Download

1 / 0

0 likes | 168 Views

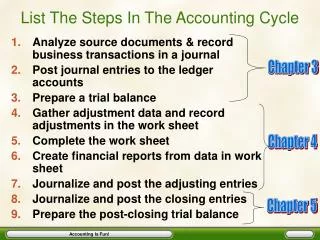

Completing the Accounting Cycle for a Merchandising Corporation & Accounting for Publicly Held Corporations. Chapter 20 & 21. Steps for Closing the Ledger. Close temporary accounts with credit balances to Income Summary Close temporary accounts with debit balances to Income Summary

E N D