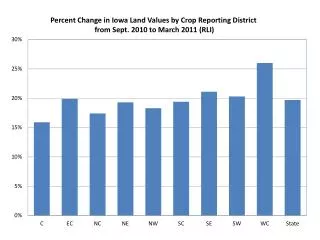

Download

1 / 19

190 likes | 414 Views

THE COST APPROACH TO VALUE. INVOLVES ESTIMATION OF REPRODUCTION OR REPLACEMENT COST OF A PROPERTY LESS ACCRUED DEPRECIATION. BASED ON THE PROPOSITION THAT THE INFORMED PURCHASER WOULD PAY NO MORE THAN THE COST OF PRODUCING A SUBSTITUTE PROPERTY WITH THE SAME UTILITY AS THE SUBJECT PROPERTY.

E N D

THE COST APPROACH TO VALUE • INVOLVES ESTIMATION OF REPRODUCTION OR REPLACEMENT COST OF A PROPERTY LESS ACCRUED DEPRECIATION. • BASED ON THE PROPOSITION THAT THE INFORMED PURCHASER WOULD PAY NO MORE THAN THE COST OF PRODUCING A SUBSTITUTE PROPERTY WITH THE SAME UTILITY AS THE SUBJECT PROPERTY.

RELIABILITY IS AFFECTED BY: 1) REPRODUCTION OR REPLACEMENT COST DATA. 2) ESTIMATE OF ACCRUED DEPRECIATION. • ESPECIALLY APPLICABLE TO: SINGLE FAMILY RESIDENCES SPECIAL USE PROPERTIES SPECIAL PURPOSE PROPERTIES OR WHERE WHEN THE STRUCTURAL IMPROVEMENTS REPRESENT A MAJOR VALUE CONTRIBUTION.

STEPS IN THE COST APPROACH 1) ESTIMATE LAND VALUE AS THOUGH VACANT AND AVAILABLE TO BE PUT TO ITS HIGHEST AND BEST USE. 2) ESTIMATE REPRODUCTION OR REPLACEMENT COST OF STRUCTURES AS OF THE EFFECTIVE DATE OF THE APPRAISAL. 3) ESTIMATE ACCRUED DEPRECIATION. 4) DEDUCT DEPRECIATION FROM REPRODUCTION OR REPLACEMENT COST. 5) ADD DEPRECIATED REPRODUCTION OR REPLACEMENT COST TO THE VALUE OF THE LAND.

CERTAIN DEFINITIONS • BOOK DEPRECIATION • AN ACCOUNTING TERM THAT REFERS TO THE AMOUNT OF CAPITAL RECAPTURE WRITTEN OFF ON AN OWNER’S BOOKS. BOOK DEPRECIATION IS NOT MARKET DERIVED.

ECOMONIC LIFE • THE PERIOD OF TIME OVER WHICH IMPROVEMENTS TO REAL ESTATE CONTRIBUTE TO PROPERTY VALUE. • REMAINING LIFE • THE ESTIMATED PERIOD DURING WHICH IMPROVEMENTS CONTINUE TO CONTRIBUTE TO PROPERTY VALUE.

EFFECTIVE AGE • THE AGE INDICATED BY THE CONDITION OF A STRUCTURE. • CONTRIBUTORY VALUE • THE VALUE THAT IMPROVEMENTS CONTRIBUTE TO THE TOTAL VALUE OF A PROPERTY.

ACCRUED DEPRECIATION • DEPRECIATION - THE LOSS IN PROPERTY VALUE FROM ANY CAUSE. • ACCRUED DEPRECIATION IS THE LOSS IN PROPERTY VALUE FROM: • PHYSICAL DETERIORATION • FUNCTIONAL OBSOLESCENCE • EXTERNAL OBSOLESCENCE • THE DIFFERENCE BETWEEN THE REPRODUCTION COST OR REPLACEMENT COST OF THE IMPROVEMENT AND ITS MARKET VALUE.

REPRODUCTION COST - THE COST OF CONSTRUCTION AT CURRENT PRICES OF AN EXACT DUPLICATE OR REPLICA USING THE SAME MATERIALS, CONSTRUCTION STANDARDS, DESIGN, LAYOUT, AND QUALITY OF WORKMANSHIP. • REPLACEMENT COST - THE COST OF CONSTRUCTION AT CURRENT PRICES OF AN IMPROVEMENT HAVING EQUIVALENT UTILITY TO THE IMPROVEMENT BEING APPRAISED, BUT CONSTRUCTED WITH MODERN MATERIALS AND ACCORDING TO CURRENT STANDARDS, DESIGN, AND LAYOUT.

TYPES OF ACCRUED DEPRECIATION • PHYSICAL DETERIORATION - THE ADVERSE EFFECT ON VALUE CAUSED BY DETERIORATION OR IMPAIRMENT OF CONDITION AS A RESULT OF WEAR AND TEAR AND DISINTEGRATION.

1) CURABLE PHYSICAL DETERIORATION - DEFERRED MAINTENANCE; APPLIES TO ITEMS IN NEED OF REPAIR ON THE EFFECTIVE APPRAISAL DATE. MEASURED AS THE COST OF RESTORING THE ITEM TO A REASONABLELY NEW CONDITION. CONSIDERED CURABLE ONLY IF THE COST OF CORRECTING THE CONDITION WOULD BE OFFSET BY AN EQUAL OR GREATER INCREASE IN VALUE. MUST BE ECONOMICALLY FEASIBLE TO CURE.

2) INCURABLE PHYSICAL DETERIORATION - PHYSICAL DETERIORATION THAT CANNOT BE PRACTICALLY OR ECONOMICALLY CORRECTED AT PRESENT. INCURABLE PHYSICAL DETERIORATION MUST BE BASED ON THE REPRODUCTION OR REPLACEMENT COST OF THE ENTIRE STRUCTURE AFTER THE COST TO CURE CURABLE COMPONENTS HAVE BEEN DEDUCTED. USUALLY CALCULATED USING THE PHYSICAL-LIFE METHOD OR THE ECONOMIC AGE-LIFE METHOD.

AGE-LIFE METHODS • THE PHYSICAL AGE-LIFE METHOD IS THE APPLICATION OF THE RATIO OF ACTUAL AGE TO ESTIMATED TOTAL PHYSICAL LIFE OF THE STRUCTURE. THIS METHOD IS USED TO ESTIMATE PHYSICAL DETERIORATION ONLY. • THE ECONOMIC AGE-LIFE METHOD IS THE APPLICATION OF THE RATIO OF EFFECTIVE ARE TO ESTIMATED ECONOMIC LIFE. THIS METHOD IS TYPICALLY USED TO ESTIMATE THE TOTAL DEPRECIATION, BUT MAY BE USED TO ESTIMATE INCURABLE PHYSICAL DETERIORATION.

OBSOLESCENCE • FUNCTIONAL OBSOLESCENCE - THE ADVERSE EFFECT ON VALUE RESULTING FROM DEFECTS IN DESIGN THAT IMPAIR UTILITY. CAUSED BY CHANGES OVER THE YEARS THAT HAVE MADE SOME ASPECTS OF THE STRUCTURE, MATERIAL, OR DESIGN OBSOLETE.

3) CURABLE FUNCTIONAL OBSOLESCENCE - MUST BE ECONOMICALLY FEASIBLE TO CURE. MAY BE FROM A DEFICIENCY OR AN EXCESS. 4) INCURABLE FUNCTIONAL OBSOLESCENCE - A FUNCTIONAL OBSOLESCENCE NOT PHYSICALLY OR ECONOMICALLY CURABLE. EX. BARN DOORS TOO SMALL FOR MODERN FARM EQUIPMENT.

EXTERNAL OBSOLESCENCE IS THE ADVERSE EFFECT ON VALUE FROM INFLUENCES OUTSIDE THE PROPERTY ITSELF. EFFECTS BOTH LAND AND IMPROVEMENTS. USUALLY INCURABLE ON THE PART OF THE OWNER.

METHODS OF ESTIMATING ACCRUED DEPRECIATION • DIRECT METHODS: 1) BREAK DOWN METHOD - ESTIMATE THE LOSS IN VALUE ATTRIBUTABLE TO EACH OF THE THREE CATEGORIES OF DEPRECIATION - PHYSICAL, FUNCTIONAL, AND EXTERNAL. 2) AGE-LIFE - MEASURES THE RELATIONSHIP BETWEEN EFFECTIVE AGE AND TOTAL LIFE. (EFFECTIVE AGE IS RELATED TO USEFULNESS, CONDITION, AND REMAINING LIFE EXPECTANCY. MAY BE MORE OR LESS THAN CHRONOLOGICAL AGE.) THE AMOUNT OF DEPRECIATION IS A PERCENTAGE OF THE RCN.

INDIRECT METHODS: USE OF COMPARABLE SALES WHERE THE RCN OF THE IMPROVEMENTS AS OF THE EFFECTIVE DATE OF THE APPRAISAL MINUS THE VALUE CONTRIBUTION AS OF THE SAME DATE EQUALS TOTAL ACCRUED DEPRECIATION. LIMITATIONS OF THE INDIRECT METHOD INCLUDE: AN INADEQUATE QUANTITY OF COMPARABLE SALES WITH RESPECT TO IMPROVEMENTS BEING VALUED.

ESTIMATING DEPRECIATION USING MARKET EXTRACTION • FARMLAND WITH IMPROVEMENTS SOLD FOR CASH ON THE OPEN MARKET. THE SALE PRICE IS DEEMED TO BE REPRESENTATIVE OF MARKET VALUE. • SALE PRICE: 240 AC. @ $1,250 / AC = $300,000 LAND VALUE: 240 AC. @ $1,000 / AC = $240,000 INDICATED VALUE OF IMPROVEMENTS $ 60,000 ESTIMATED COST TO REPLACE IMPROVEMENTS $100,000 INDICATED ACCRUED DEPRECIATION OF IMPROVEMENTS $ 40,000 THE INDICATED CONTRIBUTORY VALUE OF THE IMPROVEMENTS IS $60,000 OR 60 PERCENT OF REPLACEMENT COST NEW (RCN) THE INDICATED DEPRECIATION IS 40 PERCENT OF RCN

ESTIMATION OF PHYSICAL DETERIORATION • BARN WITH A REPLACEMENT COST NEW (RCN) OF $43,550. PHYSICAL AGE OF 40 YEARS AND EXPECTED LIFE OF 100 YEARS. • CURABLE PHYSICAL DETERIORATION: NEW ROOF - $3,600 EXTERNAL PAINT - $1,000 -$4,600 • RCN LESS CURABLE PHYSICAL DETERIORATION: $43,550 - $4,600 = $38,950 • INCURABLE PHYSICAL DETERIORATION: 40/100 = .40 .40*$38,950 = $15,580 • TOTAL PHYSICAL DETERIORATION: $4,600 + $15,580 = $20,180 • CONTRIBUTORY VALUE: $43,550 - $4,600 - $15,580 = $23,370