Download

1 / 19

190 likes | 301 Views

Sampling Frequency and Jump Detection Mike Schwert ECON201FS 4/28/08. Background and Motivation Various tests exist to identify jumps in asset price movements These tests use high frequency financial data which must be sampled at some frequency

E N D

Sampling Frequency and Jump Detection Mike Schwert ECON201FS 4/28/08

Background and Motivation • Various tests exist to identify jumps in asset price movements • These tests use high frequency financial data which must be sampled at some frequency • Market microstructure noise prevents the highest frequency data from being usable • Earlier this semester, found that it is appropriate to sample prices from approximately 5 to 15 minute frequencies, based on volatility signature plots of RV and BV • Sampling at different frequencies causes jump tests to identify different “jump days” • Compound Poisson Process behind many of these models may not be appropriate model of jumps in actual asset price processes • Jump tests used: • Barndorff-Nielsen Shephard ZQP-max and ZTP-max tests • Jiang-Oomen “Swap Variance” Difference and Logarithmic tests • Microstructure Noise Robust Jiang-Oomen Difference and Log tests • Lee-Mykland test • Ait-Sahalia Jacod test

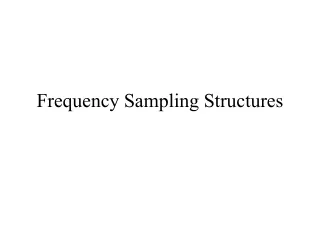

High Frequency Data • Minute-by-minute stock prices • ExxonMobil 1999-2008 (2026 days) • General Electric 1997-2007 (2670 days) • Microsoft 1997-2008 (2683 days) • AT&T 1997-2008 (2680 days) • Procter & Gamble 1997-2008 (2686 days) • Chevron 2001-2008 (1566 days) • Johnson & Johnson 1997-2008 (2685 days) • Bank of America 1997-2008 (2685 days) • Cisco Systems 1997-2008 (2683 days) • Altria Group 1997-2008 (2685 days) • Simulated data • 5-minute price data, 84 observations per day, 2500 days • Continuous process with jumps from a tempered stable distribution: α = .40, .90, 1.50, 1.90 • Many more medium sized jumps than Compound Poisson Process, which has rare large jumps and is the model assumed in most jump detection literature

Simulated Data α = 0.40 α = 0.90 α = 1.50 α = 1.90

Barndorff-Nielsen Shephard Tests • Introduced by Ole Barndorff-Nielsen and Neil Shephard in a 2006 paper • Uses the difference between realized variance, which includes jumps, and bipower variation, which is robust to jumps, to detect jumps in price processes • Realized variance: • Bipower variation: • Relative jump: • Tripower quarticity: • Quadpower quarticity: • Z statistics:

Jiang-Oomen “Swap Variance” Tests • Introduced by George Jiang and Roel Oomen in a 2005 paper • Continuous process: • Arithmetic returns: • Difference between arithmetic and geometric returns: • Normalizing coefficient: • Difference test: • Logarithmic test: • Ratio test:

Microstructure Noise Robust Jiang-Oomen Tests • Like Jiang-Oomen tests, but with microstructure noise bias correction • Microstructure noise bias: • Bias corrections: • Normalizing coefficient: • Difference test: • Logarithmic test: • Ratio test:

Lee-Mykland Test • Introduced by Suzanne Lee and Per Mykland in a 2007 paper • Allows identification of jump timing, multiple jumps in a day • Instantaneous volatility measure (K = 270): • Test statistic: • Asymptotic distribution:

Ait-Sahalia Jacod Test • Introduced in 2008 article by Yacine Ait-Sahalia and Jean Jacod • Null hypothesis: no jumps • Multipower realized variation (usually use p = 4): • Test statistic (k = 2, 3, 4): • Convergence of statistic: Jumps: • No jumps • Rejection region:

Summary of Sample Robustness • Significance levels: • Barndorff-Nielsen Shephard, Jiang-Oomen, MNR Jiang-Oomen: 0.999 • Lee-Mykland: 0.99 at each observation • Ait-Sahalia Jacod: 0.95 • Sample prices at 5, 10, 15, and 20 minute frequencies • Calculate average ratio of jump days to total days at each frequency • Calculate average percentage of common jumps between sampling frequencies for each test: • Results of jump tests appear to be highly dependent on sampling frequency • Note: these frequencies may not be entirely appropriate for some tests – more work to come • Ait-Sahalia and Jacod work with higher frequency data than we currently have • Lee and Mykland use 5 minutes as their lowest sampling frequency • Contingency tables in two pages examine results with 1, 2, 3, and 4 minute frequencies

Contingency Tables – High Frequency Ait-Sahalia Jacod MNR-JO Diff MNR-JO Log

Conclusions • Number of jump days identified is highly dependent on sampling frequency of prices • All tests except Jiang-Oomen (and MNR J-O) identify fewer jumps as frequency decreases • Barndorff-Nielsen Shephard and Jiang-Oomen tests perform very poorly in finding common jump days when sampled at different frequencies • Jiang-Oomen tests perform far better with microstructure noise corrections than without them • Lee-Mykland test appears to be fairly robust to sampling frequency • Ait-Sahalia Jacod and Microstructure Noise Robust Jiang-Oomen tests are much more sample robust with higher frequency data

Conclusions • All tests successfully identify fewer jumps as alpha increases • Tests generally seem to be more sample robust for smaller alpha, meaning they are detecting the same medium-size jumps • While Lee-Mykland detected far more jump days than the other tests with actual asset price data, it finds far fewer with the simulated data at all levels of alpha • Microstructure Noise Robust Jiang-Oomen is less consistent between samples with simulated data than with actual asset price data • All other tests are more sample robust with simulated data than with actual price data

Cross-Test Contingencies • All tests compared with the 10 stocks sampled at 5-minute frequency • 95% significance level – ratios normalized in same way as in sample robustness tables