Download

1 / 6

60 likes | 444 Views

Expected (Ex Ante) Return, Variance, and Covariance. Expected Return: E(R) = S (ps x Rs)Variance: s2 = S {ps x [Rs - E(R)]2}Standard Deviation = sCovariance: sAB = S {ps x [Rs,A - E(RA)] x [Rs,B - E(RB)]}Correlation Coefficient: rAB = sAB / (sA sB). Return and Risk for Portfolios (2 Ass

E N D

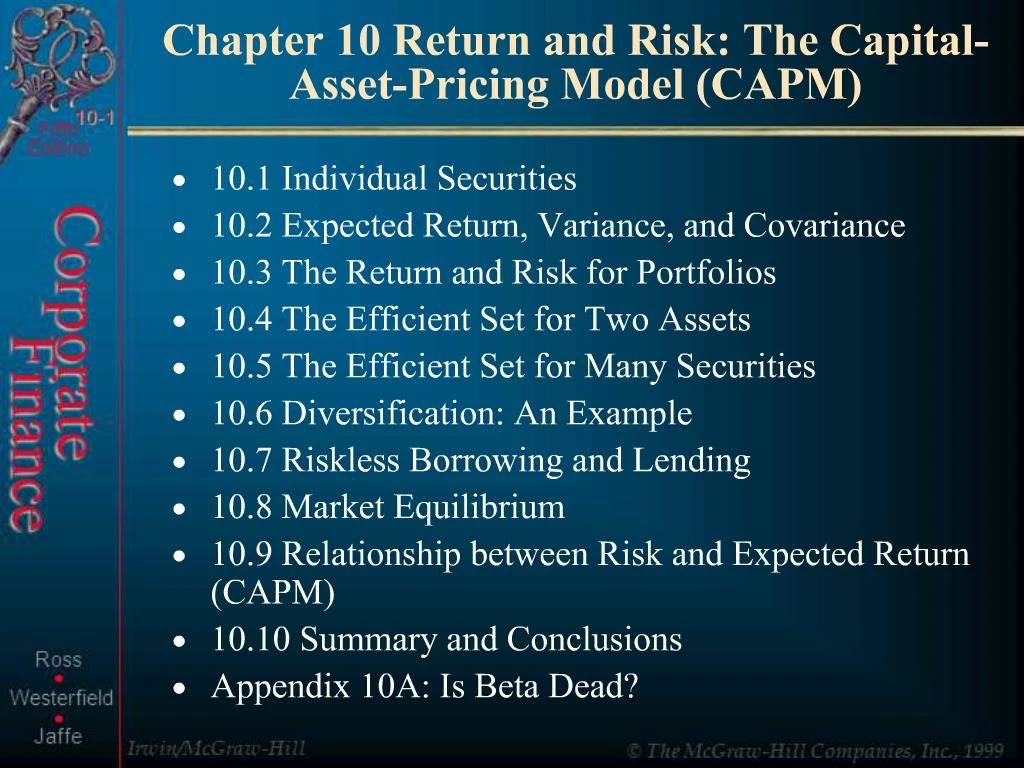

1. Chapter 10 Return and Risk: The Capital-Asset-Pricing Model (CAPM) 10.1 Individual Securities

10.2 Expected Return, Variance, and Covariance

10.3 The Return and Risk for Portfolios

10.4 The Efficient Set for Two Assets

10.5 The Efficient Set for Many Securities

10.6 Diversification: An Example

10.7 Riskless Borrowing and Lending

10.8 Market Equilibrium

10.9 Relationship between Risk and Expected Return (CAPM)

10.10 Summary and Conclusions

Appendix 10A: Is Beta Dead?

2. Expected (Ex Ante) Return, Variance, and Covariance Expected Return: E(R) = S (ps x Rs)

Variance: s2 = S {ps x [Rs - E(R)]2}

Standard Deviation = s

Covariance: sAB = S {ps x [Rs,A - E(RA)] x [Rs,B - E(RB)]}

Correlation Coefficient: rAB = sAB / (sA sB)

3. Return and Risk for Portfolios (2 Assets) Expected Return of a Portfolio:

E(Rp) = XAE(R)A + XB E(R)B

Variance of a Portfolio:

sp2 = XA2sA2 + XB2sB2 + 2 XA XB sAB

4. An Example of Portfolio Return and Risk Stock Investment Xi E.(Ri) si2

IBM $5000 50% 0.09 0.01

HM $5000 50% 0.13 0.04

Total $10000 100%

sIBM,HM = 0

E[Rp] = (0.5)(0.09) + (0.5)(0.13) = 11%

sp2 =(.5)2(.01) + (.5)2(.04) + 2(.5)(.5)(0) = 0.0125

sp = (0.0125)(1/2) = 0.1118

5. Efficient Sets and Diversification

6. Capital Market Line

7. Security Market Line