Download

1 / 28

280 likes | 497 Views

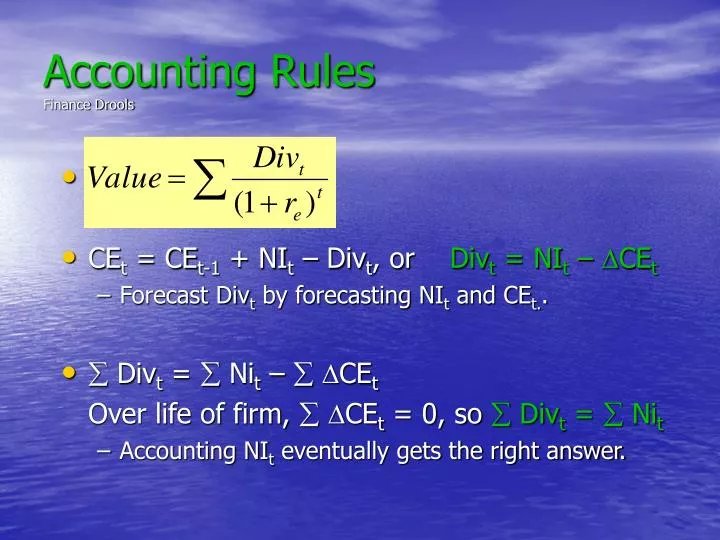

Accounting Rules Finance Drools. CE t = CE t-1 + NI t – Div t , or Div t = NI t – D CE t Forecast Div t by forecasting NI t and CE t. . Div t = Ni t – D CE t Over life of firm, D CE t = 0, so Div t = Ni t

E N D

Accounting RulesFinance Drools • CEt = CEt-1 + NIt – Divt, or Divt = NIt – DCEt • Forecast Divt by forecasting NIt and CEt.. • Divt = Nit – DCEt Over life of firm, DCEt = 0, so Divt = Nit • Accounting NIt eventually gets the right answer.

BC Accounting Analysis • What are the accounting distortions in BC’s financial statements? • How can we correct them? • When will the distortions reverse?

Consolidating the ADs Chicken Sales Note Receivables royalties interest ADs BC fictitious consolidated entity

Gain of issuance of ENBC stock • $38.2M gain on sale of sub’s stock Cash (+ asset) 135.4 Minority Interest (+ liab.) 97.2 Gain (+ equity plug) 38.2

Conversion of MidAtlantic, NJ and ENBC loans to equity page 37 of 10K Also states on pg 7 that $30M loan to MidA was converted in deal

Conversion of MidAtlantic, NJ and ENBC loans to equity goodwill (81.4+110) 191.5M Assets (plug) 130.2M Equity (in MidA deal) 15.0 Debt (promissory note in MidA deal) 6.8 3rd party debt (38.5 MidA +1.1 NJ) 39.6 Cash (13.4 in NJ and 45.9 in ENBC) 59.3 Note receivable (120 ENBC + 30 MidA) 150.0 Minority Interest (see below) 51.0 MI is 153 at year end. Need to back out the MI earnings on income statement of 5.2M and the effect of the ENBC stock issuance of 97.2M. 321.7

Remove the gain on sale of ENBC stock and write off $191 in goodwill from conversions/acquisitions.

What Happened in the company stores? December 29, 1996 December 28, 1997 ----------------------------- ----------------------------- Number of Company stores at year end...................... 104 306 Net weekly revenue per store for the year. $ 23,643 $ 20,181 Net sales......................... $ 73,512.7 100.0% $231,248.4 100.0% Food and paper costs.............. 27,441.7 37.3% 84,666.3 36.6% Salaries and benefits............. 18,470.6 25.1% 58,197.9 25.2% Operating expenses................ 5,656.8 7.7% 22,250.3 9.6% Occupancy and advertising costs... 8,080.8 11.0% 31,303.5 13.5% ---------- -------- ---------- -------- Store cash flow................... $ 13,862.8 18.9% $ 34,830.4 15.1% ========== ======== ========== ========

Exploiting Information in Accruals • Accruals represent the difference between earnings and cash flows, so earnings consists of an ‘accrual component’ and a ‘cash flow component’. • In long run, earnings = cash flows and accruals=0. • Accruals are based on estimates and therefore are susceptible to manipulation.

Measuring Operating Accruals Prepaid legal SCF 1998 1997 • Operating Accruals = (NI – CFO) deflated by total assets, so Operating Accruals = (NI – CFO)/TA • examples of manipulation? Operating accruals = (30-10)/[(167+105)/2] = 15%

Earnings Performance Mean Reverts Slowly Sloan (1996)

But Earnings Performance Without Cash Performance Mean Reverts Quickly Operating Accruals = (NI – CFO)/TA

Do Investors Use the Information In Cash Flows to Evaluate the Quality of Earnings?

What Should You Watch Out For? Average Earnings and Cash Flow Performance of Firms Sanctioned by the SEC for Manipulating Earnings (Manipulation Occurs in Year 0)

Would Operating Accruals have identified Boston Chicken’s distortion? Boston Chicken, 1996 average noncash Net Operating Assets = $930,534k, so DnonCurrentOperatingAssets/noncashNetOperatingAssets = 525,025/930,534 = 56%.

A Comprehensive Analysis of Accruals • total accruals = accounting income – cash income = NI - (net dividends + Dcash) = DCE – Dcash = (DAssets – Dcash) – DLiabilities • total accruals = DNoncash Net Operating Assets + DNet Financial Assets (i.e. mkt securities less debt) • total accruals = DNon-Cash Working Capital + DNon-Current Net Operating Assets + DNet Financial Assets

Future Stock Returns and Accrual Decomposition Richardson, Sloan, Soliman, Tuna (2002)

How big is a big accrual? on page 121 in textbook

why are net operating assets growing? which cause of NOA growth is best? which is the worst?

Future Stock Returns and Accrual Decomposition II Richardson, Sloan, Soliman, Tuna (2002)