Download

1 / 49

500 likes | 730 Views

Probability. Probability. Probability is a measure of the possibility of an event happening Measure on a scale between zero and one Probability has a substantial role to play in financial analysis as the outcomes of financial decisions are uncertain e.g. Fluctuation in share prices.

E N D

Probability • Probability is a measure of the possibility of an event happening • Measure on a scale between zero and one • Probability has a substantial role to play in financial analysis asthe outcomes of financial decisions are uncertain e.g. Fluctuation in share prices

The classical approach to probability • The range of possible uncertain outcomes is known and equally likely • EXPERIMENT, SAMPLE, EVENT consider the tossing of a fair coin: the range is limited to two the tossing of the coin is the experiment the two possible outcomes refer tothe sample space the outcome whether it is head or tail isthe event

The empirical approach to probability • In finance, we cannot rely on the exactness of a process to determine the probabilities • Consider ‘the return of financial assets’ • The range is unlimited • In such situations the probability of a given outcome Z, P(Z), is

The empirical approach to probability • E.g. Consider a sample of 100 daily movements in a share price. Assume that of the 100 absolute movements, five movements were 0.5 Baht each, 15 were 1 Baht each, 20 were 1.5 Baht each, 30 were 2 Baht each, 20 were 2.5 Baht and 10 were 3 Baht each

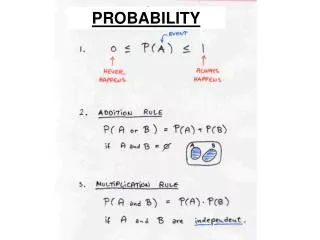

Basic rules of probability • These rules are : • the addition rule concerned with A or B happening • the multiplication rule concerned with A and B occurring • Which of these rules is applicable will depend on whether the combined events are • INDEPENDENT or MUTUALLY EXCLUSIVE ???

Mutually exclusive • Two events cannot occur together Sample space = {1,2,3,4,5,6} A is the event that the face of die shows odd number: A = {1,3,5} B is the event that the face of die is even number: B = {2,4,6} A Λ B = { } = Ø A and B is MUTUALLY EXCLUSIVE

Mutually exclusive B A

The addition rule applied to non-mutually exclusive events • P(A or B) = P(A) + P(B) – P(A and B) • Assume that the FTSE 100 index may rise with a probability of 0.55 and fall with the probability of 0.45. Also assume that a particular time interval the S&P index may rise with a probability of 0.35 and fall with a probability of 0.65. There is also a probability of 0.3 that both indices rise together. What is the probability of wither the FTSE 100 index or the S&P 500 index rising A B

The multiplication rule applied to non-independent events • P(A and B) = P(A) * P(B A) • P(B A) is the conditional probability of B occurring given that A has occurred • Suppose the probability of the recession is 25% and long-term bond yields have an 80% chance of declining during a recession What is the probability that a recession will occur and bond yields will decline?

Bayes’ theorem • Manipulation of the general multiplication rule • The probability of the updated event An can be updated to P(A|B) if Scenario B is known to have occurred by using the following relationships

Bayes’ theorem • Suppose the economy is in an uptrend three out of every four years (75%). Furthermore, when the economy is in an uptrend, the stock market advances 80% of the time. Conversely, the economy declines one out of every four years (25%), and the stock market declines 70% of the time when the economy is in a recession.

Random variable Random Variable • A variable that behave in an uncertain manner • As this behavior is uncertain we can only assign probabilities to the possible values of these variables. • Thus the random variable is defined by its probability distribution and possible outcomes. • Two types of random variable: discrete and continuous

Discrete probability distribution • Variables that have only a finite number of possible outcomes • For example …a six-sided die is thrown Possibilities r=1 1 2 3 4 5 6 Probability thatZ=r 1/61/6 1/6 1/6 1/6 1/6

Discrete probability distribution Probability Distribution ValuesProbability 0 1/4 = .25 1 2/4 = .50 2 1/4 = .25 Event: Toss two coins Count the number of tails T T T T

Continuous probability distribution • Variables that can be subdivided into an infinite number of subunits for measurement • For example …speed, asset returns • Consider: a movement in an asset price from 105 to 109 will give a return of … %

Continuous probability distribution • To overcome this practical problem, we must define our continuous random variable by integrating what is know as a probability density function (pdf)

Expected value of a random discrete variable • Expected value (the mean) • Weighted average of the probability distribution • e.g.: Toss 2 coins, count the number of tails, compute

Expected value of a random discrete variable • Expected value (the mean) • Weight average squared deviation about the mean • e.g. Toss two coins, count number of tails, compute variance

Computing the Mean for Investment Returns Return per $1,000 for two types of investments Investment P(XiYi) Economic condition Dow Jones fund XGrowth Stock Y .2 Recession -$100-$200 .5 Stable Economy + 100+ 50 .3 Expanding Economy + 250+ 350

Computing the Mean for Investment Returns Return per $1,000 for two types of investments Investment P(XiYi) Economic condition Dow Jones fund X Growth Stock Y .2 Recession -$100-$200 .5 Stable Economy + 100+ 50 .3 Expanding Economy + 250+ 350

Probability Distribution Important probability distributions in finance Discrete: • BINOMIAL • POISSON Continuous: • NORMAL • LOG NORMAL

Binomial probability distribution • Only two possible outcomes can be taken on by the variable in a given time period or a given event. e.g.getting head is success while getting tail is failure • For each of a succession of trials the probability of two outcome is constant e.g. Probability of getting a tail is the same each time we toss the coin

Binomial probability distribution • Each binomial trial is identical e.g. 15 tosses of a coin; ten light bulbs taken from a warehouse • Each trial is independent the outcome of one trial does not affect the outcome of the other

Binomial probability distribution Su2 j=2 Su Sud = Sdu j=1 S Sd Sd2 j=0 J = number of success

Binomial probability distribution The probability of achieving each outcome depends on: • the probability of achieving a success • the total number of ways of achieving that outcome e.g. consider the case of j = 1 (Sdu = Sud) • each way has a probability of 0.25 • there are two ways to achieving an outcome

Binomial probability distribution Combination rule or the number of binomial trials

A binomial tree of asset prices • The most common application of the binomial distribution in finance is ‘security price change’ • It is assumed that over the next small interval of time security price will wither rise (‘a success’) or fall (‘a failure’) by a given amount • The binomial distribution is an assumption in some option pricing models

A binomial tree of asset prices 3 stages in developing the expected value of asset price: • create a binomial lattice • determine the probabilities of each outcome • multiply each possible outcome by the appropriate probability and sum the products to arrive at the expected value

A binomial tree of asset prices In each of the time period the asset may rise with probability of 0.5, or it may fall with a probability of 0.5 Su2 Su Sud = Sdu S=50 Sd suppose: u= 1.10, d = 1/1.10 Sd2 T0 T1 T2

A binomial tree of asset prices Su2 (60.50) Su (55) Sud = Sdu(50) S=50 Su (45.45) Sd2 (41.32) T0 T1 T2

A binomial tree of asset prices The expected value is calculated as: (60.50 x 0.25) + (50.0 x 0.50) + (41.32 x 0.25) = 50.46 The variance is (60.50-50.46)2 x 0.25 + (50.0-50.46)2 x 0.50 + (41.32-50.46)2 x 0.25 = 46.18

The Poisson distribution • Discrete events in an interval • The probability of One Success in an interval is stable • The probability of More than One Success in this interval is 0 • e.g. number of customers arriving in 15 minutes • e.g. information which causes market price to move arrive at a rate of 10 pieces per minute

The Poisson distribution ex. Find the probability of 4 customers arriving in 3 minutes when the mean is 3.6. ex. information which causes market price to move arrive at a rate of 10 pieces per minute. Find the probability of only eight pieces of information arriving in the next minute ???

The normal distribution • Most important continuous probability distribution • Bell shaped • Symmetrical • Mean, median and mode are equal f(X) X Mean Median Mode

The normal distribution • Probability is the area under the curve! f(X) X d c

The normal distribution • There are an infinite number of normal distributions • By varying the parameters and µ, we obtain different normal distributions • An infinite number of normal distributions means an infinite number of tables to look up!!!

Standardizing example Standardized Normal Distribution Normal Distribution

Standardized Normal Distribution Normal Distribution

(continued) Cumulative Standardized Normal Distribution Table (Portion) .02 Z .00 .01 .5832 .5000 0.0 .5040 .5080 0.1 .5398 .5438 .5478 0.2 .5793 .5832 .5871 Z = 0.21 0.3 .6179 .6217 .6255

The normal distribution Example: We wish to know the probability of a given asset, which is assumed to have normally distributed returns, providing a return of between 4.9% and 5%. The mean of the return on that asset to date is 4%, and the standard deviation is 1%

The normal distribution Example: The earnings of a company are expected to be $4.00 per share, with a standard deviation of $40. Assuming earnings per share are a continuous random variable that is normally distributed, calculate the probability of actual EPS will be $3.90 or higher.

The normal distribution Example: The earnings of a company are expected to be $4.00 per share, with a standard deviation of $40. Assuming earnings per share are a continuous random variable that is normally distributed, calculate the probability of actual EPS will be between $3.60 and $4.40.

The lognormal distribution • Modern portfolio theory assumes that investment return are normally distributed random variable. Is that true ?

The lognormal distribution • However, this is not true, investment return can only take on values between -100% and % which are not symmetrically distributed, but skewed.

The lognormal distribution • Mathematical trick !!! Distribution of Vt/Vo is Lognormal Distribution of ln(Vt/Vo) is Normal