Download

1 / 20

210 likes | 420 Views

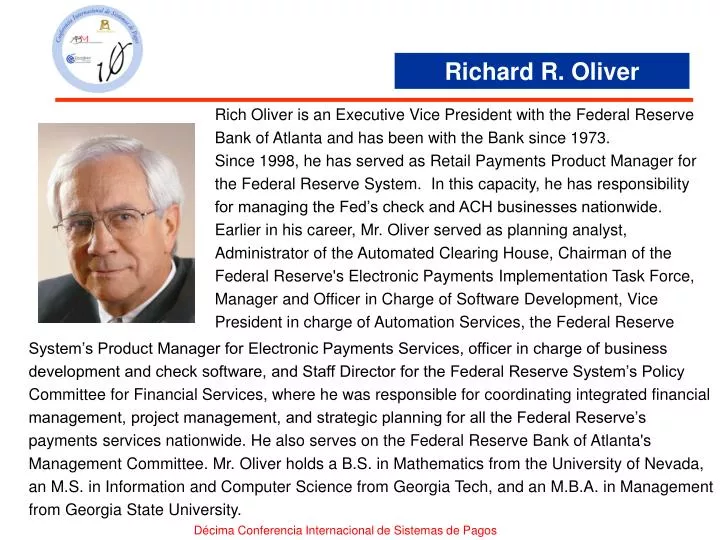

Richard R. Oliver. Rich Oliver is an Executive Vice President with the Federal Reserve Bank of Atlanta and has been with the Bank since 1973.

E N D

Richard R. Oliver Rich Oliver is an Executive Vice President with the Federal Reserve Bank of Atlanta and has been with the Bank since 1973. Since 1998, he has served as Retail Payments Product Manager for the Federal Reserve System. In this capacity, he has responsibility for managing the Fed’s check and ACH businesses nationwide. Earlier in his career, Mr. Oliver served as planning analyst, Administrator of the Automated Clearing House, Chairman of the Federal Reserve's Electronic Payments Implementation Task Force, Manager and Officer in Charge of Software Development, Vice President in charge of Automation Services, the Federal Reserve System’s Product Manager for Electronic Payments Services, officer in charge of business development and check software, and Staff Director for the Federal Reserve System’s Policy Committee for Financial Services, where he was responsible for coordinating integrated financial management, project management, and strategic planning for all the Federal Reserve’s payments services nationwide. He also serves on the Federal Reserve Bank of Atlanta's Management Committee. Mr. Oliver holds a B.S. in Mathematics from the University of Nevada, an M.S. in Information and Computer Science from Georgia Tech, and an M.B.A. in Management from Georgia State University. Décima Conferencia Internacional de Sistemas de Pagos

Current Situation of the Retail Payment System in the USA -The 2007 Federal Reserve Payments Study- Richard Oliver Executive Vice President, Federal Reserve Bank of Atlanta Federal Reserve Retail Payments Product Office Décima Conferencia Internacional de Sistemas de Pagos Ciudad de México, 12 y 13 de Mayo 2008

Payments in the United StatesHistorical Perspective Current Situation of the Retail Payment System in the USA • Checks and credit cards were the main types of non-cash retail payments in the United States until the 1970s when ATM and Automated Clearing House (ACH) options evolved nationwide • Debit cards became popular in the late 1990s • All payments alternatives grew continuously until the late 1990s • The pace of change has been slow Décima Conferencia Internacional de Sistemas de Pagos

Current Situation of the Retail Payment System in the USA Managing More Rapid Change • As the pace of change became faster, business profitability became more challenging • No accurate studies of the payments system as a whole, and the check system more specifically, had been done since 1979 • In 2000, the Federal Reserve, as the largest processor of check and ACH payments, decided to conduct a valid study and share the results with the whole industry Décima Conferencia Internacional de Sistemas de Pagos

Current Situation of the Retail Payment System in the USA Purpose of Study • Define and understand recent trends in the use of noncash retail payment instruments • Estimate the annual number and value of check and electronic payments in the United States • Better understand the composition of the check market (who writes checks to whom and why) • Measure the pace of migration from paper-based to electronic payments Décima Conferencia Internacional de Sistemas de Pagos

Current Situation of the Retail Payment System in the USA Scope and Methodology • The 2007 Payments Study included three research efforts: A Depository Institutions (DI) Payments Study An Electronic Payments (EP) Study A Check Sample (CS) Study • The study methodologies from the 2001 and 2004 studies were repeated in order to ensure comparability with those studies. Décima Conferencia Internacional de Sistemas de Pagos

Number of Noncash Retail Payments 3.9% 4.6% 2000 2003 2006 2000 - 2003 2003 - 2006 Checks (paid) 41.9 37.3 30.6 Total (billions) 72.5 81.4 93. 3 • -3.8% • -6.4% Debit card 8.3 15.6 25.3 • 23.5% • 17.5% Signature 5.3 10.3 16.0 • 24.9% • 15.8% PIN 3.0 5.3 9.4 • 21.0% • 20.6% Credit card 15.6 19.0 21.7 • 6.7% • 4.6% ACH 6.2 8.8 14.6 • 12.1% • 18.6% EBT 0.5 0.8 1.1 • 15.4% • 10.0% Current Situation of the Retail Payment System in the USA • CAGR Décima Conferencia Internacional de Sistemas de Pagos

Distribution of Noncash Retail Payments 2003 Number 2006 Number • Debit card • Debit card • Checks (paid) • Debit card • 19% • 19% • Checks (paid) • Checks (paid) • 27% • 33% • 46% • 46% • 23% • 23% • Credit card • Credit card • 1% • EBT • 1% • 1% • 23% • 16% • 11% • 11% • Credit card • ACH • EBT • EBT • ACH • ACH 2003 Value 2006 Value • Checks (paid) • Debit card • 1% • 55% • Checks (paid) • Checks (paid) • 61% • Credit card • 3% • Debit card • 1% • 3% • Credit card • 36% • 0% • ACH • EBT • 1% • 0% • 41% • EBT • EBT • ACH Current Situation of the Retail Payment System in the USA Décima Conferencia Internacional de Sistemas de Pagos

A Closer Look at Check Payments 3.9% 4.6% 2000 2003 2006 2000 - 2003 2003 - 2006 Checks (paid) 41.9 37.3 30.6 Total (billions) 72.5 81.4 93.3 • -3.8% • -6.4% 8.3 15.6 25.3 Debit card • 23.5% • 17.5% 5.3 10.3 16.0 Signature • 24.9% • 15.8% 3.0 5.3 9.4 PIN • 21.0% • 20.6% 15.6 19.0 21.7 Credit card • 6.7% • 4.6% 6.2 8.8 14.6 • 12.1% • 18.6% ACH 0.5 0.8 1.1 • 15.4% • 10.0% EBT Current Situation of the Retail Payment System in the USA • CAGR Décima Conferencia Internacional de Sistemas de Pagos

Check Usage Current Situation of the Retail Payment System in the USA • Survey results are based on the checks paid by the customer’s bank (paying bank) • Estimates are based on a two month sample of over 1400 financial institutions • The number of checks paid is different than the number of checks written because of the possibility that some checks can be converted to ACH debits for the purpose of collection • The Check Truncation Act (Check 21) was adopted in 2004 and allows collecting banks to truncate their checks and exchange check images for collection • Most banks offer both Check 21 and ACH conversion services Décima Conferencia Internacional de Sistemas de Pagos

Number of checks written, paid, and converted to ACH (billions) A Closer Look at Checks Written Current Situation of the Retail Payment System in the USA CAGR (2003-06) Total change (billions) • 37.6 -4.1% -4.5 Checks written • 33.1 Converted to ACH* 98.7% 2.2 • 37.3 -6.4% -6.7 • 30.6 • Checks paid • 2003 • 2006 Figures may not add due to rounding. * Other forms of check conversion exist, but their volumes are insignificant. Décima Conferencia Internacional de Sistemas de Pagos

2006 distribution of checks by counterparty and purpose Percent of sampled population of checks* Composition of the Check Market Current Situation of the Retail Payment System in the USA • 51% • Representative random sample of over 32,000 checks. • Sample population is about 40% of “prime pass” checks. • Consumers write 58% of checks paid. • Businesses/government receive 76% of checks paid. • Remittance • Remit/POS • POS • 32% • Income • 25% • Casual • 17% • 16% • 6% • 7% • 13% • 5% • 3% • C2B • B2B • B2C • C2C “B” refers to business or government. Figures may not add due to rounding. * Population is “prime pass” checks processed by nine large commercial banks. Estimates exclude 0.2% of checks that could not be classified. Décima Conferencia Internacional de Sistemas de Pagos

A Closer Look at Card Payments 3.9% 4.6% 2000 2003 2006 2000 - 2003 2003 - 2006 Checks (paid) 41.9 37.3 30.6 Total(billions) 72.5 81.4 93.3 • -3.8% • -6.4% Debit card 8.3 15.6 25.3 • 23.5% • 17.5% Signature 5.3 10.3 16.0 • 24.9% • 15.8% PIN 3.0 5.3 9.4 • 21.0% • 20.6% Credit card 15.6 19.0 21.7 • 6.7% • 4.6% ACH 6.2 8.8 14.6 • 12.1% • 18.6% EBT 0.5 0.8 1.1 • 15.4% • 10.0% Current Situation of the Retail Payment System in the USA • CAGR Décima Conferencia Internacional de Sistemas de Pagos

Debit Card Payments by Type Current Situation of the Retail Payment System in the USA CAGR (2003-06) Total change (billions) • Number of debit card payments • (billions) Debit card 17.5% 9.7 • 25.3 20.6% 4.0 • 9.4 • PIN • 15.6 • 5.3 15.8% 5.7 • 16.0 • Signature • 10.3 • 2003 • 2006 Figures may not add due to rounding. Décima Conferencia Internacional de Sistemas de Pagos

Prepaid Cards Current Situation of the Retail Payment System in the USA Décima Conferencia Internacional de Sistemas de Pagos

A Closer Look at ACH Payments 3.9% 4.6% 2000 2003 2006 2000 - 2003 2003 - 2006 Checks (paid) 41.9 37.3 30.6 Total(billions) 72.5 81.4 93.3 • -3.8% • -6.4% Debit card 8.3 15.6 25.3 • 23.5% • 17.5% Signature 5.3 10.3 16.0 • 24.9% • 15.8% PIN 3.0 5.3 9.4 • 21.0% • 20.6% Credit card 15.6 19.0 21.7 • 6.7% • 4.6% ACH 6.2 8.8 14.6 • 12.1% • 18.6% EBT 0.5 0.8 1.1 • 15.4% • 10.0% Current Situation of the Retail Payment System in the USA • CAGR Décima Conferencia Internacional de Sistemas de Pagos

A Closer Look at ACH Payments Current Situation of the Retail Payment System in the USA • Number of ACH payments • (billions) CAGR (2003-06) Total change (billions) ACH payments 18.6% 5.8 • 14.6 98.7% 2.2 • 2.6 • Converted checks • 8.8 12.6% 3.6 • 12.0 • Other ACH • 8.4 • 2003 • 2006 Figures may not add due to rounding. Décima Conferencia Internacional de Sistemas de Pagos

2007 View Current Situation of the Retail Payment System in the USA • Electronic payments today comprise over two-thirds of all noncash retail payments • Card payments are now over half of all noncash retail payments • Debit cards are now used more frequently than credit cards • The number of checks continues to decline, and at a more rapid rate • Check clearing is increasingly electronic • Biggest share of checks remaining are consumer to business Décima Conferencia Internacional de Sistemas de Pagos

Conclusions Current Situation of the Retail Payment System in the USA • Payments are being made electronically and more paper payments are being processed electronically • Results underscore the importance of check electronification and other innovations that improve payments system efficiency • Payment instruments and the preferences of consumers and businesses will continue to evolve • Market intelligence is increasingly important and payments system participants must carefully manage assets and resources Décima Conferencia Internacional de Sistemas de Pagos

Current Situation of the Retail Payment System in the USA • Detailed reports on the three studies are available at www.frbservices.org • ¿Preguntas? Gracias por su interés Décima Conferencia Internacional de Sistemas de Pagos