Download

1 / 41

410 likes | 871 Views

What is vertical integration?. Vertical (or horizontal) integration means that the assets that were previously held by two firms are combined into a single firm.The result is either joint ownership or the sale of one firm's assets to the other.. Market Imperfections. Upstream and downstream firmDownstream firmMonopolist with no costsSets price to its market (mark-up over marginal costs)Upstream firmMonopolistSets input price to downstream firm anticipating impact on demand .

E N D

1. Vertical integration When does outsourcing/ownership matter?

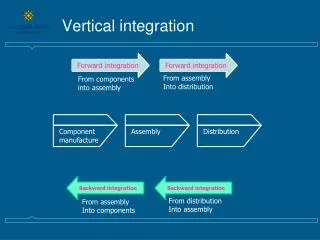

2. What is vertical integration? Vertical (or horizontal) integration means that the assets that were previously held by two firms are combined into a single firm.

The result is either joint ownership or the sale of one firm�s assets to the other.

3. Market Imperfections Upstream and downstream firm

Downstream firm

Monopolist with no costs

Sets price to its market (mark-up over marginal costs)

Upstream firm

Monopolist

Sets input price to downstream firm anticipating impact on demand

4. Vertical Integration Suppose upstream and downstream firms are commonly owned

Best internal transfer price is based on upstream marginal cost, c.

Market price set so that MR = c.

Maximises joint profits

5. Impact on Profits

6. Double Marginalisation With outsourcing

Both firms charge a mark-up

Higher prices, low overall profits, lower consumer welfare (not very competitive if there is another vertical chain)

Solved by:

Vertical integration

Two-part tariffs

More downstream or upstream competition

7. Can vertical integration matter? The Coase Theorem tells us that asset ownership does not matter for efficiency.

Assumes complete contracting

When contracts are incomplete there exist residual rights of control (unspecified actions). According to Grossman & Hart:

�To the extent that there are benefits of control, there will always be potential costs associated with removing control (i.e., ownership) from those who manage productive activities.�

8. GM-Fisher Body 1920s: General Motors purchased car bodies from independent firm (Fisher Body)

Technology change: wooden to metal

GM built a new assembly plant that required reliable supply

wanted Fisher Body to build a new car body plant next to it

no need for shipping docks etc.

9. Fisher Refused Fisher Body refused to make this investment.

Feared that a plant so closely tailored to GM�s needs would be vulnerable to GM�s demands (hold-up)

Eventually resolved this issue by vertical integration -- could not find a contractual solution

10. Merger Benefits & Costs Benefits to GM:

Could make more demands of Fisher Body

More investment or extra supply

Costs to GM:

Diminished managerial incentives

If costs are lowered in the body plant, GM is better able to appropriate these at expense of managers.

Harder to keep those costs down.

11. Bottling Pepsi PepsiCo has two types of bottlers:

Independent: owns assets of bottling operation and exclusive rights to franchise territory. Can determine how these are used - when to restock stores etc.

Company owned: decisions can be made higher up; Pepsi can choose to delegate local marketing to its subsiduary

12. Pepsi�s Control Pepsi cannot control how an independent bottler operates in a territory

If it wants a national marketing strategy (such as the Pepsi Challenge), it can�t compel the bottler to cooperate

By acquiring a bottler, Pepsi has ultimate control.

If the subsidiary managers refused to participate in the national campaign, they could be sacked and replaced.

13. Motivating Example Again Service requires a truck (the asset) for production

Also, enhancing value are:

a shipper, S (who wants to ship goods)

there are also other shippers except that they have goods to ship that are $100 less in value created

a trucker, T (does this): can take care or no care in maintaining truck;

there are many truckers who can take no care but this particular trucker is the only one that can take care

Effort in care is relationship-specific and is now assumed to be non-contractible

Also assume that care is a skill that is developed (through habits etc.). Therefore, it becomes embedded in the trucker�s human capital.

14. Effort and Value Benefit from extended truck life

No Care: truck�s value is $50

Care: truck�s value is $200

Trucker�s effort cost of care

Minimal care: cost of $0

High care: cost of $100

Marginal Benefit = $150 > $100 = Marginal Cost

Efficient to take care

What happens under different ownership structures for the asset?

15. Non-contractible Investment Suppose bargaining took place after effort choice is made

There are four cases to evaluate.

Minimal care and alternative shipper

Minimal care and S

High care and alternative shipper

High care and S

S is no longer essential and so their added value is less than the T if they do not own the asset.

16. Will trucker take care?

17. Incentives and Ownership Trucker can be easily replaced if does not take care. However, under BI and 3rd party ownership (vertical separation), does not expect to earn enough to cover costs of $100.

Will take care under FI: needs to have control rights (i.e., right to exclude use of asset) in order to gain sufficient surplus ex post.

That is, under FI, by taking care, T gets $50 (=$150-$100) but only $25 if it does not take care.

Under Cooperative, taking care gives T $0 but not taking care gives them $25.

General principle: give control rights to agents making important investments.

18. Efficient Integration Level As they encourage the trucker to take care, forward integration is the only efficient organisational form

Do we expect asset ownership to track efficiency?

19. Shipper Interests Shipper might choose to have a back haul. A back haul adds value of $100 (independent of level of care).

Suppose that trucker � if they own the truck � can find alternative customers for the back haul. If expend cost of $10 will find alternative customer adding value of $50.

20. Forward Integration Shipper�s added value ex post:

$250 if trucker searches for alternative customer

$300 if trucker does not search

Trucker�s added value ex post

$300 regardless of whether searches

Searching improves trucker�s expected surplus from $150 to $175; therefore, worth the $10 expense.

If search very costly, BI may become efficient again.

21. Optimal Firm Boundaries Ownership provides maximal incentives to take non-contractible actions

Optimal firm boundary depends upon:

whose actions are hardest to encourage

whose actions are most important for value

Never vest ownership with someone who does not provide a non-contractible action (I.e., 3rd party)

22. What Happens in Trucking? Suppose that you could put on-board computers on truckers to monitor drivers.

Theory: easier to monitor driver�s care and reflect it in explicit performance payments or fines � therefore, less need for trucker ownership.

Baker & Hubbard (2000): use of OBCs has increased non-trucker ownership especially on routes that may be more subject to trucker rent seeking.

23. Shipper vs. Carrier ownership What determines whether shippers use internal (captive) fleets or for-hire carriers for a haul?

Determines who owns control rights associated with dispatch (truck scheduling)

Shippers use internal fleets when want high service levels from truck drivers

Truck utilisation higher in for-hire fleets � ability to line up a sequence of hauls for a truck � tight coordination (requires dispatcher effort)

Need for flexibility conflicts with search for back hauls

Harder to motivate truck drivers when looking for high service levels.

Empirically: OBCs lead to more shipper ownership

24. Case: Insurance Industry Insurance industries

In-house sales force: whole life

Independent brokers: fire and casualty

Choice determines ownership of client list

25. Effect of ownership Agent owns list

cannot be solicited without permission

agent looks for clients most likely to renew

motivate agents by using renewal commission

agent can hold-up company; threaten not to introduce new products to clients

Company owns list

company can hold-up agent; threaten to increase premiums that reduce renewal commission

26. Applying Grossman & Hart Choice between independent and in-house agents should turn on relative importance of investments in developing long-term clients by the agent and list-building activities of the insurance firm

Whole life: customer less likely to switch so searching for long-term customers less important -- in-house

Fire & casualty: searching for long-term customers is important -- independent

27. Dynamic Issues How does outsourcing and integration performance change over time?

28. T5 at Heathrow Project management handled internally

Contractors on cost-plus contracts (not fixed price as is usually the case)

British Airports Authority wanted to keep options open to change design specifications throughout the life of the project

Happy to engage in on-going managerial attention

29. Fixed vs Cost Plus Fixed contracts

Costs aren�t passed through

High powered incentives to keep costs down

Anticipate cost savings that might be achieved when tendering

But contracts incomplete: so subject to renegotiation (also anticipated in tender)

Cost plus contracts

Costs are passed through

Low powered incentives

No difficult renegotiations � easier to change designs during project

For complex projects that require lots of coordination, may be better to use cost plus contracts

30. Car Manufacturing Varied patterns of outsourcing

Some companies integrated (GM)

Some outsource almost everything (Volvo)

Novak-Stern case studies suggest that...

External sourcing allows firms to access state-of-the-art technology but leaves them open to hold-up and low effort supply after the initial terms of the contract are satisfied

Internal development is associated with inferior technology development and high costs for an initial model-year, but there are much greater opportunities for improvements over time

31. Performance Over time

32. Empirical Findings

33. Summary No black and white choice in outsourcing

Capabilities can improve over time

Ability to coordinate internal or external teams

Ability to improve internal performance

Handling contractual disputes

No �one size fits all�

Complexity � design and parts

34. Principles of Efficient Ownership Simple example

Asset: luxury yacht

Service: gourmet seafare

Workers: chef and skipper

Customer: tycoon

Value created

Tycoon value = $240 (no other customers)

Substitutes for skipper�s skills (no added value)

Chef: asset-specific action (no other yachts) for cost of $100; necessary to provide service for Tycoon

Time-line

Date 0: chef chooses whether to take action

Date 1: negotiate over division of $240

35. Ownership Outcomes

36. Skipper Value Now suppose, skipper has a non-contractible (date 0) action

for cost of $100 can increase value of service to tycoon by another $240 (total now $480)

for example, increases knowledge of local islands

37. Ownership Outcomes

38. Complementary Assets Now suppose there are other customers who can use the yacht

But tycoon can choose a non-contractible action (e.g., plan entertainment schedule for the year). Gives additional value of $240.

Yacht can be split in two: galley and hull

39. Divided Ownership Is it ever optimal for chef to own galley and skipper to own hull?

Division of value is: chef ($320), skipper ($320) and tycoon ($240/3)

Tycoon has to reach agreement with both while skipper and chef only require their joint agreement

Better to give entire yacht to skipper or chef. Tycoon�s incentive rises ($240/2)

40. Principles Never give ownership to dispensable individuals

Give ownership to indispensable agents (even though may not make an investment)

Vest ownership of complementary assets with a single individual

41. Qualification Does asset ownership really improve incentives for specific investments?

Those investments create value

But may reduce the asset�s value outside of the relationship: it is specialised to the other agent

Without ownership, do not care about this reduction

Hence, it is possible that incentives could be reduced by ownership

42. Summary Value of ownership

Increased bargaining position (added value)

Incentives to take non-contractible actions

Ownership improves this by allowing agent to capture a greater share of the rewards

But diminishes the incentives of non-owners

Who should own an asset?

Agents taking non-contractible actions

Important agents