Download

1 / 29

290 likes | 307 Views

This text provides an overview of demand and supply in economics, including concepts such as demand curve, supply curve, elasticity, demand shifters, supply shifters, and equilibrium price. It explains the factors that can cause changes in demand and supply, as well as the consequences of price controls.

E N D

Demandthe amount of a good or service that consumers are able and willing to buy at various possible prices.

Quantity Demand • As price goes up quantity demanded goes down. • As price goes down, quantity demanded goes up. The quantity demanded and price move in opposite directions. (Inverse)

What Can Cause Demand to Change? Demand Shifters/Determinants Factors other than price can shift demand. • Changes in income. Normal & Inferior goods • Changes in the number of consumers. • Changes in consumer tastes and preferences. • Changes in consumer expectations. • Changes in the price of substitute goods. • Changes in price of complementary goods.

Elasticity of Demand- A measure of consumer’s sensitivity to a change in price. Inelastic- a product’s price change has little impact on the quantity demanded by consumers.

Factors that influence Elasticity of Demand • Availability of Substitutes. • Price Relative to Income. • Necessities versus luxuries. • Time needed to adjust to a price change

Supply • The amount of good or service that producers are able and willing to supply at various prices.

Law of Supply • As the price rises for a good, the quantity supplied generally rises. • As the price falls, the quantity supplied also falls. Price and quantity supplied move in the same direction

What Can Cause Supply to Change? Supply Shifters/Determinants • Changes in the cost of inputs • Changes in the number of producers. • Changes in conditions due to natural disasters or international events. • Changes in technology. • Changes in producer expectations. • Changes in government policy. • Taxes (decrease) Subsidies (increase)

Elasticity of Supply • Supply Elasticity—is a measure of the way in which the quantity supplied responds to a change in price • Increase in price leads to large increase in output=elastic supply • Increase in price causes a smaller change in output supply is inelastic

Elasticity of Supply • Factors that influence elasticity of supply • Time—longer it takes to make changes to production makes supply inelastic • EXAMPLE: Candy production easy to change just resources land, labor, or capital which means its elastic supply, but it takes longer for a power plant to add recourses needed to expand because of the amount of land, labor, capital it will take

Law of Diminishing Returns • As more units of a factor of production (such as labor) are added to other factors of production (such as equipment), after some point total output continues to increase but at a diminishing rate. • EXAMPLE: Workers with nothing to do

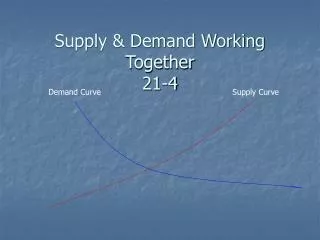

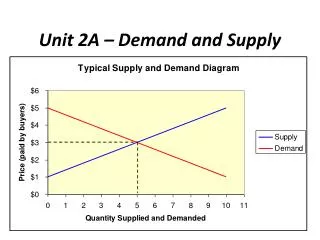

What Happens When Demand Meets Supply? Equilibrium Price This is the price at which the amount producers are willing to supply is equal to the amount consumers are willing to buy.

Prices Serve as Signals What happens when the Price isn’t “Right?” When the price is too low: Shortages- quantity demanded is greater than the quantity supplied. When the price is too high: Surpluses- quantity supplied is greater than quantity demanded.

Price controls should make you think…. Wonderworks in Orlando

Price Controls • Price Ceiling-a legal (gov’t set) maximum price that may be charged for a particular good or service. example: what landlords can charge for rent, the price of gasoline. Effective price ceilings–and resulting shortages–often lead to nonmarket ways of distributing goods and services. The government may resort to: • Rationing- or limiting, items that are in short supply. • Black Market- illegally high prices are charged for items in short supply.

Price Controls-Continued • Price Floor- government set minimum price that can be charged for goods and services. Price floors prevent prices from dropping too low. Example- minimum wage, supporting agricultural prices.