Download

1 / 63

750 likes | 1.01k Views

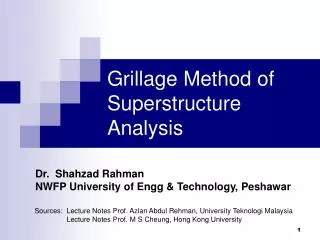

Lecture Notes ECON 437/837: ECONOMIC COST-BENEFIT ANALYSIS Lecture Three. INVESTMENT CRITERIA, TIMING, AND SCALE. (+). 0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15. Benefits Less Costs. Year of Project Life. (-). Initial Investment Period. Operating Stage. Liquidation.

E N D

Lecture Notes ECON 437/837: ECONOMIC COST-BENEFIT ANALYSIS Lecture Three

(+) 0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 Benefits Less Costs Year of Project Life (-) Initial Investment Period Operating Stage Liquidation Project Life Project Cash Flow Profile

Discounting Basic Concepts: • Discounting • Recognizes time value of money a) Funds when invested yield a return b) Future consumption worth less than present consumption o o PVB = B /(1+r) + B /(1+r) 1 +.…….+ B /(1+r) n r o 1 n o o n PVC = C /(1+r) + C /(1+r) 1 +.…….+ C /(1+r) o r 1 n o NPV = (B - C )/(1+r) +(B - C )/(1+r) +.…….+(B - C )/(1+r) n o 1 r o o 1 1 n n

Discounting (Cont’d) B. Cumulative Values • The calendar year to which all projects are discounted to is important. • All mutually exclusive projects need to be compared as of same calendar year. 1 - C )(1+r) +(B - C ) +..+..+(B - C )/(1+r) and 1 n - 1 If NPV = (B r o o 1 1 n n 3 NPV = (B - C )(1+r) +(B - C )(1+r) +(B - C )(1+r)+(B - C )+...(B - C )/(1+r) 3 2 n - 3 o o 1 1 2 2 3 3 n n r 3 1 Then NPV = (1+r) 2 NPV r r

Example of Discounting Year 0 1 2 3 4 Net Cash Flow -1000 200 300 350 1440

r0 r1 If funds currently are abnormally scarce r2 r3 r4 r5 Normal or historical average cost of funds r *4 r *3 If funds currently are abnormally abundant r *2 r *1 r *0 Years from present period 0 1 2 3 4 5 C. Variable Discount Rates • Adjustment of Cost of Funds Through Time • For variable discount rates r1, r2, & r3 in years 1, 2, and 3, the discount factors are, respectively, as follows: 1/(1+r1), 1/[(1+r1)(1+r2)] & 1/[(1+r1)(1+r2)(1+r3)]

Example of Discounting (multiple rates) Year 0 1 2 3 4 Net Cash Flow -1000 200 300 350 1440 r 18% 16% 14% 12% 10%

Alternative Investment Criteria • Net Present Value (NPV) • Benefit-Cost Ratio (BCR) • Pay-out or Pay-back Period • Internal Rate of Return (IRR) • Debt Service Capacity Ratio • Cost Effectiveness Analysis

Criterion: Net Present Value (NPV) • The NPV is the algebraic sum of the discounted values of the incremental expected positive and negative net cash flows over a project’s anticipated lifetime. • What does net present value mean? • Measures the change in wealth created by the project. • If this sum is equal to zero, then investors can expect to recover their incremental investment and to earn a rate of return on their capital equal to the private cost of funds used to compute the present values. • Investors would be no further ahead with a zero-NPV project than they would have been if they had left the funds in the capital market. • In this case there is no change in wealth.

NPV Criterion (Cont’d) • Use as a decision criterion to answer following: a. When to reject projects? b. Select projects under a budget constraint? c. Compare mutually exclusive projects? d. How to choose between highly profitable mutually exclusive projects with different lengths of life?

NPV Criterion (Cont’d) a. When to Reject Projects? Rule:“Do not accept any project unless it generates a positive net present value when discounted by the opportunity cost of funds” Examples: Project A: Present Value Costs $1 million, NPV = + $70,000 Project B: Present Value Costs $5 million, NPV = - $50,000 Project C: Present Value Costs $2 million, NPV = + $100,000 Project D: Present Value Costs $3 million, NPV = - $25,000 Result: Only projects A and C are acceptable. The country is made worse off if projects B and D are undertaken.

NPV Criterion (Cont’d) b. When You Have a Budget Constraint? Rule: “Within the limit of a fixed budget, choose that subset of the available projects which maximizes the net present value” Example: If budget constraint is $4 million and 4 projects with positive NPV: Project E: Costs $1 million, NPV = + $60,000 Project F: Costs $3 million, NPV = + $400,000 Project G: Costs $2 million, NPV = + $150,000 Project H: Costs $2 million, NPV = + $225,000 Result: Combinations FG and FH are impossible, as they cost too much. EG and EH are within the budget, but are dominated by the combination EF, which has a total NPV of $460,000. GH is also possible, but its NPV of $375,000 is not as high as EF.

NPV Criterion (Cont’d) c. When You Need to Compare Mutually Exclusive Projects? Rule:“In a situation where there is no budget constraint but a project must be chosen from mutually exclusive alternatives, we should always choose the alternative that generates the largest net present value” Example: Assume that we must make a choice between the following three mutually exclusive projects: Project I: PV costs $1.0 million, NPV = $300,000 Project J: PV costs $4.0 million, NPV = $700,000 Project K: PV costs $1.5 million, NPV = $600,000 Result: Projects J should be chosen because it has the largest NPV.

Criterion: Benefit-Cost Ratio (R) • As its name indicates, the benefit-cost ratio (R), or what is sometimes referred to as the profitability index, is the ratio of the PV of the net cash inflows (or economic benefits) to the PV of the net cash outflows (or economic costs):

Benefit-Cost Ratio (Cont’d) Basic rule: If benefit-cost ratio (R) >1, then the project should be undertaken. Problems? Sometimes it is not possible to rank projects with the Benefit-Cost Ratio: • Mutually exclusive projects of different sizes • Mutually exclusive projects and recurrent costs subtracted out of benefits or benefits reported gross of operating costs • Not necessarily true that project “A” is better if RA>RB.

Benefit-Cost Ratio (Cont’d) First Problem: The Benefit-Cost Ratio does not adjust for mutually exclusive projects of different sizes.For example: Project A: PV0 of Costs = $5.0 M, PV0 of Benefits = $7.0 M NPV0A = $2.0 M RA = 7/5 = 1.4 Project B: PV0 of Costs = $20.0 M, PV0 of Benefits = $24.0 M NPV0B = $4.0 M RB = 24/20 = 1.2 According to the Benefit-Cost Ratio criterion, project A should be chosen over project B because RA>RB, but the NPV of project B is greater than the NPV of project A. So, project B should be chosen.

Benefit-Cost Ratio (Cont’d) Second Problem: The Benefit-Cost Ratio does not adjust for mutually exclusive projects recurrent costs subtracted out of benefits and costs.For example: Project A: PV0 Total Costs = $5.0 M PV0 Recurrent Costs = $1.0 M (i.e. Fixed Costs = $4.0 M) PV0 of Gross Benefits= $10.0 M RA = (10-1)/(5-1) = 2.25 When not subtracting the recurrent cost: RA = 10/5 = 2 Project B: Total Costs = $20.0 M PV0 Recurrent Costs = $18.0 M (i.e. Fixed Costs = $2.0 M) PV0 of Gross Benefits= $24.0 M RB = (24-18)/(20-18) = 3 When not subtracting the recurrent cost: RB = 24/20 = 1.2 Hence, project B should be chosen over project A under Benefit-Cost Criterion. Conclusion:The Benefit-Cost Ratio should not be used to rank projects.

Criterion: Pay-out or Pay-back Period • The pay-out period measures the number of years it will take for the undiscounted net benefits (positive net cash flows) to repay the investment. • A more sophisticated version of this rule compares the discounted benefits over a given number of years from the beginning of the project with the discounted investment costs. • An arbitrary limit is set on the maximum number of years allowed and only those investments having enough benefits to offset all investment costs within this period will be acceptable.

Bt - Ct Ba Bb ta 0 tb Time Ca = Cb Payout period for project a Payout period for project b • Project with shortest payback period is preferred by this criteria. Comparison of Two Projects With Differing Lives Using Pay-Out Period

Pay-Out or Pay-Back Period (Cont’d) • Assumes all benefits that are produced by a longer life project have an expected value of zero after the pay-out period. • The criterion may be useful when the project is subject to high level of political risk.

t i=0 Criterion: Internal Rate of Return (IRR) • IRR is the discount rate (K) at which the present value of benefits are just equal to the present value of costs for the particular project: Bt - Ct (1 + K)t Note: the IRR is a mathematical concept, not an economic or financial criterion. = 0

Common uses of IRR: (a) If the IRR is larger than the cost of funds, then the project should be undertaken. (b) Often the IRR is used to rank mutually exclusive projects. The highest IRR project should be chosen. Note: An advantage of the IRR is that it only uses information from the project.

Bt - Ct +300 Time -100 -200 IRR Criterion (Cont’d) First Difficulty: Multiple rates of return for project Solution 1: K = 100%; NPV= -100 + 300/(1+1) + -200/(1+1)2 = 0 Solution 2: K = 0%; NPV= -100+300/(1+0)+-200/(1+0)2 = 0

IRR Criterion (Cont’d) Second difficulty: Projects of different sizes and also mutually exclusive Year 0 1 2 3 ... ... Project A - 2,000 +600 +600 +600 +600 +600 +600 Project B - 20,000 +4,000 +4,000 +4,000 +4,000 +4,000 +4,000 NPV and IRR provide different conclusions: Opportunity cost of funds = 10% 0 NPV : 600/0.10 - 2,000 = 6,000 - 2,000 = 4,000 A NPV : 4,000/0.10 - 20,000 = 40,000 - 20,000 = 20,000 0 B Hence, NPV > NPV 0 0 B A IRR : 600/K - 2,000 = 0 or K = 0.30 A A A IRR : 4,000/K - 20,000 = 0 or K = 0.20 B B B Hence, K >K A B

Third difficulty: Projects of different lengths of life and mutually exclusive Opportunity cost of funds = 8% Project A: Investment costs = 1,000 in year 0 Benefits = 3,200 in year 5 Project B: Investment costs = 1,000 in year 0 Benefits = 5,200 in year 10 0 5 NPV : - 1,000 + 3,200/(1.08) = 1,177.86 A 10 0 NPV : - 1,000 + 5,200/(1.08) = 1,408.60 B 0 0 Hence, NPV > NPV B A IRR : - 1,000 + 3,200/(1+K ) = 0 which implies that K = 0.262 5 A A A IRR : - 1,000 + 5,200/(1+K ) = 0 which implies that K = 0.179 10 B B B Hence, K >K A B IRR Criterion (Cont’d)

IRR Criterion (Cont’d) Fourth difficulty: Same project but started at different times Project A: Investment costs = 1,000 in year 0 Benefits = 1,500 in year 1 Project B: Investment costs = 1,000 in year 5 Benefits = 1,600 in year 6 0 NPV : - 1,000 + 1,500/(1.08) = 388.88 A 0 6 5 NPV : - 1,000/(1.08) + 1,600/(1.08) = 327.68 B 0 0 Hence, NPV > NPV A B 1,000 + 1,500/(1 + K IRR : - ) = 0 which implies that K = 0.5 A A A 6 IRR : - 1,000/(1 + K ) = 0 which implies that K = 0.6 ) + 1,600/(1 + K 5 B B B B Hence, K >K B A

IRR for Irregular Cashflows -- Numerical Examples for Various Projects --

Debt Service Capacity Ratio • The debt service capacity ratio is a key factor in determining the ability of a project to pay its operating expenses and to meet its debt servicing obligations. • Annual debt service coverage ratio (ADSCR) is the ratio of annual net cash flow of the project before financing to annual debt payments of interest and principal. • Loan life cover ratio (LLCR) is the ratio of the present value of annual net cash flows over the present value of annual interest and loan repayments from the current period to the end of loan repayment.

Annual Net Cash Flow t Annual Debt Repayment t PV (NCFt : NCFn) PV (Debt Repaymentt: Debt Repaymentn) Calculation of ADSCR: ADSCRt = Calculation of LLCR: LLCRt = Where: The Annual Net Cash Flow of the project is calculated before financing. The Annual Debt Repayment includes the interest expenses and principal repayment due in the specific year t of the loan repayment period. The last year of debt repayment is denoted as n. The discount rate used is the borrowing rate.

Debt Service Capacity Crterion • Debt Service Capacity Ratio is another criterion for evaluating the financial viability of a project. • A viable project must repay the principal and interest on the loan, as well as to bring a positive return on equity to the owners. • It is used by bankers who want to know: • The ADSCR of a project • A summary ratio LLCR • LLCR tells the banker if there is enough cash from the project to make bridge-financing even when some years have inadequate cash flows to serve the debt.

Examples of Debt Cover Ratios • The minimum ADSCR requirement varies between projects. • Approximate levels for standard projects could be: - 1.3 for a power or process plant project with an Offtake Contract - 1.4 for an infrastructure project with a toll road or mass transit project - 1.5 for a natural resources project - 2.0 for a merchant power plant project with no Offtake or price hedging • Higher cover levels would be required for a project with nonstandard risks or located in a country with a poor credit risk.

Year 0 Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year 10 Net Cash Flow -2,000,000 320,000 320,000 360,000 440,000 380,000 100,000 200,000 480,000 540,000 640,000 Debt Repayment 298,316 298,316 298,316 298,316 298,316 ADSCR 1.07 1.07 1.21 1.47 1.27 Use of ADSCR • A project is considered for implementation: Total Investment Costs: 2,000,000 Equity Funds: 1,000,000 Proposed Loan: 1,000,000 Start of Loan Repayment Year 1 (equal repayments) Required Rate of Return on Equity: 20% • Loan of 1,000,000 is given to project for 5 years at 15%: • Result: this project is not attractive to the banker since the ADSCR are low, meaning that the net cash flow may not be enough to meet the debt service obligations and to obtain the required rate of return on equity.

How to improve the ADSCRs? • Decrease the interest rate on the loan • Decrease the amount of borrowing • Increase the duration of loan repayment • Restructuring of the terms of the loan will make the ratios look better, and the project will become attractive to the Banker.

Year 0 Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year 10 Net Cash Flow -2,000,000 320,000 320,000 360,000 440,000 380,000 100,000 200,000 480,000 540,000 640,000 206,040 206,040 206,040 206,040 206,040 Debt Repayment ADSCR 1.55 1.55 1.75 2.14 1.84 • Decrease the Interest Rate on the loan Loan of 1,000,000 is given to project for 5 years at 1%: • Result: the ratios look better now, but it will normally require government guarantees or subsidies to reduce interest rates – not easy to obtain.

Year 0 Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year 10 Net Cash Flow -2,000,000 320,000 320,000 360,000 440,000 380,000 100,000 200,000 480,000 540,000 640,000 Debt Repayment 178,989 178,989 178,989 178,989 178,989 ADSCR 1.79 1.79 2.01 2.46 2.12 2. Decrease the amount of borrowing by increasing equity to 1.4 million Loan of 600,000 is borrowed for 5 years at 15%: • Result: since the proportion of borrowing in the total investment decreases, the amount of annual repayment of the loan also becomes smaller, hence the ability to service the debt becomes more certain.

Year 0 Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year 10 Net Cash Flow -2,000,000 320,000 320,000 360,000 440,000 380,000 100,000 200,000 480,000 540,000 640,000 Debt Repayment 199,252 199,252 199,252 199,252 199,252 199,252 199,252 199,252 199,252 199,252 ADSCR 1.61 1.61 1.81 2.21 1.91 0.50 1.00 2.41 2.71 3.21 3. Increase the duration of loan repayment Loan of 1,000,000 is given to project for 10 years at 15%: • Result: Increasing the duration of debt repayment improves the ratios. The same amount of loan is repaid over more years. • However, in Year 6 and Year 7 the Net Cash Flows are inadequate to meet the debt repayment obligations.

What is the solution to improve cash flows at the bad year? • If project expects difficulties in a particular future year as the net cash flows are not enough to service the debt in that period(s). • Questions: • Should project maintain Debt Service Reserve Account (e.g., an Escrow Fund)? • Is bridge financing a viable option?

Should project maintain a Debt Service Reserve Account? • Definitions: • A fund established upon the requirement of the lenders to hold cash that can be used towards debt servicing. • This fund restricts the payment of dividends. • Typically contains between 6 and 12 months of debt service. • Cash can be withdrawn from the Debt Service Reserve Account if the project’s cash flow from operations does not cover the project’s debt service requirements.

Is bridge financing a viable option? • To find out if the bridge-financing is worth undertaking, we need to look at the cash flows and debt repayments over the remaining period of debt service. • LLCR is the appropriate criteria to use to determine if project finances for bridge-financing. • The present values of net cash flows remaining till the end of debt repayment period, discounted at the loan interest rate, is divided by the present values of debt repayments remaining till the end of debt repayment period, also discounted at the loan interest rate. It needs to be substantially bigger than one.

Year 0 Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year 10 Net Cash Flow -2,000,000 320,000 320,000 360,000 440,000 380,000 100,000 200,000 480,000 540,000 640,000 Debt Repayments 199,252 199,252 199,252 199,252 199,252 199,252 199,252 199,252 199,252 199,252 2,052,134 1,991,954 1,922,747 1,797,159 1,560,733 1,357,843 1,446,519 1,433,497 1,096,522 640,000 NPV of NCF NPV of Debt Repayments 1,150,000 1,093,360 1,028,224 953,318 867,176 768,112 654,189 523,178 372,515 199,252 ADSCR 1.61 1.61 1.81 2.21 1.91 0.50 1.00 2.41 2.71 3.21 LLCR 1.78 1.82 1.87 1.89 1.80 1.77 2.21 2.74 2.94 3.21 Is Bridge Financing an option ? Results: Although the ADSCRs in Year 6 and Year 7 are very low, the ability of the project to generate cash in consequent years should be enough to obtain bridge-financing for these two critical years.

Cost Effectiveness Analysis • The cost effectiveness analysis is primarily used in social projects where it is difficult to quantify benefits in monetary terms. • Examples include health and educational projects. In such projects, the selection criterion could be to select the alternative which has the least cost.

SCALE, TIMING AND ADJUSTMENT FOR LENGTH OF LIFE IN PROJECT APPRAISAL

The Importance of Scale and Timing in Project Appraisal • Why is scale important? • Too large or too small can destroy a good project

Bt - Ct B3 B2 B1 0 Time C1 C2 C3 Choice of Scale • Rule: Optimal scale is when NPV = 0 for the last addition to scale and NPV > 0 for the whole project. • Net benefit profiles for alternative scales of a facility < NPV (B1 – C1) 0 ? < NPV (B2 – C2) 0 ? < NPV (B3 – C3) 0 ?

NPV (+) NPV of Project 0 Scale of Project A B C D E F G H I J K L M N (-) Determination of Scale of Project • Relationship between net present value and scale

Determination of Scale of Project for Improvement Projects that generate Benefits forever Year Scale $000s 0 1 2 3 4 5 to MC MB $000s MNPV 10% MIRR S0 S1 - S0 S2 - S1 S3 - S2 S4 - S3 S5 - S4 S6 - S5 -3000 -1000 -1000 -1000 -1000 -1000 -1000 50 75 275 400 200 101 49 50 75 275 400 200 101 49 50 75 275 400 200 101 49 50 75 275 400 200 101 49 50 75 275 400 200 101 49 -2500 -250 1750 3000 1000 10 -510 0.017 0.075 0.275 0.400 0.200 0.101 0.049 Year Scale 0 1 2 3 4 5 to Costs Benefits NPV 10% IRR S0 S1 S2 S3 S4 S5 S6 -3000 -4000 -5000 -6000 -7000 -8000 -9000 50 125 400 800 1000 1101 1150 50 125 400 800 1000 1101 1150 50 125 400 800 1000 1101 1150 50 125 400 800 1000 1101 1150 50 125 400 800 1000 1101 1150 -2500 -2750 -1000 2000 3000 3010 2500 0.017 0.031 0.080 0.133 0.143 0.138 0.128

Note: • NPV of last increment to scale at scale S5, i.e., ΔNPV of scale 5 = 10. • NPV of project is maximized at scale of 5, i.e. NPV1-5 = 3010. • IRR is maximized at scale 4. • When the IRR on the last increment to scale (MIRR) is equal to discount rate, the NPV of project is maximized.

Timing of Investments Key Questions: 1. What is right time to start a project? 2. What is right time to end a project? Four Illustrative Cases of Project Timing: Case 1. Benefits (net of operating costs) increasing continuously with calendar time. Investments costs are independent of calendar time. Case 2. Benefits (net of operating costs) increasing with calendar time. Investment costs are function of calendar time. Case 3. Benefits (net of operating costs) rise and fall with calendar time. Investment costs are independent of calendar time. Case 4. Costs and benefits do not change systematically with calendar time.

Benefits and Costs B (t) I D E rK A C B1 Time t0 t1 t2 rKt Bt+1 <> K rKt > Bt+1 Postpone rKt < Bt+1 Start K Case 1: Timing of Projects: Potential Benefits are Rising but Investment Costs are Independent of Calendar Time