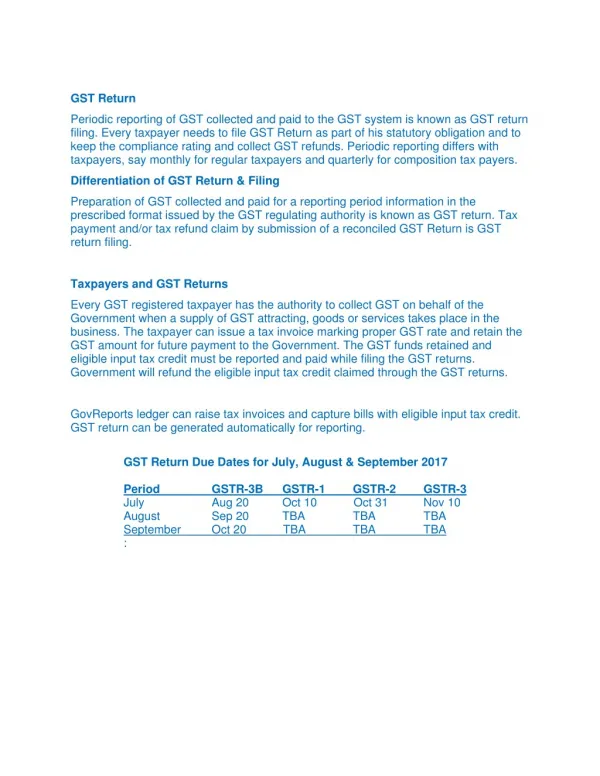

Download

1 / 13

130 likes | 273 Views

GST ISSUES. REIWA Rural Chapter Regional Meeting 31 August 2012 – The Vines Peter Michael. GST ISSUES. GST is a tax on business payable by consumers collected by the seller. Need details and intimate accounting knowledge to advise. GST ISSUES.

E N D

GST ISSUES REIWA Rural Chapter Regional Meeting 31 August 2012 – The Vines Peter Michael

GST ISSUES • GST is a tax on business payable by consumers collected by the seller. • Need details and intimate accounting knowledge to advise.

GST ISSUES • If land is held by an owner who is registered for GST and the land is a business asset, the land will be GST supply and GST is payable. • Conversely, land that is held in a private capacity and not as a business asset is not a GST supply and is outside the system.

GST ISSUES • Various exemptions are applicable for GST purposes where land is supplied. • The main exemption from GST for land sales is the farm land exemption provisions.

GST FARMLAND EXEMPTION • The farm land exemption automatically applies and does not require the express agreement of the parties. • Express agreement of the parties is, however, strongly recommended.

GST farmland exemption • A farming business must have been carried on on the land for a minimum of 5 years preceding the supply. • The farming business does not need to have been carried on by the seller.

GST farmland exemption • The buyer must intend that a farming business will be carried on on the land after the supply. This is why it is important to have a contract clause as set out in the REIWA standard form.

GST farmland exemption • The recipient does not have to be the entity carrying on the farm business. • Farming business does not have to be the sole purpose carried on by the recipient but must be the dominant intention.

GST farmland exemption • It is not necessary that the same type of farming is carried on, e.g., the land could have been used for agriculture or livestock and could be converted to forestry or horticulture.

HOBBY FARM SALES FOR GST PURPOSES • Key issues: • Is the seller registered for GST purposes and is the land a GST supply? • Is the scope of the farming operation sufficient that farm land exemption will apply? • What is the buyer’s intention in regard to the acquisition of the land?

Hobby Farm Sales For GST Purposes • In establishing whether a farm is a farm for exempt purposes, there is a need to examine the intent of the party and is it intended to conduct a profitable farm operation on the land. Evidence of this is in regard budget, bank applications, consultants and other experts assisting in the establishment of the business and to establish that the business is a farm operation.

Hobby Farm SalesFor GST Purposes • Must be an intent to carry on a viable commercial operation. • Business plan.