Download

1 / 65

650 likes | 778 Views

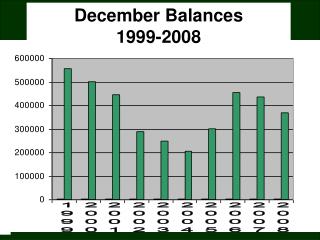

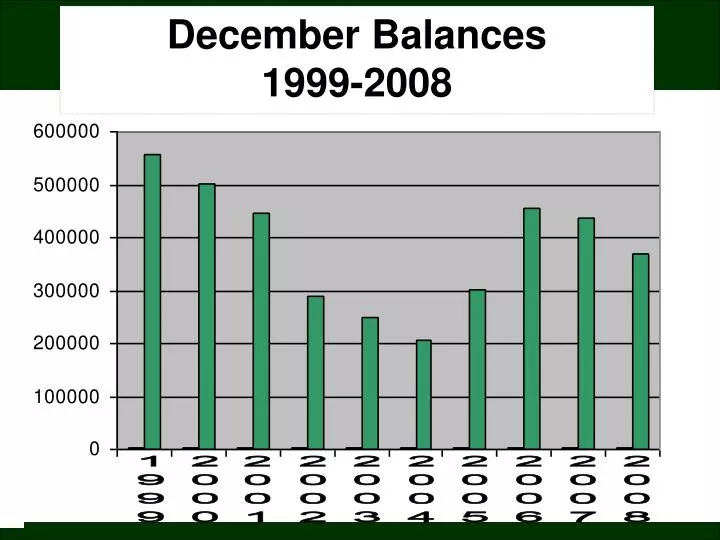

December Balances 1999-2008. 1999. 2000. 2001. 2002. 2003. 2004. 2005. 2006. 2007. 2008. ADM Count 1973-2009. http://mustang.doe.state.in.us/SEARCH/snapcorp.cfm?corp=6805. http://mustang.doe.state.in.us/TRENDS/corp.cfm?corp=6805&var=sal. School Consolidation Options

E N D

December Balances 1999-2008 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

http://mustang.doe.state.in.us/SEARCH/snapcorp.cfm?corp=6805

http://mustang.doe.state.in.us/TRENDS/corp.cfm?corp=6805&var=salhttp://mustang.doe.state.in.us/TRENDS/corp.cfm?corp=6805&var=sal

School Consolidation Options • IC 20-23-4-38; Further Reorganization of School Corporations (School Corporation Reorganization Act of 1959) • Summary-School board (or school boards acting jointly) submit proposed plan for further reorganization of schools in the County. Plan must meet requirements of 1959 Act. If approved by State Board of Education, after hearing in County, plan must be adopted by petition signed by 55% of voters in proposed new corporation or by receiving majority of votes cast at special election. • Initiated by: School board or school boards or State Superintendent • Challenged by: Testimony in opposition at State Board hearing; not signing petition; voting “no” at election • State approval: Yes • Unique features: Presumably may be initiated unilaterally by one School board; always requires affirmation by voters • IC 20-23-5; Territory Annexation • Summary – School boards adopt resolution under which one corporation annexes all of territory of another school corporation. • Initiated by: School boards • Challenged by: Remonstrance lawsuit, with grounds limited and specified in statute • State approval: No • Unique features: No state approval; challenged in court

School Consolidation Options (continued) (3) IC 20-23-6; Consolidation Summary-School boards adopt joint resolution, which is subject to protest petition signed by 20% of voters of either school corporation and special election in the protesting corporation. As an alternative to school board resolution, 20% of voters in each corporation may petition for consolidation, which results in special election Initiated by: School boards or voters Challenged by: protest petition and special election State approval: Yes Unique features: May be initiated by voters; may be defeated by voters of one corporation

Indiana Department of Education Cost Saving Considerations Budgetary/Administrative Considerations • Eliminate insurance payments for all school board personnel • Increase insurance deductibles • Investigate moving to state employee health benefit plan or another shared plan • Guarantee all school employees contribute equally and equitably to insurance plans • Freeze all expenditures at current levels • Roll back budgets to prior year where appropriate • Reduce all non instructional budgets • Consider participation fees or eliminating for extracurricular activities • Creation of nonprofit foundation or endowments to support school district • Suspend all capital outlays until budget plan is determined • Eliminate pay for membership into professional organizations or associations • Shared legal and other professional services • Utilization of technology to deliver instructional materials • Require electronic funds transfer for all payroll and payments • Limit or eliminate subscriptions and publications • Limit or eliminate reimbursable travel • Eliminate cell phone, Blackberry and pager costs • Utilize community resources to create efficiencies and supplement programs • Explore volunteerism within the local community • Examine all vendor contracts in excess of $1,000 • Renegotiate purchasing agreements • Buy bulk • Buy online • Cooperative purchasing agreements • Pursue inter-local agreements • Purchase from state QPA’s

Indiana Department of Education Cost Saving Considerations (Continued) Personnel/Staffing Considerations • Suspend Hiring • Initiate rigorous contract negotiations within the confines of local fiscal health • Freeze salaries at current levels • Suspend salary increment for biennium • Roll back salaries to previous year levels • Eliminate any overtime pay • Examine retire to rehire opportunities • Examine early retirement incentive • Furlough non instructional employees • Reduce central office staff • Reduce all administrative and clerical staff • Reduce or eliminate paid lay staff • Examine need for ancillary staff Operating/Capital Project Considerations • Close underutilized buildings • Reduce or mothball square footage in existing buildings • Track and monitor monthly utilities and other fixed costs. Consider budget plans or prepaid plans • Examine the outsourcing of transportation, cafeteria and janitorial services • Reduce or eliminate school vehicle inventories • Monitor school facility usage for potential of establishing hours of operation • Sell or lease surplus property or facilities • Freeze all building projects that are not general fund neutral • Freeze all nonessential building upgrades

Indiana Department of Education Cost Saving Considerations (Continued) Policy Considerations • Shared services inside and outside school districts • Evaluate benefits of school consolidation • Operating referendum • Written policies to support anonymous reporting and investigation of claims of fraud, waste and abuse • Investigate programs designed to retain and recruit students • Examine corporations grade level delivery ststem • Increase student/teacher ratio; larger classes; team teaching • Examine partnerships with local government Legislative Considerations • Allow for transportation and capital funds to be used for 2010 General Fund shortfall • Allow a levy access transfer • Local Option Income Tax (LOIT) for schools • Delay circuit breaker • Require a state hiring salary freeze for all state funded employees • Change referendum language

2008 - 2009 Management SurveyIssued May 4, 2009ISBA Indiana Superintendents: 2008/09 Average Superintendent Salary for Indiana:$111,072 Days worked:260 Average daily earnings for 2008/09:$427.20/day2008/09 Average Teachers' Salaries at Top of Masters Schedules:$61,457 Average Days Worked:184 Average daily earnings for 2008/09:$334.01/day

2008-2009 State Superintendent Averages Wages: • $111,072 • Benefits • Paid TRF • Annuity $6,981 • Health $15,192 • Life $303 • LTD $434 • Mileage 50 cents per mile • Some school corporations pay for a car or a car allowance • Contract Days: • 254 days • 3.91 weeks of vacation (20 days) • Some schools have other paid central office management positions: • business managers • curriculum directors • assistant superintendent (s) • director of transportation • special education directors • RSSC has one central office administrator and each building has one principal. • Our central office has all the jobs above shared among the four of us, which saves RSSC a lot of money. • The three RSSC administrators are foregoing a possible raise in the 2009-2010 school year. • I have said, as superintendent, I will forego any raise through June 30, 2013 if that helps keep RSSC alive.

General Fund – 100% paid by Indiana 1-1-09 State Support - $6,000/per student 2010 – 0.87 less than 2009 (now 3 – 3.5% cut by Governor for 2010) 12 months not 18 2009 – 3,845,957 2010 – 3,812,379 -0.87 = 33,578 3% = $114,371 3.5%= $133,433 2010 total Loss 33,578 33,578 3% 114,371 3.5% 133,433 $147,949 $167.011 General Fund is used for salaries, benefits, utilities, unemployment, etc.

Form 9 July 1, 2008 to June 30, 2009 General Fund 88.74% -Certified Salaries and Benefits -Non-Certified -School Board -Administration This left only 11.26% for utilities, unemployment, etc. Form 9 January 1, 2009 to June 30, 2009 Salaries and Benefits 91.12% Other Funds – county tax monies Loss CPF $1,649 Transportation $1,018 Bus Replacement $ 160 Severance/Pension Debt $ 292 Debt Service $ 838 -2009 circuit breaker - $3,957 2010 circuit breaker – loss in revenue in these funds again 2010 approved budget – General Fund, CPF and Transportation appropriations were reduced by the DLGF. *Will the state make further cuts in K-12 public education?

K-12 EDUCATION FUNDING REDUCTIONS On December 28, 2009, Governor Daniels announced that funding for K-12 Education would be reduced by $297 million in calendar year 2010 beginning with the January distribution. The State Budget Agency has recently determined that the amount of savings needed to balance the stat’s budget from public school education funding is $298,437,168. The Budget Agency in conjunction with the Department of Education has developed a methodology to make the reductions to each school corporation. The DOE will be distributing a new DOE 54 on January 14th that will reflect the reductions and methodology. It is extremely important that you review this document carefully so that you are aware of the actual reduction amount for your school corporation. In comparing the total 2009 tuition support actual amount with the new 2010 state total (which reflects the $298+ million reduction), there is an approximate $189 million reduction or 3%. This is the percentage of decrease that the administration is stating that school corporations are facing. The issue here is that school corporations built their 2010 General Fund budgets based on the actions of the 2009 General Assembly. These budgets were approved last fall with the assumption that state monies approved last June would flow to school corporations. The state’s final crisis has changed the environment, but not the assumptions that were used last year to develop the 2010 expenditure plan including staffing.

K-12 EDUCATION FUNDING REDUCTIONS (continued) In reality, school corporation General Fund budgets for 2010 will need to be reduced by the $298+ million or 4.557%. The methodology created to make the 2010 reductions cuts that amount (4.557%) from the 2010 formula calculation adopted by the 2009 General Assembly for every school corporation. The above is a brief overview of the impact for 2010. A more important issue is that the reduction is PERMANENT. When the 2011 state support formula is being developed by each corporation, the starting point will be the previous year’s revenus. That amount will be the 2010 reduced formula calculation.

Administration Governor Daniels has stated Indiana Districts with less than 1,000 students have “too many superintendents and an array of assistant superintendents..” THE TRUTH The 48 districts in Indiana with less than 1,000 students employ 44.75 full-time superintendents. This is less than one superintendent per district (.3). Indiana ranks 49th among the 50 states in the number of central office certified personnel. Only Arizona ranks lower. This information has been sent to the governor by the Indiana Association Public School Superintendents. In Randolph County there are five school corporations with 4.5 superintendents, as Union has a part-time superintendent. RSSC has one (1) elementary principal, one (1) jr./sr. high school principal and one (1) superintendent.

Indiana State Budget, Appropriations, Fiscal Year 2008 Total Appropriations: $12,986 million All Other 7% Public Safety 6% K-12 Education 37% Health & Social Services 7% Property Tax Relief 18% Higher Education 13% Medicaid 12% Indiana State Budget, Appropriations, Fiscal Year 2011 Total Appropriations: $14,512 million All Other 7% Public Safety 6% Health & Social Services 9% K-12 Education 53% Medicaid 13% Higher Education 12%

Demographics • Population • A. County – slight decline • B. School age – steady decline • Economic • A. Employment • B. Income • C. Commuter Patterns • D. Children in Poverty • School Enrollments • A. History – steady decline • B. Projection – continuing decline

Curriculum • Open enrollment • Shared educational programs • Shared staff • Calendars • Schedules • Transportation • Funding/transfer cost • AP/ACP classes • Career/vocational programs • Higher expectations • Curriculum development

Administrative Costs • Centralize business services A. Software B. Calendar and pay schedule • Consolidate central administration and business services A. Current staffing B. Consolidate staffing C. Potential savings

Transportation • Directors, mechanics • 63 buses, 1500 miles per day • 71 drivers – $660,000

Facilities • Effects of collaboration/consolidation • Building Issues • Community facilities • Capacity

Maintenance • Consolidation of services • Contractors • Purchasing

Technology • Directors, technicians • Systems compatibility • Centralized plan • Common software: • Student management • Budget/finances • Transportation • Food services

Community • Athletics and Extra curricular • Volunteers and financial support • Scholarships • Partnerships

Finances • Comparison of expenditures by fund • Tax rate and assessed valuation comparisons • Teacher Contract Issues A. Salary B. Benefits C. Other provisions

THE COLLABORATION/CONSOLIDATION STUDY TEAMRECOMMENDATIONSFOR RANDOLPH COUNTY SCHOOL CORPORATIONS(Randolph Central, Randolph Eastern, Randolph Southern, Union)

School Years 1 to 2: • Calendars • Schedules • Open-enrollment • Special education services • Summer school programs • School software • Common student management program • Curriculum programs

School Years 3 to 5: • Consolidation of School Boards • Consolidation of Central Administration • Master Contracts • Centralization of other services • Career/Vocational programs

School Years 6 and beyond: • Review of schools and educational needs • Career Center • Consolidation/Community

Randolph Central School Corporation Randolph Eastern School Corporation Randolph Southern School Corporation Union School Corporation Collaboration/Consolidation Study By: Administrator Assistance October 30, 2008

Population projections for the future of Randolph County would suggest a rather steady, slow decline. While the overall population is projected to decline, a relatively sharp increase could be anticipated among senior citizens over the next 20 to 25 years. The median age will increase as the senior citizen segment of the population expands and the under age groupings decline. Estimates from the US Census Bureau

Enrollment projections for the Randolph Central, Randolph Eastern, Randolph Southern, and Union school corporation would suggest steady to slightly declining enrollments over the next few years. Historical demographic data show a rising diversity of school population, increasing special education population, and a greater percentage of children receiving lunch and textbook assistance.

School Enrollments (Actual/Projections) Randolph Southern School Corporation Date of Projection: August 2008 (Actual 2003-04 through 2007-08) (Projected enrollments 2008-09 through 2017-18) Indiana Department of Education

2. Curriculum Questions regarding curriculum were posed as a part of the Collaboratin/Consolidation Study involving Randolph Central, Randolph Eastern, Randolph Southern, and Union School Corporation. One question initiated prior to the study was could the school corporations incorporate an open enrollment concept or share educational programs and staff particularly at the high school level? An open enrollment concept could be beneficial for the students in all Randolph County school corporations. Such a concept would allow students to enroll in academic programs including those co-curricular programs that they might not be able to enroll in at their “home” high schools. The inability to take a class could be the result of a number of factors including limited number of teachers, scheduling restrictions, limited student enrollment, and/or funding limitations. There are a number of different classes offered in the four high schools.

Open enrollment for Randolph County students could take at least two forms. One form of open enrollment would allow a student living outside of a given school corporation, but within the county, to transfer to another Randolph County school corporation’s high school for academic reasons. A second from of open enrollment would provide the opportunity for a student to attend selected classes (part time enrollment) at another Randolph County high school in order to take courses not available to them in their own school corporation. During interviews and general discussions with the various stakeholder groups associated with each school corporation (students, parents, teachers, board members, administrators, other school employees, taxpayers and community leaders), an area of concern that was commonly mentioned was the need for more class offerings at the high schools in the area of Advanced Placement classes and college-dual credit courses. There was also a great deal of interest in providing more classes in the areas of foreign languages, technology, sciences, mathematics and business. Open enrollment could be one method of helping to meet the needs of students in these areas.

Randolph Southern School Corporation (Facility Information)

Student to Teacher Ratios By Corporation (2007-2008)

The issue of building needs does enter into consolidation decisions. Patrons of any school district pay for the initial cost of the school buildings (lease-purchase) and future renovations and/or additions to those buildings within their school corporation. This payment is part of their school taxes. These tax funds are allocated into the various school corporation funds, including the Debt Service Fund. The debt payments are paid out throughout the year (similar to mortgage payments). When school corporation consolidate, the property owners in the various districts still have the responsibility to pay for “Debt” incurred prior to the consolidation, but any “Debt” incurred after the consolidation becomes the responsibility of all taxpayers living in the “new corporation” boundaries. An area of contention between consolidating school corporations may arise when a school corporation with “good” school facilities consolidates with a district with facilities in need of major renovations and upgrades. Again, after consolidation all taxpayers from the consolidated corporations (now the “new” school corporation) are responsible for any new debt incurred with the renovation/upgrade of any building within the “new corporation”.