Download

1 / 2

20 likes | 80 Views

When you’re in the position of buying a house and appropriately tending your loans as well, the most vital part is to determine the best use of your money in order to reduce your debt and manage a mortgage plan at the same time. Simply put, you should look for a monthly payment which is low enough that you still have remaining funds which can used to decrease your debt amount or, if possible, add to your savings. Visit site: http://www.reteotto.net/mortgage-payment-tips/

E N D

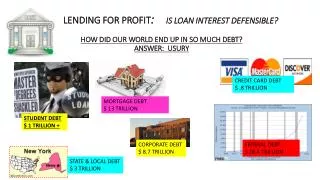

Buying a House? How to Manage Debt When you’re in the position of buying a house and appropriately tending your loans as well, the most vital part is to determine the best use of your money in order to reduce your debt and manage a mortgage plan at the same time. Simply put, you should look for a monthly payment which is low enough that you still have remaining funds which can used to decrease your debt amount or, if possible, add to your savings. In even simpler words, don’t bite off more than you can chew. Here are some mortgage payment tips to keep in mind when planning to buy a house. Though, the best possible scenario for your financial planning would be to have minimal or zero debt and hold a larger mortgage payment – which means buying the house with less money down. This is because in most cases consumer debts have no tax benefits. Bigger mortgages mean bigger payments. But when you consider the fact that your deductions are improved when you have a bigger mortgage on your home, it may make more sense to first clear all your debts. In most cases however, investing cash to avoid consumer obligations – even if it involves 0% interest – will most likely prove to be in the favor of the mortgage company. This is because all the mortgage companies keep an eye on the

minimum payment on every obligation, each month. Paying more, may make you feel better, but the bank won’t applaud you for it. If, on the other hand, you are sure you can pay off the higher down payment as well as settle off the other debts while maintaining the mortgage payment, this can be a win-win situation as soon as the consumer obligations are paid off. The challenge many people face is when they want to buy a home but are already deep in debt and this is exactly what the mortgage company sees in order to create a suitable plan for you. And, in this situation, a lower down payment reduces your buying power as well. Reducing your debts by as little as $500 per month may give you $100,000 additional buying power for your home! So whichever decision you make – whether it’s putting your money into a higher down payment or trying to pay off your debt with the money you have – the final decision is yours. But you need to make sure that it is something you can manage easily and that you will not be putting yourself in a huge pile of loan and payment plans which you cannot get rid of in time. So before you begin searching for a home, the most constructive idea is to first check your credit reports and your credit scores to see how deep in the ocean of debt you actually are. You also need to make sure that there are completely zero errors in your credit reports which could be dragging down you score.