Download

1 / 2

20 likes | 176 Views

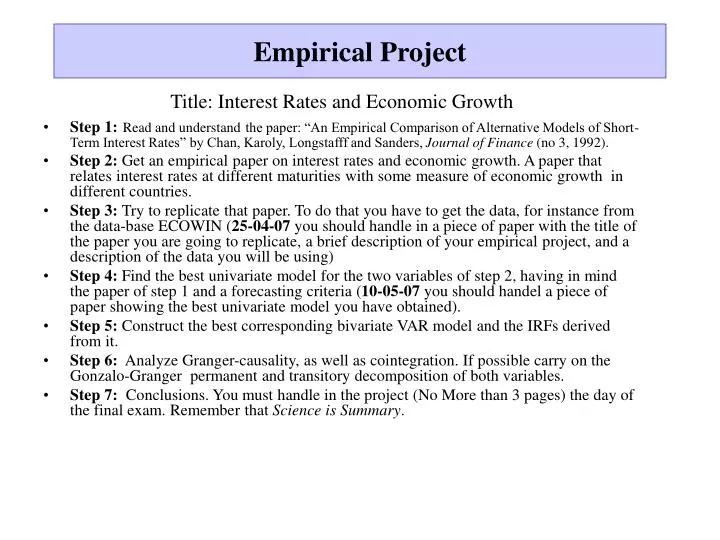

Empirical Project. Title: Interest Rates and Economic Growth Step 1: Read and understand the paper: “An Empirical Comparison of Alternative Models of Short-Term Interest Rates” by Chan, Karoly, Longstafff and Sanders, Journal of Finance (no 3, 1992).

E N D

Empirical Project Title: Interest Rates and Economic Growth • Step 1:Read and understandthe paper: “An Empirical Comparison of Alternative Models of Short-Term Interest Rates” by Chan, Karoly, Longstafff and Sanders, Journal of Finance (no 3, 1992). • Step 2: Get an empirical paper on interest rates and economic growth. A paper that relates interest rates at different maturities with some measure of economic growth in different countries. • Step 3: Try to replicate that paper. To do that you have to get the data, for instance from the data-base ECOWIN (25-04-07 you should handle in a piece of paper with the title of the paper you are going to replicate, a brief description of your empirical project, and a description of the data you will be using) • Step 4: Find the best univariate model for the two variables of step 2, having in mind the paper of step 1 and a forecasting criteria (10-05-07 you should handel a piece of paper showing the best univariate model you have obtained). • Step 5: Construct the best corresponding bivariate VAR model and the IRFs derived from it. • Step 6: Analyze Granger-causality, as well as cointegration. If possible carry on the Gonzalo-Granger permanent and transitory decomposition of both variables. • Step 7: Conclusions. You must handle in the project (No More than 3 pages) the day of the final exam. Remember that Science is Summary.

Some Hints • Use JSTOR • Use the NBER working papers data-base • Use Google and Google-Scholar • See the book by Kerry Patterson (200): “An introduction to Applied Econometrics, a time series approach”