Download

1 / 10

0 likes | 17 Views

The two big types of Disability Insurance are short- and Long Term Disability Insurance. Both offer important protection of income, but both are very different in terms of duration, amount of benefit, and even the process of obtaining a quote or buying a policy online. Here's what you need to know about each type and how to choose the right coverage for your needs.

E N D

Understanding the Differences Between Short-Term And Long-Term Disability Insurance What You Need to Know

Introduction As far as replacing your lost income in case you become disabled, it is important to understand all your insurance options. Disability Insurance can provide you peace of mind and financial stability when an illness or injury prevents you from working. The two big types of Disability Insurance are short- and Long Term Disability Insurance. Both offer important protection of income, but both are very different in terms of duration, amount of benefit, and even the process of obtaining a quote or buying a policy online. Here's what you need to know about each type and how to choose the right coverage for your needs.

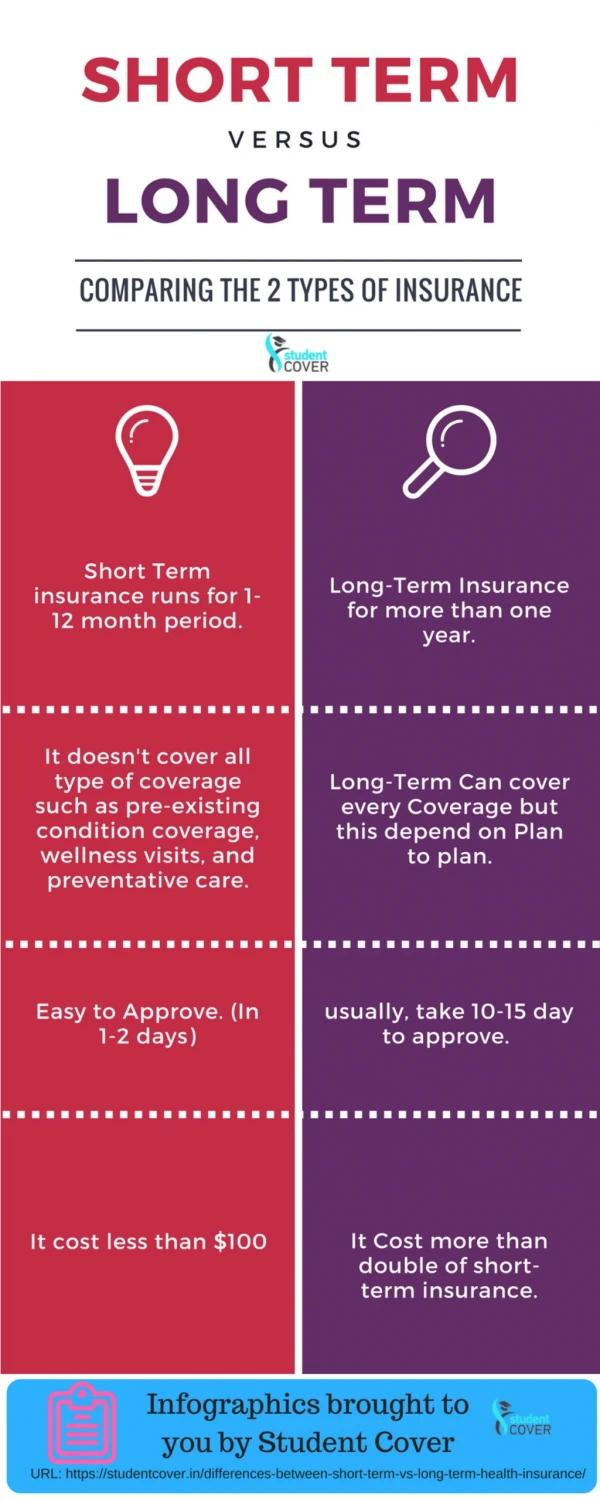

What is Short Term Disability Insurance? Short Term Disability Insurance may replace part of your income for a short period of time, usually weeks to months. It's commonly used to insure for illnesses or injuries that disable a person from working temporarily, with financial stability provided by this insurance product and without a long-term commitment.

STD Coverage Details: • Duration: Benefits usually last between 3 to 6 months, though some policies can extend up to a year. • Benefit Amount: Typically, STD policies cover about 40-70% of your pre-disability earnings. • Waiting Period: The elimination period—the time you must wait before benefits begin—is generally short, ranging from 0 to 14 days. • STD policies can be purchased through employers or unions, or one can purchase a policy directly from an insurer. Many Canadians buy Disability Insurance Policy Online for convenience and to compare quotes on Disability Insurance easily.

What is Long Term Disability Insurance? • Long Term Disability Insurance gives long-term coverage, generally designed to offer some economic security in the event that, due to disability, a person cannot work for several months or even years. LTD is important for serious health problems that may lead to substantial loss of earned income over a long period.

LTD Coverage Details: • Duration: Benefits can last from a few years up to retirement age, depending on the policy terms. • Benefit Amount: LTD policies typically replace about 50-70% of your salary. • Waiting Period: The elimination period for LTD benefits is longer, often ranging from 90 days to several months. • LTD insurance is a very critical part of your financial planning strategy, especially if you have dependents or major money-related obligations resting on you. Much like STD, Long Term Disability Insurance Quotes can be got online to make comparisons between different policies and providers.

Key Differences Between STD and LTD Insurance • Duration of Benefits: The most apparent difference is the benefit duration. STD is suitable for short-term financial relief, whereas LTD is designed for long-term financial security. • Cost: Generally, LTD insurance is more expensive than STD insurance due to the extended coverage period and the higher likelihood of a claim being filed. • Waiting Period: STD insurance typically has a shorter waiting period compared to LTD, reflecting the urgency of financial needs for short-term disabilities.

How to Choose the Right Disability Insurance • Assess Your Financial Situation: Consider your current financial obligations—like mortgages, loans, and family needs—which will guide whether short-term or long-term coverage is more appropriate. • Understand Your Employment Benefits: Check if your employer provides Disability Insurance and the extent of that coverage. This will help you determine if you need additional personal coverage. • Compare Policies: Use online tools to compare Disability Insurance Quotes and policies. Many websites provide detailed comparisons and user-friendly interfaces for purchasing Disability Insurance Policies Online. • Consult with Professionals: Insurance brokers or financial advisors can provide personalized advice based on your specific circumstances and needs.

Summary Disability Insurance—both short-term and long-term—is very important in Canada for protecting your earned income. While STD offers rapid, short-term support in financial terms, LTD has importance attached to shielding a person from monetary loss over a more extended period, particularly against severe illnesses or injuries. Knowing these differences and assessing your needs accordingly will thus help you to make an informed decision about buying Disability Insurance. Appropriate Disability Insurance can provide peace of mind and financial security while dealing with the real focus: regaining your health.