Download

1 / 13

130 likes | 304 Views

Test Results from Quiz #1 (Scored out of 15 with 5 bonus marks). Test Results from Quiz #2 (Group Test Scored out of 20). Test Results from Quiz #3 (Individual Test Scored out of 6). Test # 3 Review Note : Bring a calculator next time .

E N D

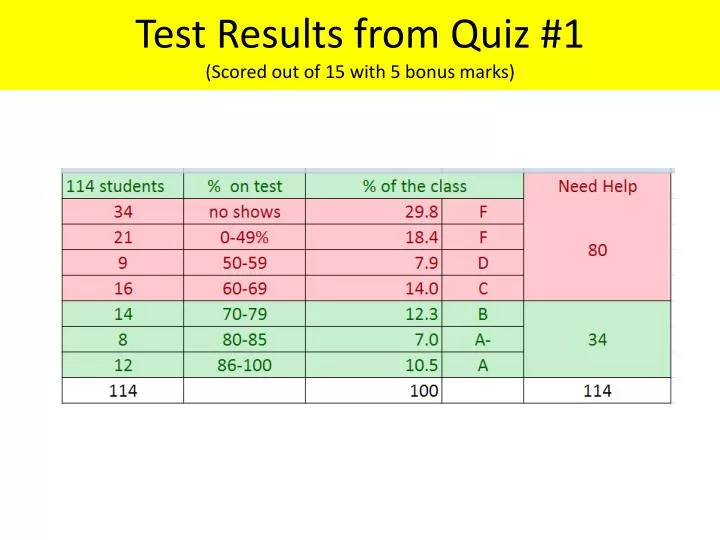

Test Results from Quiz #1(Scored out of 15 with 5 bonus marks)

Test #3 Review Note: Bring a calculator next time. Many students use percent signs when we were working with ratios. I still awarded a correct answer if the number was correct, but technically, the answer was wrong. The difference between a percent and a ratio is: Ratios are another form of a fraction, for instance: I have 1 apple to 2 oranges, which can be expressed as 1:2 (ratio) or 1/2 (fraction) which basically mean the same thing. Percent (%) is when you actually DIVIDE and multiply that decimal by 100%. For instance, with the apple and oranges, 1/2 becomes converts to 0.5 0.5 x 100= 50%

Question #1 DEBT RATIO was marked correct for .51 or .33. Explanation. The formula provided was for debt to net worth and the answer is .51 In personal finances the commonly used formula is debt to asset. Some students gave this calculation. If this calculation is asked for again, it will be the debt to asset ratio and the formula will ask for it. Question #2 asked the LIQUIDITY RATIO = liquid assets (bank account 8,000) / monthly expenses (fixed 3,065) not variable. Remember that liquidity ratio does not include variable expenses, because you could quickly reduce those expenses if you had to.

Review (continued) Question 3 DEBT PAYMENT RATIO was marked correct if it was either 25%, 37% or 50%. The best answer was 51%. Depending on whether you used one, two or three of the credit payments, you will have come up with a different answer. Mortgage; Car Loan; Credit Card. The objective here is to isolate your credit payments, those payments which if not honored will negatively affect your credit rating and increase your cost of borrowing in the future.

Review (continued) Question 4 SAVINGS RATIO was straight forward. Remember the difference between gross income (before your taxes are deducted) and net income (after taxes are deducted). Money lenders will use your gross (before tax) to evaluate your savings ratio because there are many tax implications that can reduce your tax, if you invest and save your money based on government tax incentives.

Review (continued) Question #5. REMEMBER TO READ EVERY QUESTION CAREFULLY. Many students gave excellent answers. Some students did not read the question carefully enough. In this example, there was money left over at the end of the month. A Surplus. Some students answered as if there was a shortage. Some of the answers included reducing expenses, such as not spending on beauty products or searching for less expensive car insurance. If we did not have enough money to pay our bills, this would have been correct, but the question was an effort to have you tell me how you could invest the extra and make it grow.

Review (continued) Some of the answers included: a) Invest the surplus in stocks, bonds, property, pay more on my house mortgage. b) Spend more on discretionary goods like jewelry, vacations, cars or food. Some of the examples I disagreed with but I still gave the student the mark, if it appeared that there was an effort to communicate an honest answer. An example of an answer that I did not like, but still got the mark, is “invest in insurance”. Personal example of life insurance. An example I liked was, “buy property and rent it” however, keep in mind that you will need to know something about property management.

Review (continued) Debt Ratio is different from Debt to Net Worth Ratio

Debt Ratio, is sometimes referred to as Debt to Asset Ratio and is the measure most commonly used by individuals to see how much they own as compared to how much they are borrowing.

Debt Ratio = long term liabilities/total assets(commonly used for personal finances)This will be test question Debt ratio compares debt to assets. A lower debt ratio is better to have. The smaller the liability over the asset, the more you own. More is better. This ratio tells us how heavily the individual is financed.

Debt to Net Worth Ratio = Total Liabilities/Net Worth (commonly used for business) You will NOT be tested on this ratio Why is it important to know the difference? This ratio is a leverage measure that tells you how much of the business assets, including share holders equity is leveraged against long term debt. It does not consider current liabilities. The debt/equity ratio is more conservative and useful to help when considering the risk involved when investing money in a company. Perception of risk is increased. The debt/asset ratio is like a snapshot of an individual. An individual person does not risk their equity (assets) in order to earn money. Rather, the debt to asset ratio is like a picture of your financial position at this moment in time.