Download

1 / 66

670 likes | 690 Views

Explore the importance of insurance in managing unforeseen risks and financial losses. Learn about types of insurance, coverage, premiums, and the insurance process.

E N D

Types of Insurance Advanced Level

Why is It important to have insurance? Emergency savings - at least six months of expenses set aside to cover costs of unexpected expenses Risk - chance of loss from an event that cannot be entirely controlled is managed by Insurance – a financial product purchased by many people facing a similar risk to protect against the risk of larger losses What are examples of unexpected events that may result in a financial loss?

Types of risk • Personal Risk-involve loss of income or life due to illness, disability, old age, or unemployment. • Property Risk-include losses to property caused by perils, such as fire or theft and hazards. • Liability risks-involve losses caused by negligence that leads to injury or property damage. • Negligence-is the failure to take ordinary or reasonable care to prevent accidents from happening.

Insurance Policy Coverage - The risks covered and amount of money paid for losses under an insurance policy Policyholder - Person who owns the insurance policy Premium - Money paid to purchase the policy Experts say that buying insurance is buying financial security. Do you think this is true? Why or why not?

An Illustration of How Insurance Works With a 1% chance that any one of them could get sick and require $10,000 in medical care But, no one knows who will get sick If each person pays $100 into a “pool” they will collectively have $10,000 to cover the medical costs of the person who gets sick 99 people do not collect anything, but they gain peace of mind and important protection against a large loss So, everyone gives up $100, but nobody loses more than $100 Insurance shifts the risk of big loss from the individual to the insurance company

The benefits of Insurance Property & Liability • Payments received from an insurance policy can far exceed the premiums paid • Provides financial security and peace of mind Life Health Long-term Care Disability Why is the best outcome to have insurance but never collect on it?

The Insurance Process Claim – a formal request to an insurance company asking for a payment when the policyholder has an accident, illness or injury Event occurs resulting in loss Deductible – the out-of-pocket money paid by the policyholder before an insurance company will cover the remaining costs attributed to the loss Remaining amount owed is paid by co-insurance (if applicable) Policyholder makes claim to insurance organization Co-insurance – requires the insured individual to pay a fixed percentage of the loss after the deductible has been paid Insurance organization determines if event is covered by policy If so, policyholder pays a deductible

LOUISE’S ACCIDENT what if… Louise pays the first $500 of any covered medical care plus 20% of the remaining costs Even with insurance Louise still needs funds to pay the deductible and co-insurance Louise is in an accident resulting in a $5,000 medical procedure that is covered by insurance Louise pays $500 + 20% of the remaining $4,500 for a total of $1,400 The insurance company pays $3,600 What would Louise’s options have been if she did not have insurance?

You do the Math! Carlos was involved in an automobile accident that resulted in $3,788 worth of damage to his car. How much does Carlos pay and how much does the insurance organization pay? Carlos has a property and liability insurance policy with a $500 deductible and 0% co-insurance How much does Carlos pay? $500 How much does his insurance organization pay? $3,288

Which Insurance policy would you choose? Janet wants to make sure she has the best health insurance policy. She shopped around and received multiple quotes. What are the pros and cons of each policy? $300 $200 $2000 $200 20% owed by policyholder 80% owed by insurance organization 0% owed by policyholder 100% owed by insurance organization

Why do insurance policies include deductibles and co-insurance? Dollars paid from an insurance policy are not intended to make a person better off than before the loss happened

Sources of Insurance In most cases, individuals acquire insurance from a combination of sources Employer Special programs for those who qualify and during catastrophes Health, disability, and occasionally life insurance Government Individual

Employer Provided Insurance Employee benefits - products or services that add extra value for employees beyond earned wages In-kindincome – the donation of a product or service in place of cash Employer Payroll deduction Employee • Policies may be available to the employee’s family members (usually for additional fees) • No income taxes are paid on the in-kind income

Property & Liability Insurance Property insurance - payment to insured person if his/her property is damaged or destroyed by an accident Pays for loss to insured person Liability insurance - payment to others if a member of the insured household accidently causes harm to other people or property Pays for injury or loss to others Provided by individuals

Types of Property & liability Insurance Automobile insurance - payment for liability and property insurance on a vehicle If a person drives an automobile, automobile liability insurance is required by law Homeowners insurance - payment to cover liability losses and damage/loss of home structure and its contents Renters insurance - payment for damage/loss of property in a rental unit in addition to liability losses

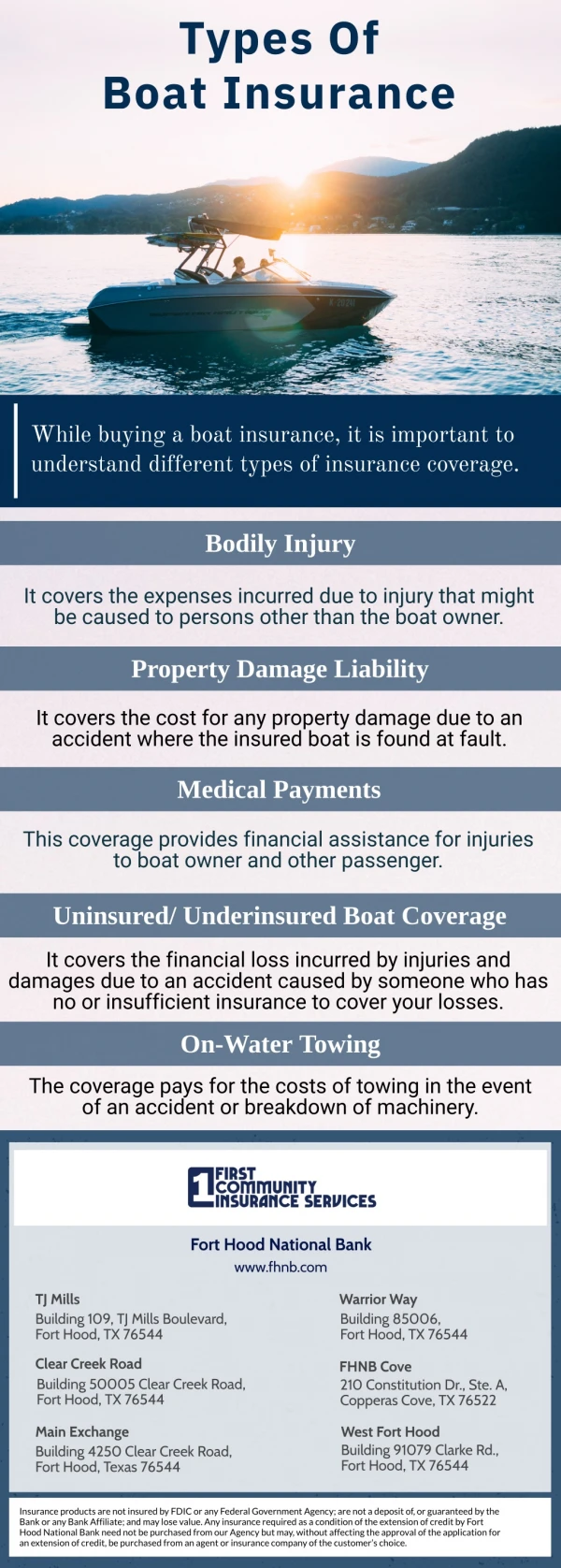

Automobile INSURANCE • 3 TYPES OF POTENTIAL LOSS WHEN OWNING OR OPERATING A MOTOR VEHICLE • LEGABLE LIABILITY • INJURY TO THE INSURED OR FAMILY MEMBER • DAMAGE TO THE VEHICLE • Six distinct coverage's • Bodily injury Liability • Medical Payments or Personal injury protection (pip) • Property Damage • Collision • Comprehensive • Uninsured/Underinsured motorist coverage

Bodily injury liability • If you are at fault in an accident, your liability coverage will pay for the bodily injury and property damage expenses caused to others. • If you do not have this you are susceptible to legal action • Liability is usually expressed in three numbers $100/$300/$50 • Each number represents $1,000 so:100,000/300,000/50,000. • First two numbers relate to bodily injury coverage. • The first number maximum number an insurance company will pay for the injuries of any one person in any one accident • The second number is the maximum amount the company will pay for all injured parties (two or more) • The third number is the maximum property damage per accident.

Medical Payments or Personal injury protection (pip) • Regardless of who is at fault, medical payments coverage will pay your medial expenses and those of your own passengers. • Covers you even if you are a pedestrian or a passenger in someone else’s car.

PROPERTY DAMAGE • Covers the damage done to someone else’s vehicle or personal property by the policy holder if the policyholder is at fault.

Collision • If you cause an accident you will need to have collision coverage to pay for the repair to your car. • If damages out weigh the value of a car then insurance company may total a vehicle. • Total-pay you the actual cash value of the car • Generally older vehicles with less value generally do not include this. • Because the cost of the market value of the car may be minimal.

Comprehensive (other than by collision) • Sometimes the insured suffers a loss that doesn’t involve an accident with another automobile. • Parked under a tree during a storm and a branch breaks landing on your car.

Uninsured/underinsured motorist coverage • If your involved in an accident with a driver who is uninsured, this coverage will pay for you injuries.

Factors that determine Premium • Vehicle Type • The make, year, and model will affect insurance cots. Vehicles that will require expensive replacement parts and complicated repair will cost more to insure • Rating Territory • In some states your rating territory is the place of residence used to determine your vehicle insurance premium. • Rural areas usually have fewer accidents and less frequent occurrences of theft, leading to lower insurance cost.

Factors that determine Premium.. • Driver Classification • Drivers under (25) and elderly drivers (over 70) have more accidents and serious accidents. As a result they have higher premium. • Cost and number of claims that you file will affect your premium, • To many claims may lead to termination of your policy and place you is an assigned risk pool. People cant get coverage with leads to them being assigned to each insurance company operating in the state. They pay several times the normal rate.

Reducing vehicle insurance premiums • Comparing companies • Premium discounts • Drivers ed • Insuring two or more vehicles with the same company. • Increasing the amounts of deductibles will also lead to lower premium

No Fault Insurance • Some states have adopted “No Fault Insurance” which works a little different then a standard policy. • Requires a driver to carry insurance of their own protection and limits their ability to sue other drivers for damages. • So if you are in an accident that is a “no fault” state is covered by their own insurance company regardless of who is at fault

If you are in an accident • What to do if involved in an accident • Read the students introduction to insurance

Go out and fill out some quotes • https://www.geico.com/information/coverage-calculator/# • https://www.libertymutual.com/auto-insurance/insurance-resources/auto-coverage-estimator • http://www.carinsurance.com/calculators/Coverage-Calculator.aspx • Finally good article read full of information • http://www.protectyoubetter.org/Research-Center/Car-Insurance.aspx

Home Owner Insurance • Is coverage that provides protection for your residence and its associated financial risks, such as damage to personal property and injuries to others. • Homeowner policy provides coverage for the following. • The building in which you live and any other structures on the property • Additional living expenses • Personal property • Personal liability and related coverage's • Specialized coverage's

Buildings and other structures • Protect against financial loss • Detached structures on your property, such as garages or toolsheds are also covered. • Homeowners coverage even include trees, shrubs, and plants.

Additional living expenses • If a fire or other event damages your home, additional living expense coverage pays for you to stay somewhere else. • Motel or apartment • Some policies limit additional living expense coverage to 10 to 20 percent of the home’s coverage amount. They may also limit payments to a maximum of six to nine months • Other policies may pay additional living expense for up to a year.

Personal Property • Covers you household belongings: • Furniture • Appliances • Clothing • Up to a portion of the insured value (Usually 55, 70, and 75 %) • Example home insured for $80,000 might have $56,000 (70 %) worth of coverage for household belongings. • Typically includes limits for the theft of certain items, such as $1,000 for jewelry.

Personal property cont. • Items you take on vacation or use at school are usually covered up to the policy limit. • Extends to property that you rent, such as a rug cleaner in your possession • If something does happen to your personal property, you must prove how much it was worth and it belonged to you. • Household inventory-is a list or other documentation of personal belongings, with purchase dates and cost information • Photographs and recordings may useful tools • Personal property floater • Is additional property insurance that covers the damage or loss of a specific item of high value. • How much its worth and its appraisal value.

Personal liability & Related coverage's • Personal liability • Protects you and members of your family if others sue you for injuries they suffer or damage to their property. Includes cost of legal defense • Friends and guests are more than likely covered • Babysitters, employees, housekeepers, and gardeners are not covered and you have to obtain worker’s compensation coverage for them. • Most homeowners policies provide basic personal liability coverage of $100,000 but often times that is not enough.

Personal liability & Related coverage's cont. • Related Coverage's • Umbrella policy-also called a personal catastrophe policy, supplements your basic personal liability coverage. • This additional protection covers you for all kinds of personal injury claims • Medial Payments coverage's-pays the cost of minor accidental injuries to visitors on your property. It also covers minor injuries caused by you, members of your family, or even your pets, away from home. • If you or a family member should accidentally damage another person’s property, the supplementary coverage of homeowners insurance will pay for it.

Specialized coverage’s • Homeowners insurance usually doesn’t cover losses from floods and earthquakes. If you live in an area that has frequent floods or earthquakes you need to purchase special coverage. • You may be able to get earthquake insurance as an endorsement -addition of coverage- to a homeowners policy or through a state-run insurance program.

Farm insurance • Operates very similar to home insurance • Combines Personal/Household coverage's together along with Farm/Ranch coverage's • Includes • Owner occupied dwelling • Household Personal Property • Scheduled Farm Personal • Farm Building and Structure • Personal liability and Farm.

Renters insurance • Includes personal property protection, additional living expense coverage, and personal liability and related coverage's.

Factors that affect home insurance costs • Location • Higher rates in areas with higher crime. Severe weather tornadoes and hurricanes. • Type of Structure • A brick house will usually cost less to insure than a similar structure constructed with wood. However earthquake coverage is more expensive for brick house than for wood. • Coverage amount and policy type • Deductible amount in your policy also affects the cost of insurance. • Home Insurance discounts • Taking certain action to reduce risks: Security systems, smoke alarms, and fire extinguishers . • Comparing Companies

Risks Covered Health Insurance Provided by Employer Health insurance - provides money to pay for health care Government And/or Individual If dollars are limited, health insurance is extremely important to protect against high medical bills Mental health treatment Hospital bills Preventative care Vision care Prescription drugs Doctors’ visits Medical procedures Dental care

Health Insurance • Is a form of protection that eases the financial burden people may experience as a result of illness or injury. • You pay a premium to the insurer. In return the company covers most of your medial costs. • Coverage’s vary on what they cover but they may reimburse you for hospital stats, doctor’s visits, medications, and sometimes vision and dental care

Group Health Insurance • Generally employer sponsored • Offer the plans and usually pays some or all of the premiums • Labor unions and professional associations also sometimes offer group insurance plans. • Cost is fairly low because many people are insured under the same policy.

Individual Health insurance • Purchase individual health insurance directly form the company of your choice. • Plans usually cover you as an individual or cover you and your family.

COBRA • Consolidated Omnibus Budget Reconciliation Act of 1986 • If a person is let go and was part of a group insurance program, it will allow you to keep that coverage for a set period of time. • You have to pay the premium yourself but at least coverage was not dropped. • Not everyone qualifies for COBRA. You have to work for a private company or a state or local government to benefit

Basic Health Insurance Coverage • Hospital Expense • Surgical Expense • Physician Expense

MAJOR medical expense Insurance • Pays large costs involved in long hospital stays or multiple surgeries. • In other words it takes up where basic health insurance coverage leaves off. • Almost every type of care and treatment prescribed by a physician , in or out of a hospital is covered. • Requires a deductible, coinsurance • Stop loss-is a provision that requires the policyholder to pay all cost to a certain amount, after which the insurance company pays 100 percent of the remaining expense as long as they are covered in the policy.

Hospital indemnity policies • Pays benefits when you’re hospitalized. Unlike most of the other plans mentioned, however these policies don’t directly cover medial costs. Instead you are paid in cash, which you can spend on medical or nonmedical expenses as you choose. • Premium generally much higher.

Medicare • National social insurance program administered by the U.S. government that guarantees access to health insurance for Americans age 65 and older who have worked and paid into the system. • Run by Social Security Administration (SSA)and funded by employee payroll deductions and matching employer contributions (1.45%) • Generally retired people pay a monthly premium for Medicare insurance, which is deducted from their Social Security payments. • 4 parts • Hospital insurance, medical insurance, advantage health plans, and prescription drug costs.

Medicaid • Government sponsored health insurance for people with incomes and limited resources. • Helps families living in poverty and helps those who cannot afford private health insurance to pay the costs associated long-term medical and custodial care. • Each state operates it s own Medicaid system. • The Federal Gov funds up to 50% of the cost of each state’s Medicaid program.

Social Security Disability • Anyone who is 65 or older. Blind or disabled and has limited income/resources. • Pays benefits to people who can not work because they have a medical conditions, that is expected to last at least one year or result in death. • If you have Social Security taxes deducted from your paycheck you are entitled to disability payments from Social Security in the event you become disabled and cannot work. • Have to meet certain standards • Pass their application test • http://www.ssa.gov/pubs/EN-05-10029.pdf