Download

1 / 11

110 likes | 407 Views

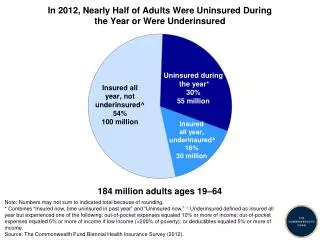

A central focus of this conference is the problems of the uninsured (and underinsured). 47 million uninsured in 2006 18,000 Americans die each year from lack of insurance Results in financial distress and disaster for many Americans. But some argue a more important problem is “overinsurance”.

E N D

A central focus of this conference is the problems of the uninsured (and underinsured) • 47 million uninsured in 2006 • 18,000 Americans die each year from lack of insurance • Results in financial distress and disaster for many Americans

But some argue a more important problem is “overinsurance” • The “consumer-driven health care” movement contends consumers must become responsible for health care purchasing • Consumers purchase too much health care now because they have too much insurance, and insurance reduces the cost of health care causing moral hazard

Insurance is necessary, but • Only catastrophic insurance is really needed • High deductible health insurance policies (HDHPs) should be accompanied by health savings accounts (HSAs)

HDHPs coupled with HSAs will • Limit consumer purchases to truly necessary care • Create competition at the point of sale of health care items and services • Encourage consumers to shop for quality and price • Make health insurance more affordable • Bring down cost while improving quality and access

The Medicare Modernization Act • Tax exclusion to employers and a deduction to employees for funds contributed to an HSA. • HSA must, however, be coupled with a HDHP • Deductible of at least $1100 a year for a single individual or $2200 a year for family coverage. • HDHP must also have caps on out of pocket expenditures, cannot exceed $5600 for an individual and $11,200 for a family. • Tax subsidies for contributions up to $2900 for individual coverage and $5800 for family coverage. • Penalty if not spent for qualified medical expenses. • Can withdraw funds at 65

HSAs have caught on • 6.1 million Americans covered • 1.5 million individual policies, 4.6 million group members • 7% of employers offer • 3% of employees enrolled

Successes • 46% over 40 • Significantly more likely to engage in preventive programs • More likely to track health care expenses

But reasons to be concerned • Disproportionately attracts wealthy, healthy, young, well educated • Coverage often limited • Many Americans can’t afford high cost-sharing • Many enrollees limit necessary care • Many end up in financial distress

Patients as consumers • Should patients be primarily responsible for controlling health care costs? • Rand Health Insurance Experiment found that high cost sharing caused decrease in expenditures, but for essential as well as inessential care • Sick patients are not well-positioned to make purchasing decisions • Cost and quality data are largely lacking • Consumers may not be the best care coordinators

Changes in the physician patient relationship • Informed consent? • Liability where patient chooses not to purchase care? • Liability of insurers for erroneous quality advice? • Liability of insurers to providers for erroneous quality advice?

Is there a place for CDHC? • Yes, empowering consumers is fine • But markets only work for those that have money • Purchasing necessary health care should not result in financial disaster • We need universal coverage first, then we can try to make those who have resources better consumers