Download

1 / 2

20 likes | 264 Views

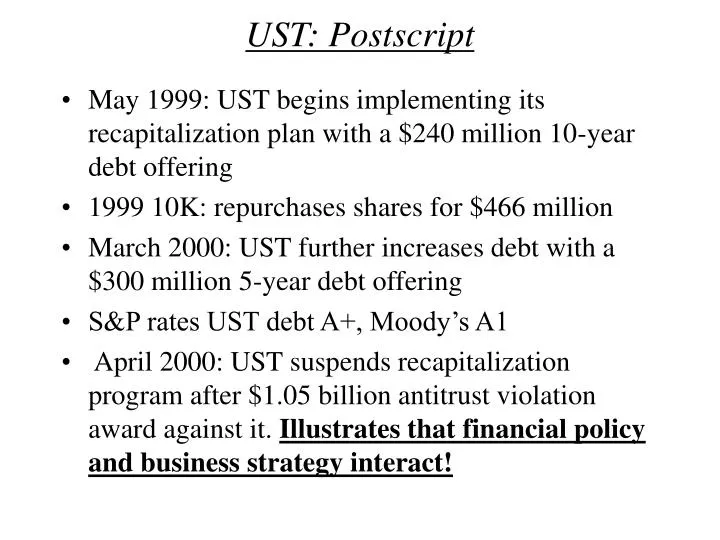

UST: Postscript. May 1999: UST begins implementing its recapitalization plan with a $240 million 10-year debt offering 1999 10K: repurchases shares for $466 million March 2000: UST further increases debt with a $300 million 5-year debt offering S&P rates UST debt A+, Moody’s A1

E N D

UST: Postscript • May 1999: UST begins implementing its recapitalization plan with a $240 million 10-year debt offering • 1999 10K: repurchases shares for $466 million • March 2000: UST further increases debt with a $300 million 5-year debt offering • S&P rates UST debt A+, Moody’s A1 • April 2000: UST suspends recapitalization program after $1.05 billion antitrust violation award against it. Illustrates that financial policy and business strategy interact!

UST: Even cash cows should borrow! • Debt increases shareholder value via corporate interest tax shield • Interest tax shields are limited by: • Firm’s ability to generate sufficient EBIT • Bondholders’ personal tax rates (if > corporate tax rate) • Bad reasons for more debt: higher ROE, EPS (should be discounted at higher equity cost also, so no effect on value (MM)!) • By levering up, UST created value on the right hand side of the balance sheet, but gain from improved capital structure is relatively small