Download

1 / 34

350 likes | 649 Views

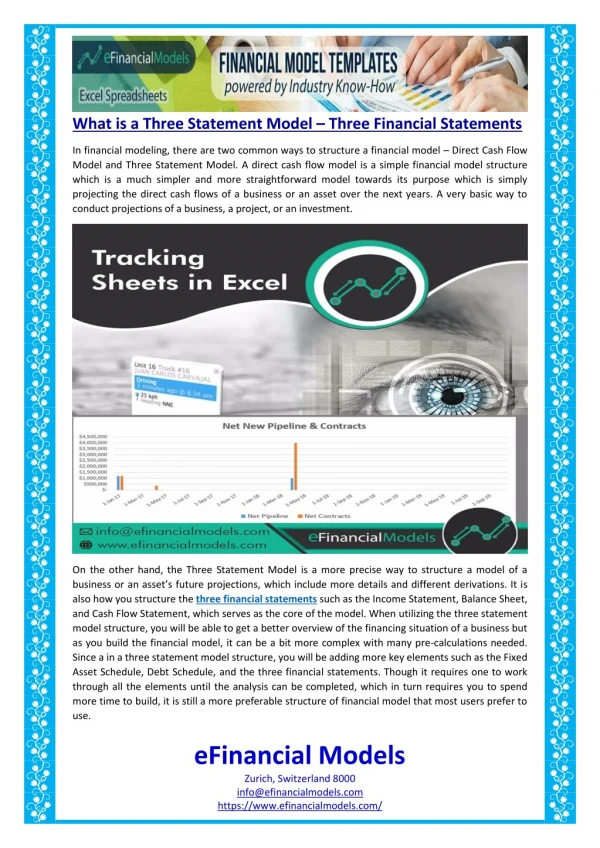

Summary of the Three Financial Statements. Income Statement. Cash Flow Statement. Balance Sheet. Snapshot at balance sheet date. History of revenue less expenses over a year. History of cash in less cash out over a year. Formula L + E = A or E = A - L where:

E N D

Summary of the Three Financial Statements Income Statement Cash Flow Statement Balance Sheet Snapshot at balance sheet date History of revenue less expenses over a year History of cash in less cash out over a year Formula L + E = A or E = A - L where: A is assets L is liabilities E is equity Formula P = R - E where: R is revenue E is expenses Formula Cash: In (Out) p 24

The Accounting Information Flow Source documents Journals General ledger Trial balance Y/e adjustments Reports Subsidiaryledgers

Reporting Principles Top downLess is more Eg – A4 overview, summary level financial statements Exception reporting,eg – current ratio reported when under 1.2(have to trust system)

Reporting Principles Top down A4 overview includes:info from 3 financial statementscrucial KPIs

Reporting Principles Top down Performance dashboard is an automated version Limit info to key performance elements updated daily Automate – link to robust, reliable, integrated systems

Reporting Principles Future and Past • Reporting enhanced when: • In context of strategy • 5 year corporate plan • Annual financial budget • Actual YTD (& month) IS – also CF forecast, BS, ratios, KPIs • 5 year review IS, CF, BS & ratios • Same format for budgets & historic reporting

Reporting Principles Future and Past Why five years: Analysts recommend 5 years, 3 minimum We think better in context Review budgets in context: Consider having 3 prior years instead of just last year’s actual Obtaining more comprehensive reporting: Add historic YTD cash flow statement reporting Add views generated through Excel spreadsheets Obtain assurance

Reporting Principles Clustering (of expenses)

Analysing Financial Statements Stages of analysis: 1 Review annual report 2 Enter numbers in spreadsheet 3 Analyse performance over time

Analyse Performance Over Time Profit performance: n Trend in sales n Nature of unusual items n Trend in profit n Segment performance n Likely future sales and profit

Analyse Performance Over Time Cash flow performance: n Strength of net operating cash flows n Evidence of self generation: op CF pays for dividends and fixed assets n Financing of expansions and acquisitions n Extent of borrowings and their repayment n Likely future operating cash inflows, self-generation, borrowings and/or cash change

Analyse Performance Over Time Balance sheet performance: n Trend in total assets - which assets cause it? n Trend in total liabilities - which liabilities cause it? n Trend in level and elements of equity

Analyse Performance Over Time Analysis of ratios - trends in: n Liquidity n Management efficiency n Financing n Profitability

Liquidity Ratio Rulesof thumb ≥1.5 current assetscurrent liabilities Current ratio= Where to find figures balance sheet; overdraft in borrowings note Purpose ability to pay debts when due p 234 & 235

Liquidity Ratios - Smith Family Years 2008 2009 2010 2011 2012 Current ratio 1.7 1.5 1.4 1.3 1.0 Ruleof thumb≥1.5

Management Efficiency Ratio Ruleof thumb 2 for retailer1 for manufacturer revenueassets Asset utilisation= Where to find figures balance sheet or notes, and income statement or notes Purpose revenue from assets p 237, 239, 241, 243

Management Efficiency - Smith Family Years 2008 2009 2010 2011 2012 Asset utilisn 1.9 2.0 1.5 1.8 1.9 Ruleof thumb2 - retailer1 - manuf.

Financing Ratios Rulesof thumb≥3 ≤1 ≤0.5 EBITinterest expense Interest cover= total liabilitiesequity Debt to equity= Interest-bearing debt to equity interest bearing debtsequity = Where to find figures balance sheet or notes, and income statement or notes Purpose profit to interest, proportions of funding p 244, 247, 248

Financing Ratios – Smith Family Years 2008 2009 2010 2011 2012 Int cover NM NM NM NM NM Debt/equity 0.5 0.6 0.6 0.8 1.3Int bear debt 0.1 0.1 0.1 0.0 0.0 Rulesof thumb≥3.0≤1.0≤0.5

Profitability Ratios EBITsales EBIT margin= x 100 EBITtotal assets ROA= x 100 Surp b unus equity ROE= x 100 Where to find figures income stmt or notes - numerator, income stmt or balance sheet - denominator Purpose surplus from revenue, assets and equity p 252, 253, 256, 258

Profitability Ratios - Smith Family Years 2008 2009 2010 2011 2012 EBIT mgn 1.1% -3.1% 1.1% -0.2% -5.7%ROA 2.1% -6.2% 1.6% -0.3% -11.0%ROE 2.4% -10.7% 1.9% -1.1% -25.0%

Size Ratios - Smith Family Years 2008 2009 2010 2011 2012 Revenue change -5.1% -13.7% 16.2% 3.2%Assets change -13.1% 18.2% -4.5% -3.2%

Summary of the Three Financial Statements Income Statement Cash Flow Statement Balance Sheet Snapshot at balance sheet date History of revenue less expenses over a year History of cash in less cash out over a year Formula L + E = A or E = A - L where: A is assets L is liabilities E is equity Formula P = R - E where: R is revenue E is expenses Formula Cash: In (Out) p 24