Download

1 / 11

250 likes | 732 Views

Schools of Economic Thought. Chapter 1. Introduction. The word "economics" is derived from oikonomikos , which means skilled in household management. Why? Modern economic thought emerged in the 17th and 18th centuries as the western world began its transformation from

E N D

Schools of Economic Thought Chapter 1

Introduction • The word "economics" is derived from oikonomikos, which means skilled in household management. • Why? • Modern economic thought emerged in the 17th and 18th centuries as the western world began its transformation from a farming to an industrial society.

Introduction Theories try to answer basic Economic Questions • How do we decide what to produce with our limited resources? • How do we decide who gets goods & services? • How are we going to produce those goods & services?

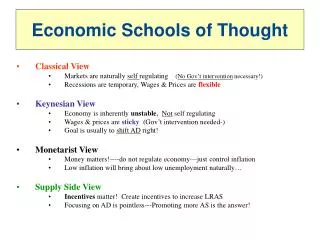

Mercantalism • Merchants and Statesmen • 16th and 17th centuries. • Mercantilists believed that a nation's wealth came from its accumulation of gold and silver. • High interest in exportation of goods • Importation restricted with high tariffs = Protectionism • Brought politics and economics together

Physiocrats • 18th century French philosophers • Idea of the economy as a circular flow of income and output. • They opposed the Mercantilist policy of promoting exportation • Believed agriculture was the sole source of wealth in an economy. • Physiocrats advocated a policy of laissez- faire, which called for minimal government interference in the economy.

Classical • Began with the publication in 1776 of Adam Smith's The Wealth of Nations. • Identified land, labor, and capital as the three factors of production and the major contributors to a nation's wealth • Ideal economy is a self-regulating market system that automatically satisfies the economic needs of the populace. • "invisible hand" that leads all individuals

David Ricardo- Classical • focused on the distribution of income among landowners, workers, and capitalists. • Conflict between landowners and labor and capital. (Have vs. Have-Nots) • Quickly growing population makes increased competition for jobs, pushes wages down

Thomas Malthus- Classical • Diminishing returns explain low living standards • Population increases, outstripping the production of food. • A rapidly growing population against a limited amount of land meant diminishing returns to labor. • The result, he claimed, was chronically low wages, which prevented the standard of living for most of the population from rising above the subsistence level.

Keynesian School • John Maybard Keynes • 1930s, reaction to great depression • Theory: People/Business Owners tend to save too much causing unemployment • Unemployment = poverty = low standard of living • Spending = job creation = employment = increase in personal wealth = increase personal spending = economic growth!! • Insisted that direct government intervention was necessary to increase total spending.

Summary • Economic theories are constantly changing. • Monetarism (value of $ predicts inflation) • Rational Expectations Theory (limited government intervention- people predict government actions minimizing affects)) • Supply-Side Economics (incentives to save & invest to create economic growth) • All theories created to answer the 3 basic Economics questions

Question • Why do you think so many people have such differing views on how to handle economic problems? • Personal socio-economic standing • Political Preferences • Personal Beliefs • Government