Download

1 / 35

350 likes | 520 Views

Financial Management Fin 620. Dr. Lawrence P. Shao Marshall University Summer 2003. CHAPTER 23 Short-Term Financing. Working capital financing policies Accounts payable (trade credit) Commercial paper Short-term bank loans Secured short-term credit. Working Capital Financing Policies.

E N D

Financial ManagementFin 620 Dr. Lawrence P. Shao Marshall University Summer 2003

CHAPTER 23Short-Term Financing • Working capital financing policies • Accounts payable (trade credit) • Commercial paper • Short-term bank loans • Secured short-term credit

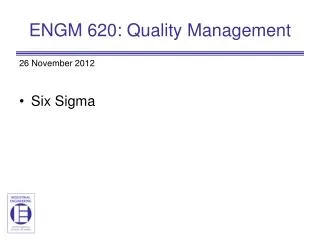

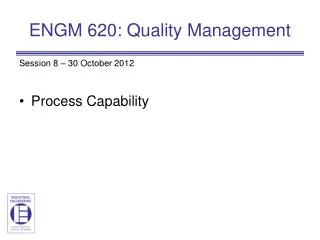

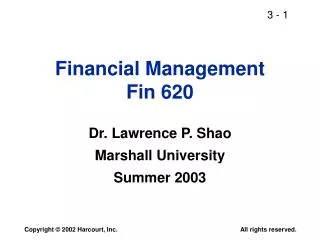

Working Capital Financing Policies • Maturity Matching: Matches the maturity of the assets with the maturity of the financing. • Aggressive: Uses short-term (temporary) capital to finance some permanent assets. • Conservative: Uses long-term (permanent) capital to finance some temporary assets.

Maturity Matching Financing Policy $ Temp. C.A. S-T Loans L-T Fin: Stock, Bonds, Spon. C.L. Perm C.A. Fixed Assets Years What are “permanent” assets?

Aggressive Financing Policy $ Temp. C.A. S-T Loans L-T Fin: Stock, Bonds, Spon. C.L. Perm C.A. Fixed Assets Years More aggressive the lower the dashed line.

Conservative Financing Policy $ Marketable Securities Zero S-T debt L-T Fin: Stock, Bonds, Spon. C.L. Perm C.A. Fixed Assets Years

The choice of working capital policy is a classic risk/return tradeoff. • The aggressive policy promises the highest return but carries the greatest risk. • The conservative policy has the least risk but also the lowest expected return. • The moderate (maturity matching) policy falls between the two extremes.

What is short-term credit?What are the major sources? • Short-term credit: Debt requiring repayment within one year. • Major sources: • Accruals • Accounts payable (trade credit) • Commercial paper • Bank loans

Short-term debt is riskier than long-term debt for the borrower. • Short-term rates may rise. • May have trouble rolling debt over. • Advantages of short-term debt. • Typically lower cost. • Can get funds relatively quickly with low transactions costs. • Can repay without penalty.

Is there a cost to accruals?Do firms have much control over amount of accruals? • Accruals are free in the sense that no explicit interest is charged. • However, firms have little control over accrual levels, which are influenced more by industry custom, economic factors, and tax laws than by managerial actions.

What is trade credit? • Trade credit is credit furnished by a firm’s suppliers. • Trade credit is often the largest source of short-term credit for small firms. • Trade credit is spontaneous and relatively easy to get, but the cost can be high.

B&B buys $3,030,303 gross, or $3,000,000 net, on terms of 1/10, net 30. However, the firm pays on Day 40.How much free and costly trade credit are they getting?What is the cost of the costly trade credit?

Gross/Net Breakdown • Company buys goods worth $3,000,000. That’s the cash price. • They must pay $30,303 more over the year if they forego the discount. • Think of the extra $30,303 as a financing cost similar to the interest on a loan. • Must compare that cost with the cost of alternative credit.

Net daily purchases = $3,000,000/360 = $8,333. Payables level if discount is taken: Payables = $8,333 (10) = $83,333. Payables level if don’t take discount: Payables = $8,333 (40) = $333,333. Credit Breakdown: Total trade credit = $333,333 Free trade credit = 83,333 Costly trade credit = $250,000

$30 , 303 k 0 . 1212 12 . 12%. Nom $250 , 000 Nominal Cost of Costly Trade Credit Firm loses 0.01($3,030,303) = $30,303 of discounts to obtain $250,000 in extra trade credit, so But the $30,303 in lost discounts is paid all during the year, not just at year-end, so the EAR is higher.

Nominal Cost Formula, 1/10, net 40 Discount % 1 - Discount % 360 Days taken - Discount period kNom = x = x = 0.0101 x 12 = 0.1212 = 12.12%. 1 99 360 30 Pays 1.01% 12 times per year.

Effective Annual Rate, 1/10, net 40 Periodic rate = 0.01/0.99 = 1.01%. Periods/year = 360/(40 - 10) = 12. EAR = (1 + Periodic rate)n - 1.0 = (1.0101)12 - 1.0 = 12.82%.

Commercial Paper (CP) • CP are short term notes issued by large, strong companies. B&B could not issue CP; the company is too small. • CP trades in the market at rates just above the T-bill rate. • CP is bought by banks and other companies, then held as marketable securities for liquidity purposes.

A bank is willing to lend B&B $100,000 for 1 year at an 8 percent nominal rate. What is the EAR under the following five loans? 1. Simple annual interest, 1 year. 2. Simple interest, paid monthly. 3. Discount interest. 4. Discount interest with 10 percent compensating balance. 5. Installment loan, add-on, 12 months.

Why must we use Effective Annual Rates (EARs) to evaluate the loans? • In our examples, the nominal (quoted) rate is 8% in all cases. • We want to compare loan cost rates and choose the alternative with the lowest cost. • Because the loans have different terms, we must make the comparison on the basis of EARs.

Simple Annual Interest, 1-Year Loan “Simple interest” means not discount or add-on. Interest = 0.08($100,000) = $8,000. $8 , 000 . k EAR 0 . 08 8 . 0% Nom $100 , 000 On a simple interest loan of one year, kNom = EAR.

Simple Interest, Paid Monthly Monthly interest = (0.08/12)($100,000) = $666.67. 0 1 12 ... 100,000 -666.67 -667.67 -100,000.00 12 100000 -666.67 -100000 N I/YR PV PMT FV 0.66667 (More…)

kNom = (Monthly rate)(12) = 0.66667%(12) = 8.00%. 12 0 . 08 EAR 1 1 8 . 30%. 12 or: 8 NOM%, 12 P/YR, EFF% = 8.30%. Note: If interest were paid quarterly, then: 4 0 . 08 EAR 1 1 8 . 24%. 4 Daily, EAR = 8.33%.

N I/YR PV PMT FV 8% Discount Interest, 1 Year Interest deductible = 0.08($100,000) = $8,000. Usable funds = $100,000 - $8,000 = $92,000. 0 1 i = ? 92,000 -100,000 1 92 0 -100 8.6957% = EAR

Discount Interest (Continued) Amount needed 1 - Nominal rate (decimal) Amt. borrowed = = = $108,696. $100,000 0.92

Amount needed 1 - Nominal rate - CB Face amount of loan = = = $121,951. $100,000 1 - 0.08 - 0.1 Need $100,000. Offered loan with terms of 8% discount interest, 10% compensating balance. (More...)

Interest = 0.08 ($121,951) = $9,756. $9 , 756 EAR 9 . 756%. $100 , 000 EAR correct only if amount is borrowed for 1 year. (More...)

8% Discount Interest with 10% Compensating Balance (Continued) 0 1 i = ? 121,951 Loan -121,951 + 12,195 -109,756 -9,756 Prepaid interest -12,195 CB 100,000 Usable funds 1 100000 0 -109756 N I/YR PV PMT FV 9.756% = EAR This procedure can handle variations.

1-Year Installment Loan, 8% “Add-On” Interest = 0.08($100,000) = $8,000. Face amount = $100,000 + $8,000 = $108,000. Monthly payment = $108,000/12 = $9,000. = $100,000/2 = $50,000. Approximate cost = $8,000/$50,000 = 16.0%. Average loan outstanding (More...)

Installment Loan To find the EAR, recognize that the firm has received $100,000 and must make monthly payments of $9,000. This constitutes an ordinary annuity as shown below: Months 0 1 2 12 ... i=? 100,000 -9,000 -9,000 -9,000

N I/YR PV PMT FV 12 100000 -9000 0 1.2043% = rate per month kNom = APR = (1.2043%)(12) = 14.45%. EAR = (1.012043)12 - 1 = 15.45%. 14.45 NOM enters nominal rate 12 P/YR enters 12 pmts/yr EFF% = 15.4489 = 15.45%. 1 P/YR to reset calculator.

What is a secured loan? • In a secured loan, the borrower pledges assets as collateral for the loan. • For short-term loans, the most commonly pledged assets are receivables and inventories. • Securities are great collateral, but generally firms needing short-term loans generally do not have securities.

What are the differences betweenpledgingandfactoringreceivables? • If receivables are pledged, the lender has recourse against both the original buyer of the goods and the borrower. • When receivables are factored, they are generally sold, and the buyer (lender) has no recourse to the borrower.

What are three forms of inventory financing? • Blanket lien. • Trust receipt. • Warehouse receipt. • The form used depends on the type of inventory and situation at hand.

Legal stuff is vital. • Security agreement: Standard form under Uniform Commercial Code. Describes when lender can claim collateral. • UCC Form-1: Filed with Secretary of State to establish claim. Future lenders do search, won’t lend if prior UCC-1 is on file.