Download

1 / 9

0 likes | 8 Views

A term life insurance plan with a critical illness rider offers enhanced financial security by combining life coverage with protection against severe health conditions. This rider provides a lump sum if you're diagnosed with a covered critical illness, ensuring funds for medical bills or income replacement during recovery. It's an effective strategy for those looking to safeguard both their family's financial future and their own health expenses, making it a versatile and valuable choice in long-term planning.

E N D

Introduction Life Insurance is among the most important coverages anyone would need to secure the future of their family's financial stability. Among the wide array of options for Life Insurance, Term Life Insurance Policies are very popular, being relatively affordable and simple. However, few people are aware that an add-on referred to as a critical illness rider can make a Term Life Insurance plan much more comprehensive. One great reason to include a critical illness rider with your Term Life Insurance is if you are diagnosed with a serious condition such as cancer, heart disease, or stroke. The following are reasons why combining Term Life Insurance with a critical illness rider is a smart move, how it works, and how to invest in a plan that is right for you.

Understanding Term Life Insurance with a Critical Illness Rider Term Life Insurance is a type of coverage in effect for a specific period, such as 10, 20, or 30 years. The death benefit will be provided to the policy's beneficiaries if the insured person dies during this term. Therefore, Term Life Insurance would be the best option for those who want to protect their family's financial future for a certain period of time, especially when large obligations are involved, like a mortgage or a child's education. Term Life Insurance does not cover hospital expenses or loss of income in case the policyholder contracts any serious illness, though. Again, this rider on critical illness is where that comes in. It is a rider that can be attached to a Term Life Insurance plan, meaning there is a lump sum given to the insured should a covered critical illness arise, such as cancer. A payout can be utilized to pay for medical care, lost income compensation, or any other thing the policyholder determines. In many aspects, adding a critical illness rider to term life investments transforms these types of insurance into a financial safety net covering not just death but serious illness.

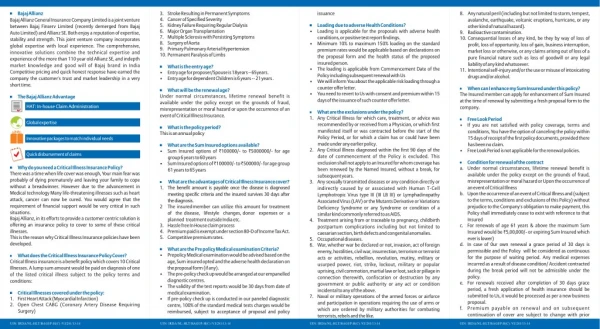

How Does a Critical Illness Rider Work? If you add a critical illness rider to your Term Life Insurance Policy, you are extending coverage that covers specified serious illnesses. In the event of being diagnosed with one of the diseases under the coverage, the policyholder receives a lump-sum payout. It may be used to pay for treatment, take care of your family, or allow you to take some time off from work. For example, suppose that, under a Term Life Insurance, the policyholder has a $500,000 death benefit with an additional critical illness rider. When they eventually come to be diagnosed with some type of cancer, the money would come forth from that rider as a sum amount commonly predetermined at the inception of the insurance policy. The remaining part of the death benefit on the term life policy would be in full force effect as specified under the insurance policy. Every insurance company also indicates which diseases are included, so reading the fine print or getting Term Life Insurance Quotes would be helpful in detailing the critical illness rider. Covered illnesses include cancer, heart attack, stroke, organ failure, and major surgeries.

Benefits of Adding a Critical Illness Rider to Your Term Life Insurance Plan Adding a critical illness rider to your Term Life Insurance policy provides several key advantages: • Financial Protection During Illness: If you’re diagnosed with a serious illness, a critical illness rider ensures you receive funds to cover unexpected costs, allowing you to focus on recovery rather than finances. • Income Replacement: Many critical illnesses can limit your ability to work, resulting in a loss of income. The lump-sum payout from the rider can act as a temporary income replacement, helping you and your family maintain financial stability. • Tax-Free Benefits: Just like Term Life Insurance Policies, the payout from a critical illness rider is typically tax-free, ensuring you maximize the amount received during a challenging time. • Affordable Addition: Adding a rider to your Term Life Insurance plan is often more cost-effective than buying a critical illness policy. This makes it an affordable way to increase your Term Life Insurance Investments without a significant increase in premiums. • Peace of Mind: Knowing you’re covered for both death and critical illness provides peace of mind. A critical illness rider complements the security provided by Term Life Insurance, offering more robust protection for you and your loved ones.

How to Buy Term Life Insurance with a Critical Illness Rider • Compare Term Life Insurance Quotes: Start by comparing to buy Term Life Insurance Online from different providers. Many insurers allow you to customize quotes online, adding riders such as critical illness, so you can see how each option affects the premium. Compare the benefits, premium costs, and the specific illnesses covered by each insurer to find the best match for your needs. • Choose an Adequate Coverage Amount: Decide how much coverage you need for both the Term Life Insurance and the critical illness rider. Your Term Life Insurance policy should be sufficient to cover major obligations and provide for your loved ones, while the critical illness rider should cover potential treatment costs and a buffer for income loss. • Understand the Terms and Conditions: Not all policies and riders are created equal. Carefully read the terms and conditions for each critical illness rider, noting which illnesses are covered, any exclusions, and how the payout is structured. This is especially important, as some policies have waiting periods or exclusions on pre-existing conditions. • Consider the Length of the Term: When choosing your term length, think about your future needs. A 20- or 30-year term may be more suitable if you're looking for long-term security, especially if you're planning to cover mortgage payments or other significant obligations. • Assess Affordability: While the critical illness rider adds valuable protection, it also increases the premium. Assess your budget to ensure the premium is affordable over the policy's term. Remember that the investment in a critical illness rider can save you financially if the unexpected happens.

Real-Life Scenarios Where a Critical Illness Rider Makes a Difference Assuming two people have Term Life Insurance Policies, but only one has a critical illness rider: for example, Person A is diagnosed with heart disease and therefore can't pay the medical costs and related living expenses to care for himself during recovery, but Person B chose a critical illness rider and received a lump-sum payout in case he needs treatment and lost income to ensure stability financially during recovery. Such scenarios depict how a critical illness rider can be pretty the deal-maker in maintaining financial security at critical times. Many have found that this rider becomes a lifeline, saving both health and wealth.

Is a Critical Illness Rider Right for You? If you're considering Term Life Insurance Investments, the critical illness rider is worth exploring. Ask yourself a few key questions: • Do you have a family history of specific critical illnesses? • Do you have financial obligations that would be challenging to meet if you became ill? • Would the added premium fit within your budget? If you agree with these questions, you might require a critical illness rider as an add-on option for your Term Life Insurance. It's not only a way to improve coverage in Life Insurance but will also help ensure financial safety in case of an illness, which is usually unaddressed in standard planning for Life Insurance.

Final Thoughts Adding a critical illness rider to the Term Life Insurance coverage made sense since it could elevate insurance from a mere death benefit to a much stronger safety net. A rider for a critical illness gives you a means of supporting unexpected costs and loss in income during severe illnesses- a thing that offers peace and practical help at a much-needed time. An excellent rider with Term Life Insurance investment comes before a discussion on online purchases or a comparative discussion with the advisor for Term Life Insurance.