Download

1 / 3

30 likes | 293 Views

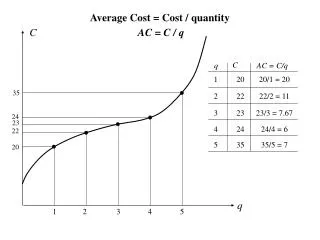

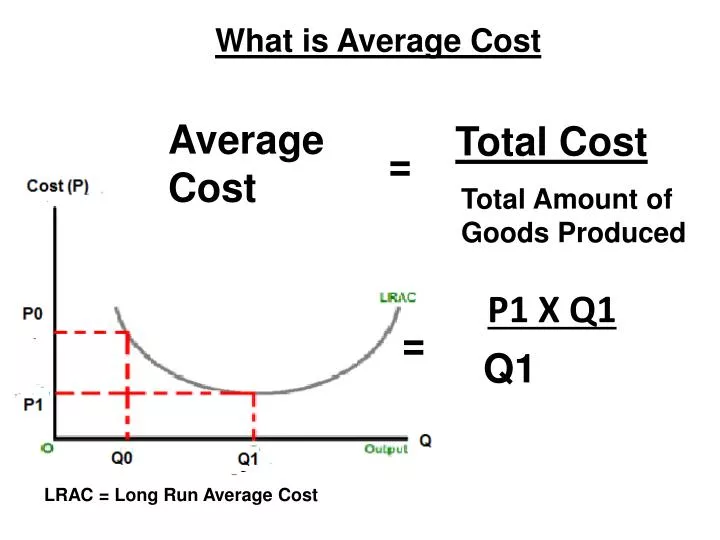

What is Average Cost. Average Cost. Total Cost. =. Total Amount of Goods Produced. P1 X Q1. =. Q1. LRAC = Long Run Average Cost. Economies of Scale.

E N D

What is Average Cost Average Cost Total Cost = Total Amount of Goods Produced P1 X Q1 = Q1 LRAC = Long Run Average Cost

Economies of Scale As the producer increases his output, it gives rise to lower and lower cost until it reaches a scale of Q1 and and achieves the lowest average cost of production P1. The idea of lowering average cost (P) as output increases is called economies of scale. Most monopolist enjoy huge economies of scale where the cost (P) is falling over a wide range of output.

Economies of Scale (Internal) What is it that allow firms to lower their cost (P) while the increase their output? It is due to the following: • Technical Economies of Scale – The use of better technology or machinery to produce. • Managerial Economies of Scale – The use of professional managers like accountants or human resource manager whose expertise can be shared by a few departments in a company. • Buying in Bulk – By buying resources in big quantities, producers get discounts than if the bought is small quantities. • Financial Economies of Scale – Bankers and financiers will feel more confident lending to firms who are big and have assests that a small company.