of ten years, but will pay nothing to the purchaser in the meantime. If interest is computed at 6% compounded continuously, at what price is the bank selling the certificates?

Engineering Economics:Continuous Compounding • Solution: • F=$5,000 r=0.06 n=10 years Therefore, the bank is selling the $5,000 certificates for $2,744.

Engineering Economics:Continuous Compounding • Discrete Payments • If interest is compounded continuously but payments are made annually, we can use the formulas given below:

Engineering Economics:Continuous Compounding • Example: A savings account earns interest at the rate of 6% Per year, compounded continuously. How much money must initially be placed in the account to provide for twenty end-of-year withdrawals, if the first withdrawal is $1,000 and each subsequent withdrawal increases by $200?

Engineering Economics:Continuous Compounding • Solution:

Engineering Economics:Continuous Compounding • Continuous Payments • The other version of continuous compounding occurs when the total payment for 1 year is received in continuous, small, equal payments during that year.

Engineering Economics:Continuous Compounding • Example: • At what rate must funds be continuously added to a savings account in order to accumulate $10,000 in 15 years, if interest is paid at 5%Per year, compounded annually? • Solution • per year. • $447.63 must flow uniformly into the account each year.

Engineering Economics:Continuous Compounding • Example: • What effective annual interest rate corresponds to a nominal interest rate of 10% per year, compounded continuously? (Answer:10.52%) • Example: • Suppose that $2,000 is deposited each year, on a continuous basis, into a savings account that pays 6% per year, compounded continuously. How much money will have accumulated after 12 years? (Answer: $35,147.77)

Measures of Merit • Present Worth • Annual Worth • Future Worth • Internal Rate of Return • External Rate of Return • Benefit / Cost Ratio • Capitalized Cost • Payback Period

Present Worth Analysis • Most Popular Measure. • Other Names • Discounted Cash Flow Method • Discount Rate • Present Value • Net Present Value • Present worth analysis is most frequently used to determine the present value of future money receipts and disbursements. • The present worth (PW) or present value (PV) of a given series of cash flows is the equivalent value of the cash flows at the end of year 0 (i.e., at the beginning of year 1).

Net Present Worth • Net present worth = present worth of benefits – present worth of cost • NPW = PW of benefits – PW of cost • If NPW 0, the requested rate of return is met or exceeded and the alternative is financially viable.

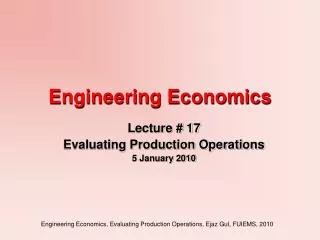

Net Present Worth Plot • Typical NPW Plot for an Investment • The NPW – i function of a cash flow representing an investment followed by benefits from the investment.

Net Present Worth Plot Typical NPW Plot for an Investment NPW i

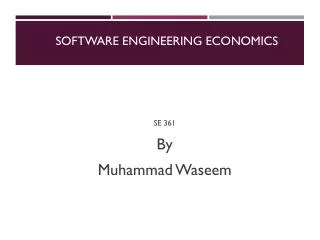

Net Present Worth Plot • Typical NPW Plot for Borrowed Money • There is a receipt of borrowed money early in the time period with a later repayment of an equal sum plus payment of interest on the borrowed money.

Net Present Worth Plot • Typical NPW Plot for Borrowed Money NPW i

Net Present Worth • ECONOMIC CRITERIA • One of the easiest ways to compare mutually exclusive alternatives is to resolve their consequences to the present time. The three criteria for economic efficiency are presented in the following table:

Net Present Worth • Analysis Period Situations • In present worth analysis careful consideration must be given to the time period covered by the analysis. There are three different analysis period situations encountered in economic analysis problems: 1-The useful life of each alternative equals the analysis period. 2-The alternatives have useful lives different from the analysis period. 3-There is an infinite analysis period.

Net Present Worth 1- The useful life of each alternative equals the analysis period • Example: • Make a present –worth comparison of the equal-service machines for which the costs are shown below, if i=10% per year.

Net Present Worth The useful life of each alternative equals the analysis period Solution: • Situation : Fixed output • Criterion : Minimize the inputs • The cash-flow diagram is left to you. The PW of each machine is calculated as follows: • Type A is selected, since the PW of costs for A are less. Note the plus sign on the salvage value, since it is a receipt.

Net Present Worth • The alternatives have useful lives different from the analysis period • The alternatives must be compared over the same number of years. The equal-service requirement can be satisfied by either of two approaches: 1- Compare the alternatives over a period of time equal to the least common multiple (LCM) for their lives. • This procedure requires some assumptions be made about the alternatives in their subsequent life cycles:

Net Present Worth • The alternatives have useful lives different from the analysis period • The alternatives under consideration will be needed for the least common multiple of years or more. • The respective costs of the alternatives will be the same in all subsequent life cycles as they were in the first one.

Net Present Worth • The alternatives have useful lives different from the analysis period 2- Compare the alternatives using a study period of length n years, which does not necessarily take into consideration the lives of the alternatives. This is also called the planning horizon approach. • Select a time horizon. • Ignore any cash occured beyond the stated horizon. • Estimate a realistic salvage value at the end of the study period for both alternatives.

The alternatives have useful lives different from the analysis period • Example: • A plant superintendent is trying to decide between two excavating machines with the estimates presented below. • Salvage value of A =$1000 and of B =$2000. • Determine which one should be selected on the basis of a present-worth comparison using an interest rate of 15% per year? ( , ) • If a study period of 5 years is specified and the salvage values are not expected to change, which alternative should be selected? ( ; ) • Which machine should be selected over a 6-year horizon if the salvage value of machine B is estimated to be $6,000 after 6 years? ( ; )

Present Worth Analysis • There is an infinite analysis period. • Some Definitions for Capitalized Cost • Capitalized cost (CC) refers to the present worth of a project that is assumed to last forever. • The sum of the first cost and the present worth of disbursements assumed to last forever is called a capitalized cost. • Capitalized cost is the present worth of a perpetual cash-flow sequence. • Some public works projects such as dams, irrigation systems, railways, tunnels, pipelines, and railroads fall into this category. • Equation for capitalized cost is derived from the factor when . As n approaches , becomes

Present Worth Analysis: Infinite analysis period. • Example: • Calculate the capitalized cost of a project that has an initial cost of $150,000 and an additional investment cost of $50,000 after 10 years. The annual operating cost will be $5,000 for the first 4 years and $8,000 thereafter. In addition, there is expected to be a recurring major rework cost of $15,000 every 13 years.Assume that i=15% per year. (Answer: $210,043) • Example: • A $500,000 gift was bequeathed to a city for the construction and continued upkeep of a music shell. Annual maintenance for a shell is estimated at $15,000. In addition, $25,000 will be needed every 10 years for painting and major repairs. How much will be left for the initial construction costs, after funds are allocated for perpetual upkeep? Deposited funds can earn 6 percent annual interest, and these returns are not subject to taxes. (Answer: $218,387)

Engieering Economics:Annual Cash Flow Analysis • Annual Cash Flow Analysis • The second of the three major analysis techniques. • In present worth analysis we resolved an alternative into an equivalent cash sum. This might have been an equivalent present worth of cost, an equivalent present worth of benefit, or an equivalent net present worth. But instead of of computing equivalent present sums we could compare alternatives based on their equivalent annual cash flows. Depending on the particular situation we may wish to compute the equivalent uniform annual cost (EUAC), the equivalent uniform annual benefit (EUAB), or their difference (EUAB-EUAC). • In annual cash flow analysis, the goal will be to convert money to an equivalent uniform annual cost or benefit. • Example: A woman bought $1,000 wort of furniture for her home. If she expects it to last ten years, what will be her equivalent uniform annual cost if interest is 7%?

Engieering Economics:Annual Cash Flow Analysis • Equivalent uniform annual cost = • Treatment of Salvage Value • In a situation where there is a salvage value, or future value at the end of the useful life of an asset, the result is to decrease the equivalent uniform annual cost. • In this case, the equivalent uniform annual cost may be solved by any of three different calculations:

Engieering Economics:Annual Cash Flow Analysis • EUAC = • The relationship above may be modified by using the equation: • Substituting this into the first equation, we obtain:

Engieering Economics:Annual Cash Flow Analysis • Or • 3. • Example: Bill owned a car for five years. One day he wondered what his uniform annual cost for maintenance and repairs had been. He assembled the following data.

Engieering Economics:Annual Cash Flow Analysis • There is a direct relationship between the present worth of cost and the equivalent uniform annual cost. It is

Engieering Economics:Annual Cash Flow Analysis • ECONOMIC CRITERIA • One of the easiest ways to compare mutually exclusive alternatives is to resolve their consequences to the equivalent uniform annual worth. The three criteria for economic efficiency are presented in the following table:

Engieering Economics:Annual Cash Flow Analysis • ECONOMIC CRITERIA

Engieering Economics:Annual Cash Flow Analysis • Example: A firm is considering which of two devices to install to reduce costs in a particular situation. Both devices cost $1,000 and have useful lives of five years and no salvage value. Device A can be expected to result in $300 savings annually. Device B will provide cost savings of $400 the first year, but will decline $50 annually, making the second year savings $350, the third year savings $300, and so forth. With interest at 7% which device should the firm purchase?

Engieering Economics:Annual Cash Flow Analysis • Solution:Device A: EUAB =$300 • Device B : EUAB =$306.75 • Select B. • Example:Three alternatives are being considered for improving an operation on the assembly line. The cost of the equipment varies as do their annual benefits compared to the present situation. Each of the alternatives has a ten-year life and a scrap value equal to 10% of its original cost.

Engieering Economics:Annual Cash Flow Analysis If interest is 8%, which alternative, if any, should be adopted? Answer: Select A.