Download

1 / 11

110 likes | 125 Views

Learn about county revenue sources, property taxes, local sales tax allocation, state and federal funding, and other income streams for efficient financial management.

E N D

County Revenues and Expenditures David M. Lawrence

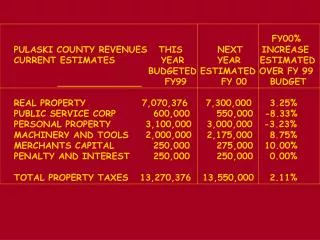

The Property Tax • The General Assembly decides what property may be taxed by counties and cities. • The counties list, value, and discover property. • Counties and cities may collect taxes. • As a practical matter, there is no rate limit on county property taxes.

The Property Tax Cycle • January 1 – The tax lien attaches. • July 1 – The fiscal year begins. • September 1 – Taxes are due. • January 6 – Interest begins to run.

Local Sales Tax - 1 • The 2.5% local sales tax is actually four separate taxes: • A one-percent tax, and • Three one-half percent taxes. • Sales tax collections are allocated thusly: • One percent – to county where goods delivered. • First two half percents – per capita • Last half percent – half of each

Local Sales Tax - 2 • Once allocated to a county, sales tax proceeds are divided between county and city governments either: • On a per capita basis, or • On the basis of each unit’s property tax levy. • Portions of the first two one-half percent taxes are earmarked for school capital outlay

State and Federal Revenues • Counties receive a share of state beer and wine taxes, about $12 to $13 million annually. • Counties receive major amounts of state and federal revenues, especially for human services.

General law taxes Business license taxes Animal taxes 911 charges Rental car license taxes Local act taxes Occupancy taxes Deed transfer taxes Prepared food taxes Motor vehicle taxes Other Local Taxes

Other Revenue Sources • User charges, such as utilities. The county may earn a profit. • Regulatory fees, such as inspection fees. The county may cover costs. • Investment income.