Download

1 / 24

240 likes | 269 Views

Exploring the role of profit in motivating producers and the law of supply in relation to quantity offered at different prices. Learn how prices influence suppliers' willingness and ability to increase quantity supplied over time.

E N D

Economics Chapter 5-Supply Section 1: The Supply Curve

Law of supply • With demand, the assumption is that consumers try to maximize utility, a goal that motivates their behavior. • With supply, the assumption is that producers try to maximize profit. • Profit is the goal that motivates the behavior of suppliers.

Role of profit • In trying to earn a profit, firms transform productive resources into products. • Profit equals total revenue minus total cost. Profit = Total revenue – Total cost

Total revenue is the total sales, or total dollars, received from consumers for the day, a week, or a year. • Total cost includes the cost of all resources used by a firm in producing goods or services, including the entrepreneur’s opportunity cost.

When a firm breaks even, total revenue just covers total cost. Over time, total revenue must cover total cost for the firm to survive. • It total revenue falls short of total cost year after year, entrepreneurs will find more attractive uses for resources, or the firm will fail.

Each year, millions of new firms enter the U.S. marketplace and nearly as many leave. • The lure of profit is so strong that entrepreneurs are always eager to pursue their dreams.

Supply • Just as demand is relation between price an quantity demanded, supply is a relation between price and quantity supplied. • Supply indicates how much of a good producers are willing and able to offer for sale per period at each possible price, other things constant.

The law of supply says that the quantity supplied is usually directly related to its price, other things constant.

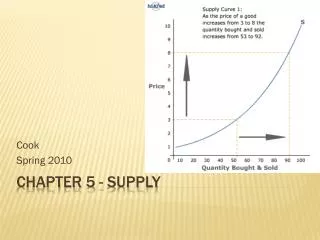

Supply curve- a curve or line showing the quantities of a particular good supplied at various prices during a given time period, other things constant.

Like the demand curve, the supply curve represents a particular period of time. • For any supply curve, it is assumed that the prices of other goods the business could produce remain unchanged.

More Willing to Supply • Producers offer more for sale when the price rises for two reasons. • 1. as the price increases, other things constant, a producer becomes more willing to supply the good. • 2. Prices act as signals to existing and potential suppliers about the rewards for producing various goods. An crease in the price, with other prices remaining constant, creates an incentive to shift some resources out or producing other goods, whose prices are now relatively lower and into another product whose price is now relatively higher.

More able to supply • Higher prices also increase the producer’s ability to supply the good. • The cost of producing an additional unit of a good usually rises as output increases- that is, the marginal cost of production increases as output increases.

Because suppliers face a higher marginal cost for producing the good, they must receive a higher price to be able to increase the quantity supplied. • A higher price makes producers more able to increase quantity supplied.

Example: A higher price for gasoline in recent decades increased producers’ ability to explore for oil in less-accessable areas, such as the remote jungles of the Amazon, the stormy waters of the North Sea, and the frozen tundra above the Artic Circle. • Thus the quantity of oil supplied increased as the price increased.

On the other hand, a two decade long slide in the price of gold means producers are no longer able to mine gold in less accessable regions where each ton of ore holds less gold. • As the price declined, the quantity supplied decreased.

In short, a higher price makes producers more willing and better able to increase quantity supplied. • Suppliers are more willing because production of the higher priced good now is more profitable than the alternative uses of the resources involved. • Suppliers are better able because the higher price allows them to cover the higher marginal cost that typically results from increasing production.

Supply Versus Quantity Supplied • As with demand, economists distinguish between supply and quantity supplied. • Supply is the entire relation between the price and quantity supplied, as reflected by the supply schedule or supply curve. • Quantity supplied refers to a particular amount offered for sale at a particular price, as reflected by a point on a given supply curve.

Thus, it is the quantity supplied that increases with a higher price, not supply. • The term supply by itself refers to the entire supply schedule or supply curve.

Individual supply and market supply • Individual supply- the supply of an individual producer. • Market supply – the supply of all producers in the market. • In most markets, there are many suppliers, sometimes thousands.

The market supply curve is simply the horizontal sum of the individual supply curves for all producers in the market.

Elasticity of Supply • Prices are signals to both sides of the market about the relative scarcity of products. • High prices discourage consumption but encourage production. • The elasticity of demand measures how responsive consumers are to a price change. • Likewise, the elasticity of supply measures how responsive producers are to a price change.

Measurement • The elasticity of supply is calculated in the same way as the elasticity of demand. • The elasticity of supply equals the percentage change in quantity supplied divided by the percentage change in price. Elasticity of supply= Percentage change in quantity supplied ____________________________ Percentage change in price

Categories of supply • If supply elasticity exceeds 1.0, supply is elastic. • If it equals 1.0, supply is unit elastic. • If supply is less than 1.0, it is inelastic.

Determinants of Supply Elasticity • The elasticity of supply indicates how responsive producers are to a change in price. • Their responsiveness depends on how costly it is to alter output when the price changes. • The elasticity of supply is typically greater the longer the period of adjustment.