Download

1 / 15

170 likes | 400 Views

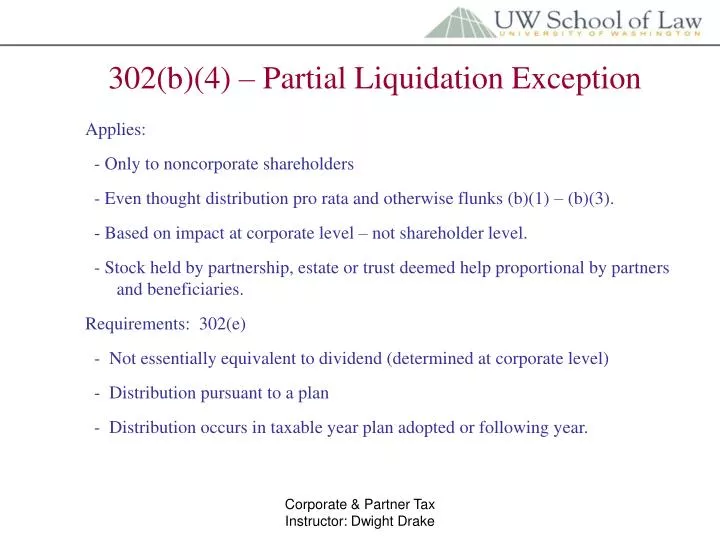

302(b)(4) – Partial Liquidation Exception. Applies: - Only to noncorporate shareholders - Even thought distribution pro rata and otherwise flunks (b)(1) – (b)(3). - Based on impact at corporate level – not shareholder level.

E N D

302(b)(4) – Partial Liquidation Exception Applies: - Only to noncorporate shareholders - Even thought distribution pro rata and otherwise flunks (b)(1) – (b)(3). - Based on impact at corporate level – not shareholder level. - Stock held by partnership, estate or trust deemed help proportional by partners and beneficiaries. Requirements: 302(e) - Not essentially equivalent to dividend (determined at corporate level) - Distribution pursuant to a plan - Distribution occurs in taxable year plan adopted or following year. Corporate & Partner Tax Instructor: Dwight Drake

Partial Liquidation – Not Essentially Equivalent to Dividend Safe Harbor: - Distribution attributable to ceasing to conduct “qualified trade or business” – operated for 5 years and not acquired during 5 yr period in transaction that recognized gain or loss. - After distribution, corp still involved in active conduct of “qualified trade or business.” Non- Safe Harbor Scenarios - Tough – must show serious contraction of business. - Example: Fire destruction; corporate cutback and all insurance proceeds distributed. - Bona fide business reason unrelated to desire to bail out liquid assets - No hope if plan is to bail out accumulated investment assets Corporate & Partner Tax Instructor: Dwight Drake

Problem 600 Basic Facts: A Corp has publishing business (“Books”) , bar review course division (“Cram”), all stock of B Corp (beta processing), and securities portfolio. A Corp stock owned equal shares by M & P (H & W) and I Corp (unrelated). A distributes Books (more than 5 yrs owned, as is Cram) to shareholders in equal shares and redeems 50 shares from each. - For M &P, qualifies for exchange as partial liquidation if pursuant to “plan”, done within year of plan or next year. A Corp must continue to operate Cram. Both held 5 yrs. Same result if no actual share surrender (just reallocate basis to stock). Makes no difference if pro rata under (b)(4) partial liquidation provision. - Partial liquidation provision not available to corp shareholder. So I Corp stuck with dividend under 301 (pro rata kills any hope of other three 302(b) provisions). 243 dividend deduction of 70% available, but any redemption that is part of partial liquidation requires stock basis reduction under 1059. Corporate & Partner Tax Instructor: Dwight Drake

Problem 600 Basic Facts: A Corp has publishing business (“Books” , bar review course division (“Cram”), all stock of B Corp (beta processing), and securities portfolio. A Corp stock owned equal shares by M & P (H & W) and I Corp (unrelated). What impact in (a) if books bought 3 yrs ago for cash? Not qualified business because not held 5 years. All shareholders have 301 dividend. Concern is bailing liquid cash through partial liquidation. Hence, 5 yr rule. If bought in tax-free reorg,where stock used, could qualify if business ran for 5 yrs. Here, no liquid asset bailout. Books destroyed by fire, 1/2 insurance proceeds distributed pro rata and other half used to scale down book business. I Corp still dividend. For P & M, not qualify under 302(e)(2) because not ceasing business or distributing all assets. Could be “not essentially equivalent to dividend” under (e)(1) but need more facts to see if it corporate contraction. For ruling purposes, IRS requires 20% cut in revenues, FMV and employees. Rev. Proc. 2002-3. Corporate & Partner Tax Instructor: Dwight Drake

Problem 600 Basic Facts: A Corp has publishing business (“Books” , bar review course division (“Cram”), all stock of B Corp (beta processing), and securities portfolio. A Corp stock owned equal shares by M & P (H & W) and I Corp (unrelated). Same as (a) but Books distributed to Michael in redemption of all his stock. Valid partial liquidation - exchange treatment allowed. Also may qualify under (b)(3) (family attribution waived) and maybe (b)(1) (attribution interest reduced from 67% to 50%). Same as (a) but Books distributed to I Corp in redemption of all stock. Although can’t qualify under be partial liquidation provision, qualifies under (b)(3) as termination of complete interest. Exchange treatment allowed. Securities portfolio distributed pro rata in redemption. No hope. Not partial liquidation or corporate contraction. 301 dividend to all shareholders. Corporate & Partner Tax Instructor: Dwight Drake

Problem 600 Basic Facts: A Corp has publishing business (“Books” , bar review course division (“Cram”), all stock of B Corp (beta processing), and securities portfolio. A Corp stock owned equal shares by M & P (H & W) and I Corp (unrelated). A sells stock in B Corp and distributes proceeds pro rata. Sub corp stock can’t qualify as partial liquidation per Rev. Rule 79-184. Hence, 301 dividend to all shareholders. A liquidates B Corp (operated for more than 5 yrs) and distributes assets in pro rata redemption. If liquidated in non-taxable transaction under 332 (discussed later in course), A picks up all B Corp attributes and may qualify as partial liquidation per Rev. Rule 75-223. Corporate & Partner Tax Instructor: Dwight Drake

Redemption Impact on Corp Two issues: - Gain or loss to corp on distribution of property other than cash. 311 governs the same as it does for non-liquidating distributions. Gain is always recognized by corporation, but losses not recognized. - E&P impact. E&P reduced by amount of distribution, but per 312(n)(7) reduction can not exceed ratable share of E&P attributable to redeemed stock. So if 1/3 stock redeemed, E&P before redemption can not be reduced more than 1/3. - Stock acquisition expenses paid by corp (brokerage commissions, legal fees, etc) are not deductible per Section 162(k). They are treated as non-amortizable capital expenditures. Amounts paid that have no nexus to redemption (employment agreement amount) are deductible and loan costs and fees involved in redemption may be amortized over term of loan. Corporate & Partner Tax Instructor: Dwight Drake

Problem 604 Basic Facts: X Corp shareholders A & B: 100 shares each with 100k basis. X E&P 120k accumulated from prior years, no current E&P, net worth 400k. X pays A 200k cash for A’s stock. Assume exchange treatment. Consequences to X Corp E&P? Since half shares redeemed, 312(n)(7) limits E&P reduction to half reduction in E&P. Thus, remaining E&P reduced to 60k as a result of redemption. Corporate & Partner Tax Instructor: Dwight Drake

Zenz Bootstrap Acquisitions Three scenarios all part of common plan: Scenario 1: Shareholder sells some stock and then has corporation redeem balance of shares. Qualifies under 302(b)(3) even though corporate E & P distributed to help facilitate acquisition. Zenz case/ Scenario 2: Corporation sells new shares to new shareholder and then redeem shares from existing shareholder. Percentages before and after both transactions control whether (b)(2) “substantially disproportionate” tests met. Scenario 3: Existing shareholder sell some shares to new shareholder and then have corporation redeem shares from existing shareholder. Percentages before and after both transactions control whether (b)(2) “substantially disproportionate” tests met. Rev. Rule 75-447 Corporate & Partner Tax Instructor: Dwight Drake

Problem 609 Basic Facts: S sole shareholder of T Corp., to be sold to B where B pay 400k for 80% of stock and Zenz redemption for 20%. - Can qualify for exchange treatment as complete (b)(3) redemption under Zenz case so long as all part of the same plan. - Consider E&P implications. If exchange, T Corp E&P reduced 20%, but not over 100k amount distributed in redemption. If 301 dividend, E&P reduced 100k. Thus, if E&P less than 500k before, may get bigger E&P reduction (a good thing for B) with dividend. Corporate & Partner Tax Instructor: Dwight Drake

Corporate Buy-Sell Agreements • Most important document in many privately-owned businesses • Determines value and exit opportunities for shareholders • Contain buy-out triggers: death, disability, bankruptcy, expulsion, etc. • Many tax issues, including estate tax valuation. • Often rely on (b)(3) exception for family businesses • Constructive dividend trap • - Co-shareholders become obligated under agreement to buy out a departing shareholder. Cross-purchase structure. • - Corporation then discharges obligation of co-shareholders by redeeming stock. • - Result is constructive dividend to co-sharholders. • - Often screwed-up through bad life insurance structuring. Corporate & Partner Tax Instructor: Dwight Drake

Corporate Buy-Sell C Corp Cash or Property Constructive dividend Sells Stock Shareholder A Shareholder B Cross-Purchase Buy-Sell Agreement Corporate & Partner Tax Instructor: Dwight Drake

Problem 615 Basic Facts: A, B & C unrelated equal shareholders of Y Corp with cross purchase buy-sell. Y Corp owns polices on each shareholder. B dies, Y Corp collects policy and pays proceeds to redeem B stock. • Premium payments by Y Corp not deductible per 264(a)(1). • Premium payments by Y not dividend to any shareholders because Y Corp own policy. • Insurance proceeds received by Y Corp tax free per 101(a). • Y Corp E&P increased by excess of insurance proceeds over aggregate premiums paid on policy. • On payment of insurance proceeds in redemption of B stock, A & C have constructive dividend distribution because their obligation to buy shares being satisfied by Y Corp. Defective buy-sell planning. 301 dividend to extent of E&P. Corporate & Partner Tax Instructor: Dwight Drake

Marital Dissolution Stock Redemption C Corp Cash or Property Constructive dividend Sells Stock Spouse A Spouse B Divorce Decree Corporate & Partner Tax Instructor: Dwight Drake

Final Regs Under 1041 Issue: If redemption part of divorce, what is relationship of 1041 (no gain or loss on divorce property division) and 302 redemption provisions? Reg. 1.1041-2(c) If redemption for benefit of non-transferring spouse under “primary and unconditional” obligation standard, then: - No gain or loss to transferring spouse per 1041. - Constructive dividend to non-transferring spouse. If “primary and unconditional standard not met for constructive dividend, then 1041 not apply and transferring spouse must recognize gain or loss. Parties may elect opposite rule to one that would otherwise apply if they both agree. Bottom line: No opportunity to whipsaw and both avoid tax. Corporate & Partner Tax Instructor: Dwight Drake