Download

1 / 11

110 likes | 343 Views

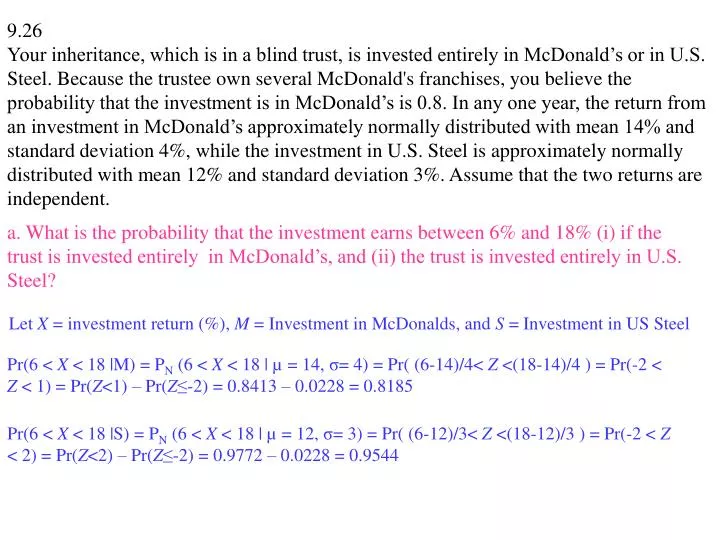

9.26

E N D

9.26 Your inheritance, which is in a blind trust, is invested entirely in McDonald’s or in U.S. Steel. Because the trustee own several McDonald's franchises, you believe the probability that the investment is in McDonald’s is 0.8. In any one year, the return from an investment in McDonald’s approximately normally distributed with mean 14% and standard deviation 4%, while the investment in U.S. Steel is approximately normally distributed with mean 12% and standard deviation 3%. Assume that the two returns are independent. a. What is the probability that the investment earns between 6% and 18% (i) if the trust is invested entirely in McDonald’s, and (ii) the trust is invested entirely in U.S. Steel? Let X = investment return (%), M = Investment in McDonalds, and S = Investment in US Steel Pr(6 < X < 18 |M) = PN (6 < X < 18 | µ = 14, σ= 4) = Pr( (6-14)/4< Z <(18-14)/4 ) = Pr(-2 < Z < 1) = Pr(Z<1) – Pr(Z≤-2) = 0.8413 – 0.0228 = 0.8185 Pr(6 < X < 18 |S) = PN (6 < X < 18 | µ = 12, σ= 3) = Pr( (6-12)/3< Z <(18-12)/3 ) = Pr(-2 < Z < 2) = Pr(Z<2) – Pr(Z≤-2) = 0.9772 – 0.0228 = 0.9544

Pr(M|X >12) = Pr(M|X >12) = b. Without knowing how the trust is invested, what is the probability that the investment earns between 6% and 18%? Pr(6 < X < 18) = Pr(6 < X < 18 ∩ M) + Pr(6 < X < 18 ∩ S) = Pr(6 < X < 18 |M) Pr(M) + Pr(6 < X < 18 |S) Pr(S) = 0.8185 (0.8) + 0.9544 (0.2) = 0.8457 c. Suppose you learn that the investment earned more than 12%. Given this new information, find your posterior probability that the investment is in McDonald’s Pr(X >12) = Pr(X >12 ∩ M) + Pr(X >12 ∩ S) = Pr(X >12|M) Pr(M) + Pr(X >12|S) Pr(S) Pr(X >12|M) = PN (X > 12| µ = 14, σ = 4) = Pr(Z > (12-14)/4) = Pr(Z >-0.5) = 1 – Pr(Z≤ -0.5) = 1- 0.3085 = 0.6915 Pr(X >12|S) = PN (X > 12| µ = 12, σ = 3) = Pr(Z > (12-12)/3) = Pr(Z >0) = 1 – Pr(Z≤ 0) = 1- 0.5 = 0.5 Pr(X >12) = 0.6915* 0.8 + 0.5*0.2 = 0.6532

9.35 • A factory manager must decide whether to stock a particular spare part. Stocking the part costs $10 per day in storage and cost of capital. If the part is in stock, a broken machine can be repaired immediately. But if the part is not in stock, it takes one day to get the part from the distributor, during which time the broken machine sits idle. The cost of idling one machine for a day is $65. There are 50 machines in the plant that require this particular part. The probability that any one of them will break and require the part to be replaced on any one day is only 0.004, regardless of how long since the part was previously replaced. The machines break down independently of one another. • If you want to use a probability distribution for the number of machines that break down on a given day, would you use the Binomial or Poisson distribution? Why? • Whichever theoretical distribution you chose in part a, what are the appropriate parameters? That is, if you chose Binomial, what are the values for p and n? If you chose Poisson, what is the value for m? • If the plant manager wants to minimize his expected cost, should he keep zero, one, or two parts in stock? Draw a decision tree and solve the manager’s problem. (Do not forget that more than one machine can fail in one day!)

X = # of machines that break down on a given day • Reasons for using Binomial distribution: 1) The number of machines that break down at any point can be between 0 and 50; 2) all machines have the same probability of breaking down; 3) machines seem to break down independently of each other • Reasons for using Poisson distribution: 1) The probability of breaking down is very small; 2)Breaking down can happen at any time during the day; 3) machines seem to break down independently of each other • If we use the Binomial distribution, then n=50, p=0.004 • If we use the Poisson distribution, then m=50*0.004=0.2

# of parts required (breakdowns) Total Cost 0 (p1) $0 1 (p2=?) -$65 $65 Stock 0 part 2 (p3=?) -$130 $130 3 (1-p1-p2-p3) -$195 $195 0 (p1) $10 1 (p2=?) $10 Stock 1 part 2 (p3=?) -$65 -$10 $75 3 (1-p1-p2-p3) -$130 $140 0 (p1) $20 1 (p2=?) $20 Stock 2 parts 2 (p3=?) -$20 $20 3 (1-p1-p2-p3) -$65 $85 c. . . Decision Tree

Using Binomial Distribution, i.e. X~ B(n=50, p=0.004) You cannot find probabilities of Binomial distribution using the tables in Appendix A when p=0.004, but you can calculate it using the formula of the PMF of the Binomial distribution or statistical tools Pr(X=0) = 0.819, Pr(X=1) = 0.164, Pr(X=2) = 0.016, Pr(X=3) = 0.001 E(cost|stock 0) = 0(0.819) + 65(0.164) + 130(0.016) + 195(0.001) = $12.935 E(cost|stock 1) = 10(0.819) + 10(0.164) + 75(0.016) + 140(0.001) = $11.17 E(cost|stock 2) = 20(0.819) + 20(0.164) + 20(0.016) + 85(0.001) = $20.065 Using Poisson Distribution, i.e. X~ Poisson(m=0.2) You can use tables in Appendix C to find the probabilities, and it turns out that the probabilities of X=0, 1, 2, 3 are the same as those in the Binomial distribution In conclusion, the preferred alternative is to stock 1 part

12.7 • You have mineral rights on a piece of land that you believe may have oil underground. There is only a 10% chance that you will strike oil if you drill, but the payoff is $200,000. It costs $10,000 to drill. The alternative is not to drill at all, in which case your profit is zero. • Draw a decision tree to represent your problem. Should you drill? Because EMV(Drill) = $10k > EMV (Don’t drill) = 0, you should drill

c. Use decision tree to calculate EVPI If you could consult a clairvoyant with perfect information EMV(with perfect information) = 190*0.1 + 0 *0.9 = $19k EVPI = EMV(with perfect information) - EMV(without information) = $19 K - $10 K = $9 K

(?) (?) (?) (?) (?) (?) d. Before you drill you might consult a geologist who can assess the promise of the piece of land. She can tell you whether your prospects are “good” or “poor”. But she is not a perfect predictor. If there is oil, the conditional probability is 0.95 that she will say prospects are good. If there is no oil, the conditional probability is 0.85 that she will say poor. Draw a decision tree that includes the “Consult Geologist” alternative. Finally, calculate the EVII for this geologist. If she charges $7000, what should you do?

Given: Pr (“good” | oil) = 0.95, Pr(oil) = 0.1, Pr(“poor” | dry) = 0.85, and P(dry) = 0.9 According to the law of total probability: Pr(“good”) = P(“good” | oil) P(oil) + P(“good” | dry) P(dry) = 0.95 (0.1) + 0.15 (0.9) = 0.23 Pr(“poor”) = 1 - P(“good”) = 1 - 0.23 = 0.77 Using Bayes Theorem Pr(oil | “good”) = Pr(“good” | oil) * Pr(oil) / Pr(“good”) = 0.95*0.1/0.23 = 0.41 Pr(dry | “good”) = 1- Pr(dry | “good”) = 1 - 0.41 = 0.59 Pr(oil | “poor”) = Pr(“poor” | oil) * Pr(oil) / Pr(“poor”) = 0.05*0.1/0.77 = 0.0065 Pr(dry | “poor”) = 1- Pr(oil | “poor”) = 1 - 0.0065 = 0.9935

EVII = EMV(Consult Geologist) - EMV(Drill) = $16.56 K - $10 K = $6.56 K Because EVII is less than $7000, which the geologist would charge, you shouldn’t consult her.