Download

1 / 22

220 likes | 314 Views

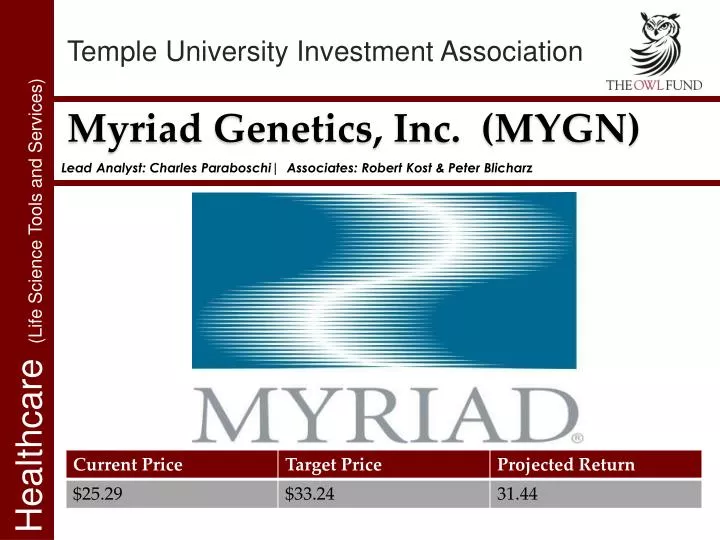

Lead Analyst: Charles Paraboschi | Associates: Robert Kost & Peter Blicharz. Myriad Genetics, Inc. (MYGN). Healthcare (Life Science Tools and Services ). Theory for Investment. Why is it cheap? Trading at discount to peers because of Law Suit speculation Why is it remaining cheap?

E N D

Lead Analyst: Charles Paraboschi| Associates: Robert Kost & Peter Blicharz Myriad Genetics, Inc. (MYGN) Healthcare (Life Science Tools and Services)

Theory for Investment • Why is it cheap? • Trading at discount to peers because of Law Suit speculation • Why is it remaining cheap? • Investors are making false assumptions about the court case, and they are completely ignoring revenue growth and pipeline prospects • Why will it go up? • The stock price will go up because revenue growth is going to remain strong and good news about the pipeline will drive it up

Legal Environment • On Nov. 30, 2013, the Supreme Court granted certiorari to review an earlier case regarding Myriad Genetics’ BRACAnalysistesting patents. • Unfortunately, these tests are Myriads most profitable tests contributing to 74% of their total revenues. • BRACAnalysis Tests for Breast and ovarian cancer.

Impact on Revenues • Will have no adverse effect on MYGN’s revenues, Why? • An adverse decision would only void any patent protections MYGN enjoys on BRAC 1 and BRAC 2. -& - • Although the patent void would open MYGN to competition, MYGN is and remains the only provider of such services. • It would take competitors 4 – 6 years to develop and market a generic test. • Oral Arguments on April 15th, final decision June30th.

Economic Moats • Market domination on BRAC 1, BRAC 2 testing with flagship BRACAnalysis. • Maintains many strategic patents, providing pricing power until 2018.

Balance Sheet Analysis • Cash & ST Investments have increased every year since FY2008, with one exception in 2011. • This is when MYGN acquired Rules Based Medicine for $80 million now accretive earnings of $25-$28 million as of last earnings release. • No debt financing. • Accounts Receivable growing at a decreasing rate relative to revenues, much lower than competitors.

Balance Sheet Analysis • MYGN aggressively repurchasing their common stock, which has increased the quality of earnings. • Most recently repurchased $33.7 million or 1.2 million shares of common stock. • To date has repurchased nearly a quarter CS valued at over $500 million; average price of $21.50. • Authorized another $200 million n share repurchase.

A Note on the Income Statement • MYGN faced a 17% SG&A increase over the same quarter last year. • Due primarily to support their 21% increase in revenue and rapid BART test adoption. • Other drivers include increased commissions associated with higher revenue and additional investments in Europe. • Should increase modestly due to rapid increase in sales force, and aggressive launching and marketing of new products.

Margin Analysis • Operates at high margins, and much more efficiently then its competitors. • Margin pressures from growth and expansion, however NI margin should remain unchanged.

Broad Segments • Molecular Diagnostic Testing • Oncology • Women’s Health • Companion Diagnostic Service